BOFIT Weekly Review 27/2026

Russia faces increasing challenges in balancing its economic policies

The rising costs of the Ukraine war have forced the Russian government to increase spending, causing the federal budget deficit to expand further. High spending growth adds to inflationary pressures, making it difficult for the central bank to lower its key rate. High interest rates also curb investment and reduce profits, especially for companies that lack access to state-subsidised financing. Output growth has slowed in sectors not linked to the war effort. High interest rates also increase the costs of servicing public debt, which is especially concerning as Russia’s rising deficit is financed with debt. Russia faces increasingly difficult economic policy choices as it pursues its war of aggression in Ukraine.

A moderate key rate cut by the Russian central bank

The Central Bank of Russia (CBR) board decided at its inflation meeting on June 19 to lower the key rate. The cut was modest, just 25 basis points, bringing the current rate down to 14.25 % p.a. The CBR board noted the spring slowdown in inflation was largely due to transient factors. Consumer prices rose by 5 % y-o-y in May. More specifically, the CBR leadership said its rate cut restraint was justified by the increased risk that inflation could pick up in coming months.

CBR governor Elvira Nabiullina added that other emerging inflation drivers were the recent rapid rise in prices of fuel and certain foods. Fuel availability has become difficult in many regions due to Ukrainian drone strikes on Russian oil refineries and fuel distribution infrastructure. Gasoline prices were up 20 % y-o-y at the end of June. Governor Nabiullina said it would take time to restore supplies and that the increase in fuel prices could influence inflation expectations. Prices for some foodstuffs have risen rapidly in recent weeks. Prices of potatoes and onions, for example, were up about 20 % in June, while prices for beets and cabbage rose by around 10 %. Although the annual price increases for regulated municipal services this year are not going to be implemented in July as usual, Nabiullina reminded reporters that the hikes had only been postponed until October, after the Duma elections in September, and thus inflationary pressures will persist.

Discussing general inflation risks, Nabiullina warned of the possibility of overly expansive fiscal policy and the acceleration of credit growth in recent months. These risks could force the CBR to keep its key rate higher that it had predicted in its spring forecast. She stressed that further rate cuts at upcoming meetings should not be treated as a foregone conclusion.

