BOFIT Weekly Review 16/2026

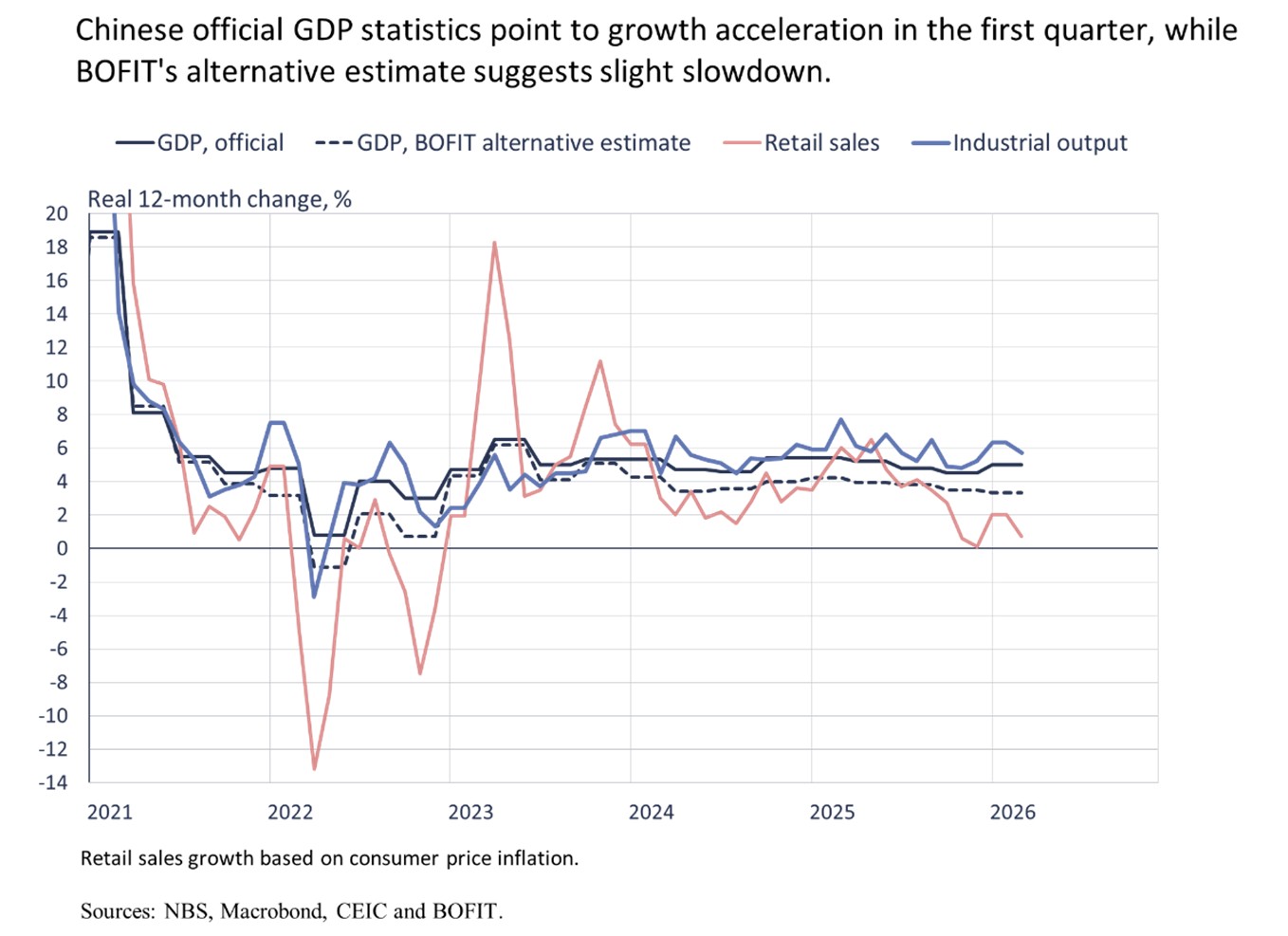

China’s official GDP statistics suggest the economy off to a decent start this year

China’s National Bureau of Statistics (NBS) reported on Thursday (April 16) that GDP growth accelerated to 5.0 % y-o-y in the first quarter of 2026, up from 4.5 % in 4Q25. According to the demand breakdown, the growth pickup was driven by rapid investment growth. It seems that in particular investment in production machinery and equipment grew very rapidly, likely related to the continued strong growth in industrial output and exports. Growth in retail sales was subdued in the early part of the year as the effects of government support programmes are fading. Contrary to the official data, BOFIT’s alternative GDP calculation suggests that GDP growth slightly slowed down in the first quarter. In conjunction with the release of our Forecast for China 2026–2028, BOFIT will hold a webinar briefing on Tuesday May 5 (sign-up link here).

Industrial output growth accelerated in the first quarter to 6.1 % y-o-y. Electronics production, up 14 %, was among the strongest performing major industries. Robust manufacturing growth in the first quarter was also reflected in ongoing growth in goods exports. China Customs reports the dollar value of 1Q exports rose by 15 % y-o-y. Export growth was broad-based. Exports increased by 20 % y-o-y to ASEAN countries, as well as grew by 21 % to the EU, 32 % to Africa and 9 % to Latin America. Exports to the United States, however, continued to decline (-16 %). Long-languishing growth in China’s imports also surged, rising by 20 % y-o-y. Remarkable growth in value terms was posted for imports of microchips (up 45 % y-o-y) and data processing devices (up 50 %). In contrast, the value of imported crude oil fell from 2025, even if import volumes rose in the first quarter. Geographically, imports increased from almost all parts of the world, with imports from ASEAN countries rising by 15 % y-o-y, from the EU by 11 %, from Africa by 18 % and from Latin America by 31 %, while imports from the US continued to decline (-18 %).

The war in the Middle East has had an impact on Chinese prices. Fuel prices have risen briskly, even if officials have restricted increases in prices at the pump. The rise in food prices, however, slowed in March, a phenomenon typical of the period following the Lunar New Year holiday season. March consumer price inflation was 1.0 % and core inflation (inflation excluding prices of energy and food) was 1.1 %. The latest episode of producer price deflation seems to be coming to a close, at least temporarily, as producer prices rose by 0.5 % y-o-y in March. Although the rise in energy prices gave a bump to producer prices, month-on-month changes in producer prices have been zero or positive since August 2025. Thus, it is likely that the long episode of producer price deflation was coming to an end even without the energy price shock.