BOFIT Weekly Review 20/2026

The yuan has appreciated moderately in 2026

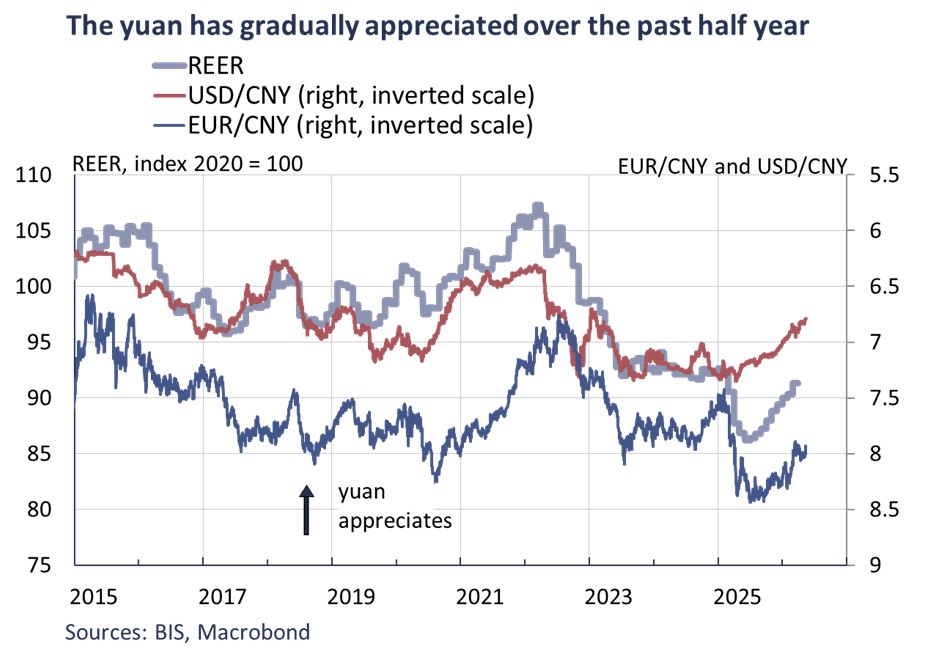

The yuan this year has strengthened somewhat against both the dollar and the euro. On May 14, one dollar bought 6.79 yuan, while one euro went for 7.93 yuan. Since the beginning of the year, the yuan has strengthened 3 % against the dollar and 2.5 % against the euro. The yuan’s real effective (trade-weighted) exchange rate (REER) in March was about 1.5 % stronger than at the start of January.

Much of the yuan’s modest appreciation reflects general dollar weakness and China's strong external position, with yuan demand sustained through robust export earnings and the large current account surplus. At the same time, the domestic risks to growth, China’s slower inflation than in the rest of the world, its low-interest-rate environment and uncertainty stemming of inflamed geopolitical tensions (particularly US-China trade tensions) limit yuan appreciation and could even put devaluation pressure on the yuan in some cases. The impact of external pressures is often limited, however, as capital flows are tightly regulated and the dollar-yuan exchange rate is actively managed. For example, the PBoC sets a daily reference rate (daily fixing) for the yuan-dollar exchange rate, around which the yuan is allowed to fluctuate within a ±2 % band during the day.

If the central bank thinks that the yuan is appreciating too fast, it has several tools at its disposal to curb the trend. The PBoC can signal its policy stance by setting the daily fixing rate at a level above or below market expectations, by guiding the activities of state-owned banks in the foreign exchange market, or through regulatory changes. At the end of February, for example, the PBoC lowered its foreign-exchange risk reserve requirement for forward forex sales from 20 % to zero, which makes it cheaper to hedge dollars and may increase demand for dollars.

International observers claim the yuan is undervalued relative to China’s economic fundamentals. The IMF, for example, put forth an estimate in its end-February report on its Article IV consultations that China’s real effective exchange rate was undervalued by 12–21 % last year and that REER weakening was a factor in creating China’s growing external imbalances. The IMF recommended that China allow greater exchange rate flexibility and clarify its exchange rate regime. At the same time, China has continued to push for greater international use of the yuan, albeit through managed channels.

This is reflected, for example, in central bank swap lines, through which yuan liquidity can be provided internationally. In the first quarter of the year, the drawdowns of other central banks using PBoC yuan swap lines climbed to its highest level in two years, reaching roughly 112 billion yuan at the end of March. Through these swap lines, a local central bank receives yuan from the PBoC, which it can then channel to domestic banks. This allows, for example, payments for trade invoices from Chinese suppliers to be made directly in yuan without first having to obtain dollars in the markets. This can facilitate payments, especially in situations where dollar funding becomes more expensive or less available. Recent developments in the international use of the yuan are discussed in this recent BOFIT Policy Brief.