BOFIT Weekly Review 23/2026

Russian economy stabilising after weak start of the year

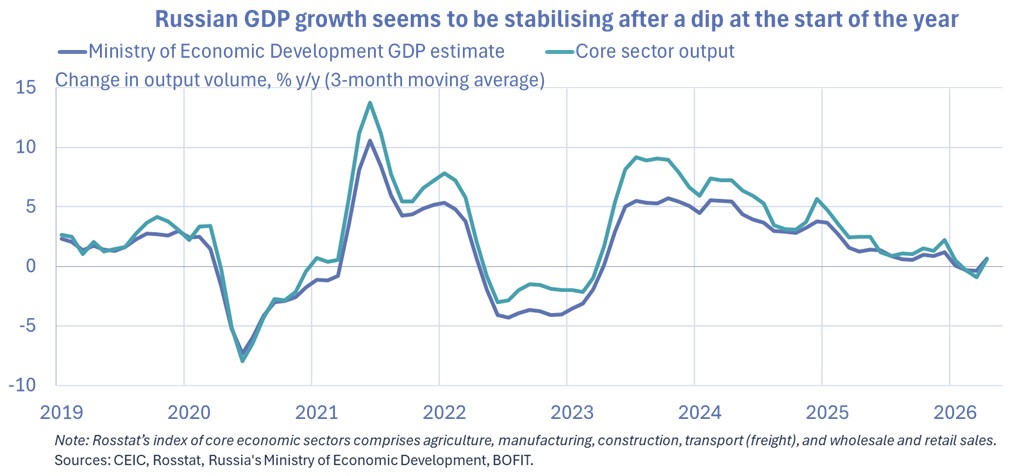

Trends in Russian GDP growth tracked using Rosstat’s composite index of five core sectors of the economy (agriculture, manufacturing, construction, freight transport, as well as wholesale and retail sales) show growth in March-April of roughly 2 % y-o-y, up from an on-year contraction of nearly 3 % in January-February. Russia’s economic development ministry estimates that GDP grew by 1.3 % y-o-y in April. Due to weakness in the first two months of 2026, on-year GDP growth in January-April was essentially zero.

Specific branches display divergent economic trends this year. Investment has contracted sharply which has been reflected in weak development of construction and production of many investment goods. Private consumption has continued to increase, supporting consumption-driven branches such as trade and production of foodstuffs. Federal government expenditures rose rapidly in the first months of this year supporting strong growth in manufacturing industries linked to the war.

Recent forecasts expect Russian GDP growth overall to remain tepid both this year and next. Russia’s economic development ministry has lowered its 2026 GDP growth forecast significantly to just 0.4 %. The OECD’s latest forecast also sees Russian GDP growth of just 0.5 % this year. Most international forecasting institutions anticipate that Russian GDP growth will hover around 1 % both this year and next.

Sharp drop in fixed investment

Preliminary Rosstat figures show investment in fixed capital contracted in the first quarter of 2026 by 14 % y-o-y. While fixed investment growth was fairly brisk in previous years, investment activity has come to a screeching halt in recent months. The last time such a large drop in investment activity was seen was in 2009 during the global financial crisis. Investment this year is down sharply in nearly all industries. The rare exceptions include public administration and national defence services, finance and insurance businesses, aerospace and tourism services.

It has become significantly harder to finance investments. In recent years, firms have increasingly financed investments out of their own pockets. In January-March, total corporate earnings contracted by 26 % y-o-y, with 37 % of companies posting 1Q losses. The share of loss-making companies this year is slightly higher than during the last peak at the pandemic year of 2020. Russia has also raised corporate taxes. The corporate profit tax was hiked already last year and a new windfall tax that firms would have to pay this year is currently being drafted. Corporate borrowing costs also remain high, as the Central Bank has been able to lower the key rate only gradually. The share of bank lending in investment financing has declined over the past year.

Business sentiment surveys reveal that companies are also less upbeat about their future investment plans. The demand outlook has become gloomier and capacity utilisation has fallen significantly in many sectors.

On the production side, investment weakness was particularly evident in construction. Construction continued to contract in April, down by 5 % y-o-y. For January-April, the overall the drop was 8 %. With the exception of war-related manufacturing activity, output contracted in most manufacturing sectors in April.

Consumption continues to support the economy

Following a subdued trend at the start of the year, consumer spending appears to have recovered somewhat in recent months. The volume of retail sales rose by over 6 % y-o-y in both March and April. Growth in services remained stable at around 3 % throughout the first four months of this year. Growth was brisk in branches such as telecommunications and digital services, as well as consumer electronics and appliance repair and maintenance services. Additionally, Sberbank’s indicator for consumer spending shows a similar pattern, pointing to a rebound in consumer spending in recent months following weaker development at the start of the year.

The unemployment rate remains at historically low levels, with wage growth again accelerating in the early part of this year. In January-March, the average real monthly wage rose by 9 % y-o-y, while real disposable incomes were up by nearly 2 % y-o-y. The CBR’s survey notes that companies expect in coming months to see growth in their personnel number and wage costs to slow down.

High oil prices boost Russian export earnings and tax revenues

Russia’s modest economic recovery in recent months has been supported by high oil prices on world markets that are a result of the ongoing Iran war. High oil prices have significantly increased Russia's export and budget revenues compared to the beginning of the year. Russian oil exports have also benefited recently by the temporary relaxation of sanctions on Russian oil by both the US and the UK.

The International Energy Agency (IEA) estimates that the average export price of Russian crude oil in April was $95 a barrel, and that the sanctions discount on Russian oil relative to benchmark grades remained at around $25 a barrel. The IEA calculates the discount on Russian crude by comparing it to the North Sea Dated price, which reflects prices of actual physical deliveries. The IEA estimates that the export volume of Russian crude oil increased slightly in April compared to March, while the export volume of petroleum products decreased. Russia has restricted the export of petroleum products to assure supply availability and restrain price increases on the domestic market.

The IEA estimates that Russia took in roughly 19 billion euros a month in oil export revenues in both March and April, almost double the amount taken in during the first two months of the year. Preliminary figures from the finance ministry show May budget revenues from mining tax on oil were almost triple those of previous months. Oil prices are expected to decline gradually, even if markets are still grappling with immense uncertainty. Futures markets at the beginning of June predict the price of Brent oil will average around $90 a barrel during the second half of this year.

Another big increase in government spending

While the recent spike in oil prices has improved the Russian government’s financial situation, low oil & gas prices in the first months of this year meant that federal budget oil & gas revenues in January-April were still down by nearly 40 % from the same period a year earlier. Total revenues of Russia’s federal budget fell by 4.5 % y-o-y in January-April.

The ruble’s strong exchange rate has moderated the impact of rising oil prices in recent months because budget revenues in Russia are denominated in rubles. According to preliminary data released by the finance ministry, oil earnings in April and May exceeded the budget plan by just over 200 billion rubles. Oil revenues were significantly below the budget plan, however, in the first three months of this year.

Despite declining revenues, government spending has increased rapidly this year, with January-April federal budget spending up by 16 % y-o-y. At the same time, the federal budget deficit ballooned to nearly 6 trillion rubles (2.5 % of GDP), or about 2 trillion rubles more than the planned budget deficit for all of 2026.

Several hundred billion rubles have been drawn this year from the National Wealth Fund to cover budget shortfalls. As of end-May, the National Welfare Fund held liquid assets worth roughly 3.4 trillion rubles (1.5 % of GDP). The government again plans cover most of the additional budget deficit by issuing government bonds.