BOFIT Weekly Review 19/2026

Russian economy weakened sharply in first two months of the year; rising oil prices bring relief

While Russian economic trends weakened dramatically in January and February, transient factors were responsible for some of the GDP contraction. Economic activity has since revived on higher oil prices. Even if it takes time for the impact of increased oil earnings to be reflected on government balance sheets, they are clearly a boon for Russian government finances. Higher oil prices alone, however, are insufficient to resolve the issues with which the government currently struggles. Low, if any, economic growth is expected for the rest of this year, and federal government finances are expected to remain in deficit.

Spike in oil export earnings

The Iran war, which has reduced global oil supplies, caused a sharp rise in oil prices that has significantly increased Russia’s export earnings. The International Energy Agency (IEA) estimates that the average export price of Russian crude oil in March was $78 a barrel, up from an average price of $46 a barrel in January-February. Oil prices rose further in April and early May. The United States also temporarily relaxed sanctions on exports of Russian oil, making it easier for Russia to sell its oil and petroleum products. Both China and India have increased their oil imports from Russia.

Ukraine’s drone strikes on the Baltic ports of Primorsk and Ust-Luga, Russia's key ports in the Gulf of Finland, temporarily ceased operations at both ports at the end of March. Russia managed fairly quickly to resume some of its Baltic exports, however. The IEA estimates that the total volume of Russian oil exports (crude oil and petroleum products) in March was slightly greater than in February. At the same time revenues from of Russian oil exports doubled as a result of sharp price increases.

GDP growth returned in March

Russia experienced a sharp weakening in economic trends in the first two months of this year. The preliminary estimate from Russia’s economic development ministry shows GDP contracted by 0.3 % y-o-y in January-March. The economy’s performance was particularly weak in the first two months of the year. The economic development ministry also reported that GDP contracted in January-February by roughly 1.5 % y-o-y, noting that the poor performance partly reflected three fewer workdays than in the period compared to last year. The Central Bank of Russia (CBR) explained that some of the slowdown in growth came from hikes in value-added tax (VAT) rates at the start of the year and inclement weather that hampered e,g, construction work. The economy recovered in March and the economic development ministry evaluated the March GDP growth at 1.8 % y-o-y.

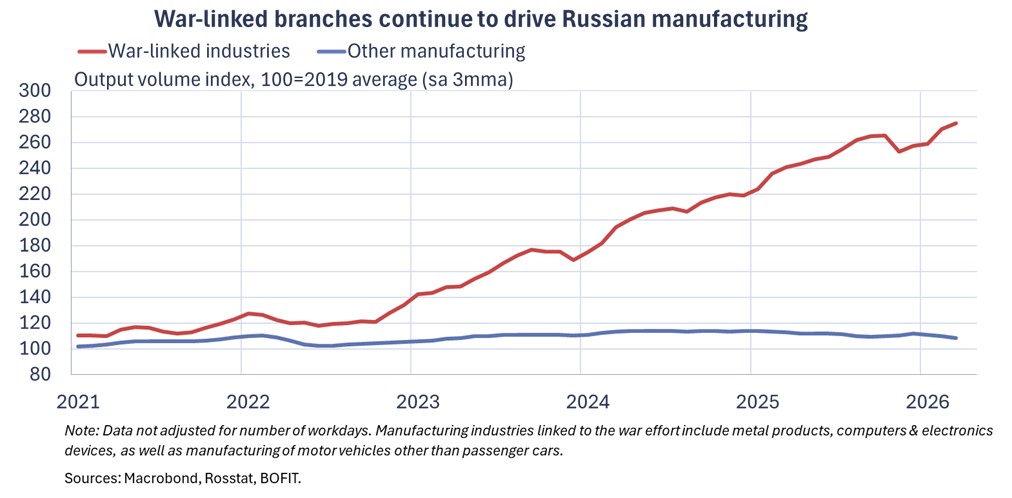

Rosstat’s headline figures show first-quarter industrial output growth was roughly the same as a year earlier. Rosstat’s seasonally-adjusted and workday-adjusted 1Q industrial output estimate, however, was up about 4 % y-o-y. March industrial output was also slightly higher than at the end of last year. Seasonally- and workday-adjusted output in both the extractive and manufacturing sectors increased slightly. The CBR’s April business survey found a distinct improvement in the business sentiment for the extractive sector (includes oil & gas), driven by higher oil prices. Expectations of manufacturers, in contrast, remained subdued like in the preceding months. Manufacturing this year has been again largely supported by industries linked to the war effort. For those industries, growth continued at a brisk pace throughout the first quarter. Output contracted 0n-year in nearly all other manufacturing industries. The diverging paths of industrial output in recent years is discussed in greater detail in this just-released BOFIT Policy Brief.

After a slow start this year, growth in the volume of retail sales revived to 6 % y-o-y in March. According to statistics reported by the Association of European Businesses in Russia (AEB), sales of new cars in March increased by 23 % y-o-y. Apparently at least part of the increase reflected temporary effects such as expectations of a hike in recycling fees on new vehicle purchases. Wages continued to rise rapidly in the first months of the year, with the average real monthly wage in January-February up by nearly 9 % y-o-y. The unemployment rate remained at a historically low level of around 2 %.