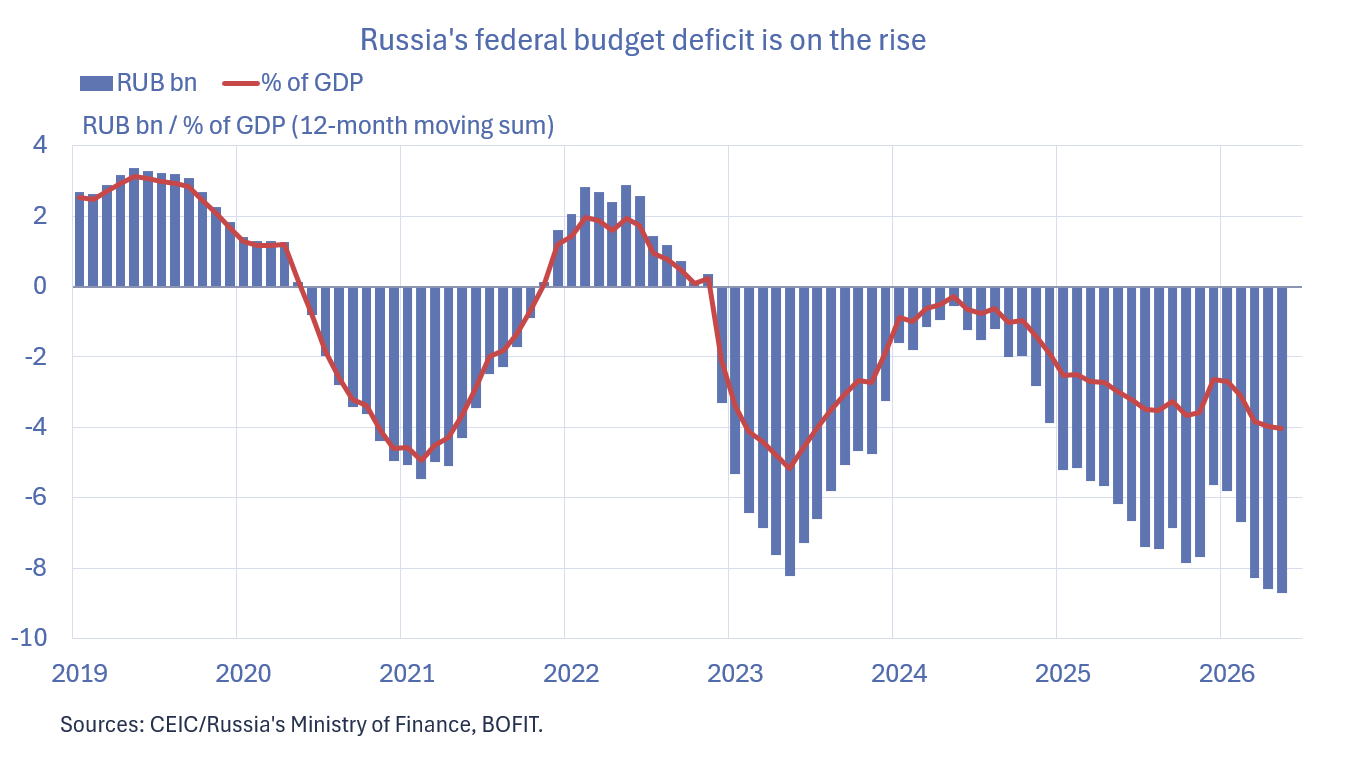

Federal budget spending continues to soar and deficit balloons

Russian federal budget spending soared in the first five months of this year, well above the few percent expenditure increase called for in this year's official budget. Preliminary figures show federal budget spending were up 17 % y-o-y in the first five months of this year. The growth in expenditure was driven by government procurement, which grew by 50 % y-o-y. Russia has discontinued to publish more detailed breakdown of federal budget spending.

Growth in federal budget revenues has failed to keep up with spending growth. In January-May, the revenue of the entire federal budget was comparable to the same period last year. After a weak start to the year, oil & gas revenues were still down by 30 % y-o-y. The rise in oil prices as a result of the Iran war only began to show up in Russia’s budget revenue reporting in May, when oil & gas revenues were up 33 % y-o-y. However, the impact of high oil prices on budget revenues has been mitigated to a certain extent by the government’s use of compensation payments to entice oil refiners to sell their products to domestic consumers rather than export those products. Boosted foremost by higher value-added tax revenue, federal budget revenue streams other than oil & gas grew by 12 % y-o-y in the first five months of this year.

The federal budget deficit swelled to 6 trillion rubles (2.6 % of GDP) in January-May, twice the amount budgeted for the entire year. Finance minister Anton Siluanov said the deficit was due in part to the front-weighting of Russia’s annual spending cycle. He also announced that this year's budget will be revised with an increase in the projected budget deficit. The proposed budget amendments will be submitted to the Duma this autumn.

Corporate borrowing continued to increase this spring

CBR data show that the total loan stock of the Russian banking sector grew by about 12 % in January-May. Corporate lending grew by around 13 % y-o-y in April and May. May saw growth in the stock of loans accelerate to 1.5 % m-o-m. Corporate credit growth has apparently focused on large state-owned companies and the construction sector. In contrast, the growth in the loan stock of small and medium-sized enterprises (SMEs) has been quite modest throughout the year, with the SME loan stock, excluding construction companies, declining for the second year in a row. High interest rates and tax hikes may have made borrowing more difficult for SMEs.

During January-April, a significant share of new corporate loans went to companies in the commercial and financial sector (sectors that account for a significant share of the total loan stock). Compared to the same period last year, however, the volume of new loans to companies in the forest industry, the tobacco industry, companies producing metal products and transport equipment grew particularly rapidly.

High interest rates and changes in government mortgage schemes have impacted household borrowing. The housing loan stock grew by about 10 % y-o-y in the first five months of this year. Household consumer credit has seen a slight increase in recent months, but in May the consumer credit stock was still around 5 % lower than a year earlier.

While the amount of non-performing loans has increased steadily, non-performing loans continues to represent a small share of the total loan stock. The CBR also releases figures for troubled loans using a broad definition. This wider category includes truly non-performing loans, very high risk loans and certain receivables from restructured loans. The CBR reported 11.2 trillion rubles in problematic corporate loans at the beginning of May, or 11.6 % of the total corporate loan stock held by banks. In May 2025, the amount of non-performing corporate loans was around 9.1 trillion rubles. Credit loss provisions and good quality collateral were sufficient to cover about half of the stock of non-performing loans, which the regulator considers a safe level. The share of non-performing loans at risk corresponds to about a quarter of the sector's equity. In addition, 13 % of consumer loans were non-performing and 2 % of housing loans. In these cases, the credit loss provisions of banks are sufficient to cover almost 90 % of such non-performing loans.

Banking sector operating profit in the first five months of the year was at the same level as a year earlier. The number of loss-making banks increased slightly, but they only represented roughly 6 % of the sector’s total assets. Banks’ return on equity (ROE) climbed to 19 % in May, a slight increase from last year. The strong financial performance of banks has also been reflected in modest equity increases. In May, the sector’s ROE was up 16 % y-o-y. The ability of Russian banks to absorb losses is good on average, but differences between specific banks may be large.