BOFIT Weekly Review 22/2026

China’s April economic growth slows from first-quarter pace

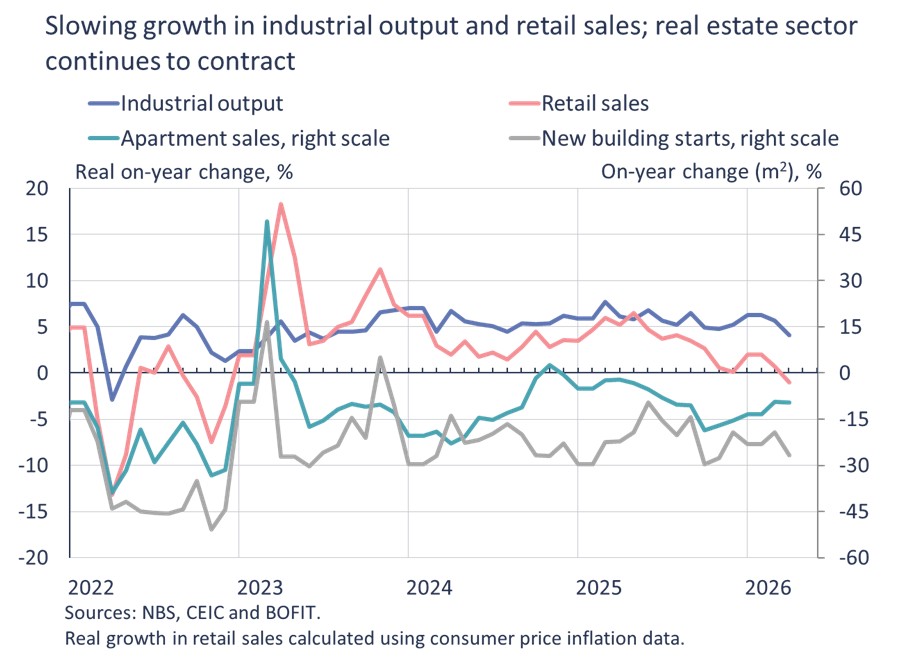

With nominal retail sales growth of just 0.2 % y-o-y in April, real growth in retail sales, which accounts for consumer price inflation, was clearly negative. Growth in online commerce slowed to around 6.5 % y-o-y, down from an average pace of nearly 9 % in the first three months of 2026 and over the past year. April sales of catering services grew at an annual rate of about 2 %, also slowing from the first quarter. China's official purchasing managers’ subindex for the services sector (services PMI) fell slightly below the 50-point neutral reading, while the S&P Global index, which has a greater focus on private businesses, remained in positive growth territory at 52.6 points.

Real industrial output growth also slowed to 4.1 % in April, down from over 6 % growth in January-March. There is, however, considerable variation across industries. Growth in manufacturing involving high degrees of processing remained robust, particularly manufacturing of electronics and telecommunications equipment (up over 15 % y-o-y). Growth in manufacturing of cars and other transport equipment rose by nearly 10 %. The pace of growth in the machine-building and chemical industries also exceeded the average. In contrast, construction-related industries continued to contract. Cement production, for example, declined more than 10 %. Growth in the beverage and textile industries was also muted or negative.

China’s foreign trade keeps powering along. The dollar-value of goods exports in April rose by 14 % y-o-y, while imports were up by 25 %. Export growth was supported by demand for cars and AI-related components. The rapid increase in the value of imports was driven by electronic devices (especially microchips) and partly also by rising energy prices. The import volumes of oil and petroleum products fell in April, however, suggesting China was dipping into its strategic hydrocarbon reserves. China typically increases its energy purchases when oil and gas prices are low and reduces such buying when prices are high.

Producer prices, driven mainly by rising energy prices, were up 2.8 % y-o-y. The increase in prices was driven by higher prices for intermediate goods (up 3.8 %), while producer prices for consumer goods remained negative (down 1 %). Consumer price inflation was up by 1.2 % in April. Inflation was restrained by falling prices for food and housing, while prices for energy, healthcare-related services, education and cultural services boosted the overall rise in prices. Core inflation, which excludes food and energy prices, was also up by 1.2 %.

Although the overall credit stock expanded by 5.5 % y-o-y, bank lending was down in April compared to March. The growth in the credit stock was entirely driven by increased lending to non-financial corporations, as the stock of household loans contracted by 2.6 % y-o-y. The household credit stock has contracted in every month since November 2025.

Weak household demand for credit largely reflects China’s years-long real estate downturn. Measured in terms of floorspace, April apartment sales were down by nearly 10 % y-o-y, and new building starts down by about 25 %. The decline in new construction starts, which has gone on for several years already, has gradually reduced the number of unsold apartments. As of April, the number of unsold apartments was only 1 % higher than a year earlier.