The contraction in construction output continued in March, with output falling 2 % y-o-y. The decline was, however, significantly less than in the previous two months (the construction sector contracted by 15 % in January-February). Housing construction has been one of the weakest segments in the construction sector. Measured in terms of floorspace, the volume of completed apartments in the first quarter was down by nearly 30 % from 1Q25. Housing construction has been especially hindered by the financing challenges of high interest rates, regulatory changes and increased building costs.

Delayed impact of higher oil prices on federal budget

Preliminary figures from the finance ministry show federal budget revenue contracted in the first quarter by 8 % y-o-y. Oil & gas revenues were down by 45 % y-o-y in January-March, reflecting the lag in oil & gas tax revenues when oil prices rise. Government revenue streams other than oil & gas increased by 7 % y-o-y. Growth in revenues was led by the general increases in VAT rates at the start of the year. VAT revenues were up by 10 % y-o-y in 1Q26.

Federal budget expenditures rose by 17 % y-o-y in the first quarter. 1Q spending growth was significantly higher than the budgeted increase in spending for the entire year. The finance ministry said the high spending level reflected front-loading of government procurements, which were up by 38 % y-o-y in the first quarter.

The 1Q federal budget deficit ballooned to 4.6 trillion ruble (2 % of GDP) which exceeded the projected budget deficit for the full year 2026. While higher oil prices should ease some of the current crisis in Russian government finances, the budget is likely to remain in the red throughout the year (see BOFIT blog). As of end-April, the National Wealth Fund (NWF) held liquid assets worth approximately 3.6 trillion rubles. The government is not planning to use the NWF this year to cover the deficit in substantial amounts, but instead will finance the gap mainly through increased debt. The possibilities of the Russian banking sector to finance the increasing government debt is discussed in this recent BOFIT Policy Brief.

Finance minister Anton Siluanov also announced on cancellations and restructurings of regional government debt to the federal government again this year. In addition, a new credit line is established for regions hit by acute financing shortages in order to help stressed regional governments avoid having to borrow from the market. Many regions struggled last year to cover their budget expenditure commitments and growing debt burdens.

CBR key rate cut in April

At its April meeting, the CBR board went ahead with another rate cut, lowering the key rate again by 50 basis points to its current level of 14.5 %. The CBR justified the latest cut by noting that demand growth that had been fuelling inflation earlier had slowed down. The central bank leadership further observed that the acceleration in inflation at the start of the year was due largely to transient effects from such measures as the increase in VAT rates and upward adjustment of administratively-set prices of municipal services. The CBR estimated that seasonally adjusted annualized rate of consumer price growth was 9 % in the first quarter, compared to 4 % at the end of last year. The CBR’s latest forecast published in connection with its rate meeting sees annual inflation running at 4.5–5.5 % in December.

At its next meeting in June, the CBR board will assess the appropriateness of another rate cut based on inflation trends and outlook. The latest CBR forecast sees the key rate averaging 13.3–14 % between May and December this year. The CBR noted that inflation outlook is subject to considerable uncertainty, however, due to the international situation and geopolitical risks, as well as risks related to fiscal policy. Under conditions of more relaxed fiscal policy and a deficit rising faster than planned, tighter monetary policy would be required compared to the baseline scenario.

The CBR typically engages in foreign exchange operations in accordance with a fiscal rule laid down by the finance ministry. The finance ministry announced in March, however, it was suspending foreign exchange operations under the fiscal rule in anticipation of rule changes. The government decided to resume its forex operations, however, to buffer some of the effects of recent swings in energy prices. Effective today (May 8), the central bank is resuming its forex and gold purchases at a level of 5.8 billion rubles a day.

Slim GDP growth expected for this year

Despite elevated oil prices, the CBR left its GDP forecast unchanged. While GDP is still expected to grow by 0.5–1.5 % this year, the central bank has raised its projections for export earnings and the size of the current account surplus. The export price of Russian crude is now expected to average $65 a barrel this year (up from the $45 a barrel). At the same time, revenues from goods exports are expected to be nearly $90 billion higher than in the CBR’s February forecast and reach $485 billion. With only a slight increase in the import outlook, higher export earnings should boost the current account surplus. The CBR’s estimate of this year’s current account surplus is now $72 billion, a considerable improvement from last year.

Despite the spike in oil prices, international forecasters have so far increased their GDP forecasts only slightly. For example, the IMF’s April forecast predicts Russian GDP growth this year will reach 1.1 %, up from its January forecast of 0.8 %. The April report from Consensus Economics stated that the average Russian GDP forecast for this year was just 1 %, only a smidgen higher than the consensus forecast of 0.9 % in February. Consensus Economics also reported that the average forecast for Russian export earnings this year substantially increased to $474 billion in April and to $79 billion for Russia’s current account surplus.