BOFIT Weekly Review 29/2021

Russia’s foreign goods trade recovered; corporate capital outflow rose

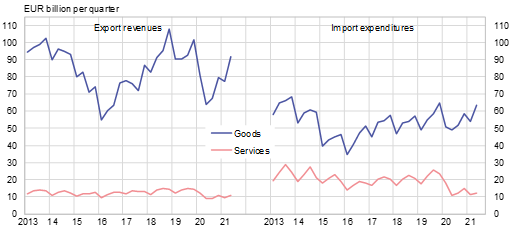

As expected, preliminary balance-of-payments figures from the Central Bank of Russia show that export revenues and import expenditures were much higher in the second quarter of this year than a year earlier when the first wave of covid-19 and economic decline diminished foreign trade. While export revenues and import spending were roughly at the same levels as in 2Q19, the situation for goods and services remained quite divergent.

Russian earnings on exported goods in the second quarter were up a few percent from two years ago. Revenues from oil & gas sector exports, however, were still down by about one tenth from their 2019 level. Revenues from crude oil exports remained significantly depressed. On the other hand, revenues from exports of non-oil-&-gas goods were up by over one fourth from two years previous. These other export goods also consist largely of basic commodities (e.g. metals) that have seen strong increases in their global prices. Russian revenues from services exports were significantly lower than two years previous especially because tourism to Russia remained small.

Spending on goods imports already in the first quarter of this year was substantially higher than two years earlier. In the second quarter, it was up by about one fifth from 2Q19, and actually at its highest in several years. Spending on services remained in a slump as Russian tourism abroad was still depressed while imports of other services were also down considerably from previous years.

Russia’s second-quarter current account surplus remained substantial, and for the last four-quarter period reached a level equal to roughly 3.5 % of GDP. The current account surplus was supported by the continuously large goods trade surplus and a considerably smaller-than-usual services trade deficit. The deficit deepened for outward and inward payments accruing from direct and other investments as well as credit largely because, after a brief hiatus, outward payments of dividends and interest from the corporate sector increased.

The financial account deficit remained rather large. Repayment of Russia’s sovereign bonds continued. Foreign-based investors this year also sold in net terms their holdings of Russian sovereigns on the secondary market. The net outflow of private capital diminished slightly, and over the last four quarters was equal to about 3 % of GDP. Most of it came from an increased net capital outflow of the corporate sector (not including banks). FDI inflows from abroad to Russian firms were still small (in the latest four-quarter period 0.7 % of GDP). Investors based abroad continued divesting their portfolio investments in Russian firms (0.9 % of GDP); these divestments started in autumn 2019. In addition, the non-bank corporate sector maintained relatively large outflows of direct and portfolio investments (0.9 and 0.8 % of GDP, respectively).

Revenues from goods exports and spending on goods imports have recovered

Sources: Bank of Russia and BOFIT.