BOFIT Weekly Review 20/2026

BOFIT sees China’s economic growth buoyed by exports this year, with a gradual slowdown over the next two years

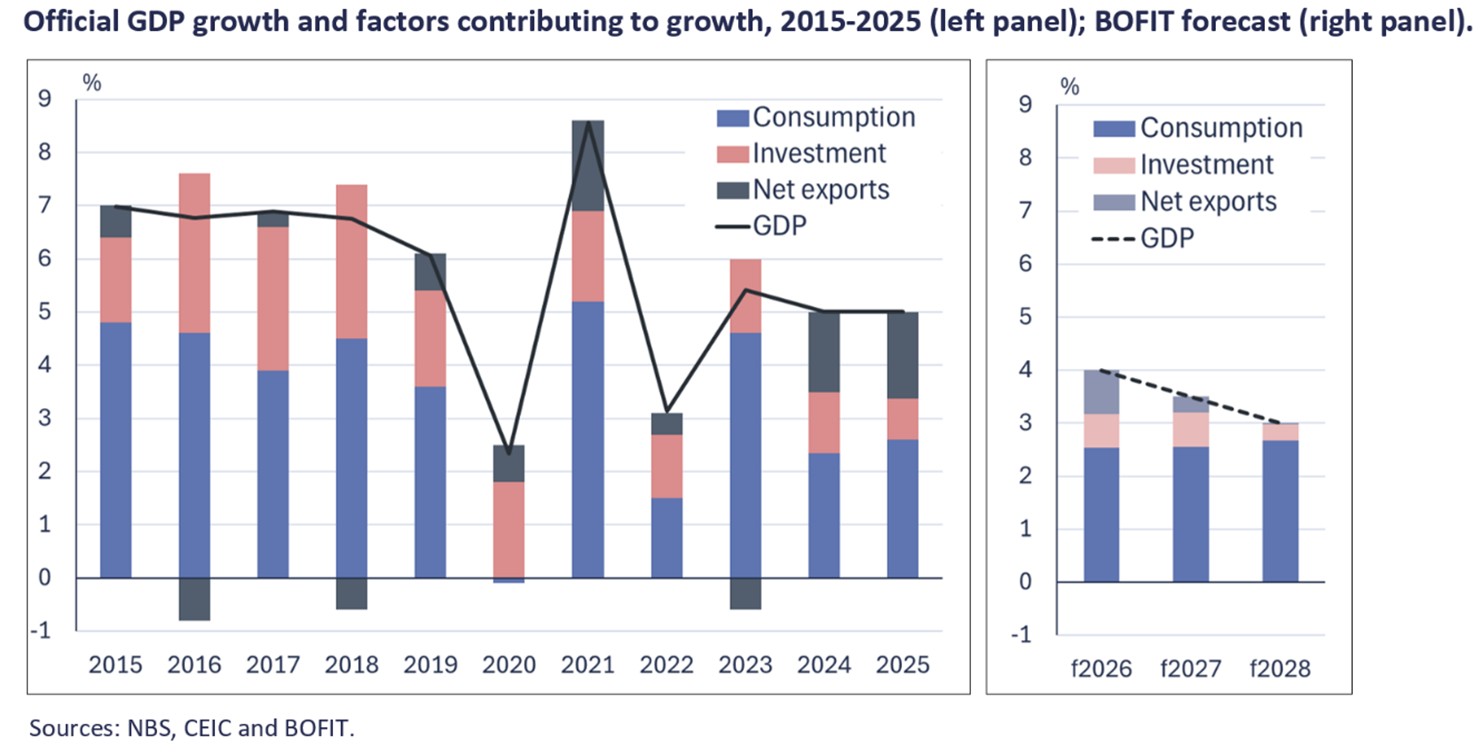

In the BOFIT Forecast for China 2026–2028 released last week, we predict actual economic growth this year to be around 4 %, roughly the same level of growth as last year. China’s economic growth has received surprisingly strong support from exports in recent years, and we forecast the impact of net exports on growth to stay positive this year as well. In 2027–2028, the impact of exports on GDP growth should fade while no meaningful improvement in domestic demand is expected. As a result, we see economic growth slowing to around 3½ percent next year and about 3 percent in 2028. Official statistics will likely again report figures that exceed our forecast and align with GDP growth targets, as the high political weight given to the targets does not allow for displaying clearly slower growth

The impact of the Iran War supply shock on China’s economy is expected to be smaller than for many Asian nations. Oil and natural gas account for a relatively small share of China’s total energy consumption, with domestic production and strategic reserves built up over the years being sufficient to blunt the impact of the current energy shock. The rise in global energy prices, however, affects prices in China as well. The more-than-three-year decline in producer prices came to an end this spring, with April producer prices up by 2.8 % y-o-y. The government has, however, implemented measures to mitigate the pass-through of high energy prices to consumer prices. Consumer price inflation is not expected to rise significantly over the forecast period due to subdued domestic demand and intense competition among Chinese producers. We also expect no major changes in China’s monetary stance. The People’s Bank of China remains cautious about significant monetary easing. Monetary policy is increasingly implemented in a targeted manner, funnelling inexpensive financing to priority areas.

Fiscal stimulus is unlikely to provide an additional boost to economic growth over the forecast period, despite a highly accommodative fiscal stance and large public sector deficits. China’s actual public sector deficit this year, like last year, is expected to be around 14 % of GDP, and the total public sector debt-to-GDP ratio is projected to rise above 130 % when off-budget activities, such as those of local government financial vehicles (LGFVs), are included. The economic situation of local governments has been weakened by a significant decline in revenues from land use right sales and by the central government’s efforts to rein in the use of LGFV financing. Local governments, which are responsible for the bulk of public spending, have seen their buffers for dealing with unanticipated problems shrink.

Economic policy will continue to focus on supporting exports and industry. Industrial policy has been shored up, self-sufficiency increased in key sectors, and high technology declared a top objective in the five-year plan beginning this year. The yuan’s relatively weak exchange rate supports exports, and China has invested heavily in fields where global demand is on track to grow rapidly such as artificial intelligence infrastructure and the green transition. In the next few years, export growth is expected to slow as China increases its share of global trade and trade barriers are expected to rise. In any case, China’s current account surpluses should remain substantial throughout the forecast period.

US president Donald Trump is currently on a state visit to Beijing to meet with Chinese president Xi Jinping. The trip is not expected to end superpower tensions. Furthermore, tensions with China’s other trading partners have intensified in response to the rising competitiveness of Chinese producers, large trade surpluses and China’s own trade policy actions (e.g. export restrictions). Some of China’s international competitiveness gains have been achieved through unfair trade-distorting practices such as providing government subsidies to firms. Trading partner countries are likely to seek higher tariffs and use other trade policy measures to level the playing field.

Uncertainty related to domestic economic development remains elevated. China has failed to implement reforms needed to bolster domestic demand, and the risks associated with its investment-driven growth model continue to increase. Indebtedness is rising, along with financial market risks. The lack of good-quality statistical data and censorship of economic discussion further complicate assessment of true economic conditions in China and make forecasting challenging. China also faces growing external uncertainty from rising geopolitical tensions. A slowdown in global demand growth, due e.g. to a prolonged energy market crisis, would also weigh on China's export-driven growth.