BOFIT Weekly Review 26/2026

Foreign government yuan bond issues – a small, but growing market

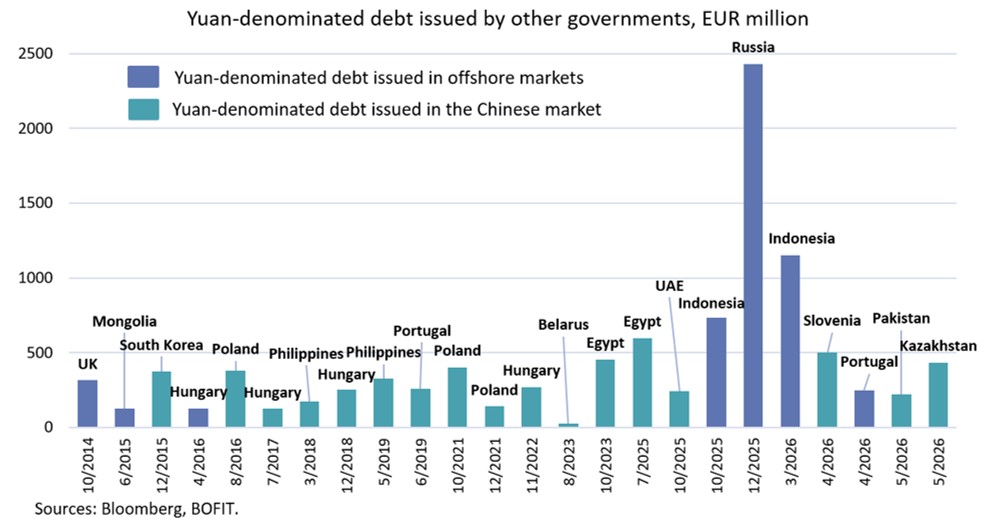

The volume of bonds denominated in Chinese yuan issued by foreign governments has risen in recent years. Such yuan bonds generally fall into one of two categories: “panda bonds” issued for the mainland China market and “dim sum” offshore yuan bonds issued outside China (mostly in Hong Kong). Although the market is still tiny, its recent growth suggests a gradual increase in the yuan’s international acceptance.

When the panda bond market launched in 2005, the number of issuers was quite limited and regulations on the use of funds raised was quite strict. Regulation has since been gradually relaxed, the number of issuers increased and the rules on the use of funds clarified. Panda bonds and dim sum bonds serve different purposes. Panda bonds offer issuers the opportunity to raise funding from Chinese investors. They are only issued on China’s domestic market and are subject to Chinese government regulation. Dim sum bonds offer issuers a flexible way to raise yuan funding from international investors. They are issued in offshore markets, typically Hong Kong. The lion’s share of issuers of panda and dim sum bonds are firms with strong ties to China. Growth has clearly accelerated in recent years. The trend has been supported by Chinese interest rates, which have generally been lower than elsewhere, as well as geopolitical tensions that have driven some firms to shift their China-related financing to the Chinese domestic market.

In 2014, the UK became the first foreign country to issue a yuan-denominated bond, a 3-year dim sum bond issue worth slightly over 300 million euros. The first foreign government panda bond was issued the following year, when South Korea issued a yuan-denominated bond on China’s domestic market. Yuan-denominated bonds were also subsequently issued by other countries, including Hungary, Poland, Portugal, Egypt and the Philippines. In April 2026, Portugal and Slovenia also sought yuan-denominated financing. Portugal’s 8-year dim sum bond issue of roughly 250 million euros carries a coupon rate of 1.77 %. Slovenia’s 3-year issue worth roughly 500 million euros carries a coupon rate of 1.9 %. As comparison, the yield on Portugal’s 10-year euro-denominated government bond was around 3.4 % in April, while the yield on Slovenia's 5-year government bond was around 2.8 %.

Several factors drive the increased interest in yuan-denominated credit. Economic relations between China and developing economies have deepened, increasing demand for yuan-denominated financial instruments. The increase in the price of dollar-denominated financing and reduced access to financing in some areas, have also increased interest in alternative sources of financing. Yuan-denominated financing remains relatively cheap due to China’s low-interest rate environment and demand is supported through regulatory changes. For example, Chinese authorities have allowed the external use of funds raised through the issuance of panda bonds since the beginning of 2022.

The trend is incremental, however. Restrictions on capital movements, the low liquidity of secondary markets, exchange rate risk, regulatory and transparency uncertainties, and restrictions on issuer use of yuan-denominated financing for their own needs continue to dull the allure of yuan-denominated credit. Individual issuances often gain prominence, but the yuan’s role as an international financial currency remains severely limited relative to the dollar or euro. Its significant expansion would require, above all, relaxation of China's rules on capital movement. The prospects for international yuan use and the possible limitations are discussed in BOFIT Policy Brief 1/2026.