BOFIT Weekly Review 17/2026

Fixed investment growth in Russia came to a standstill last year

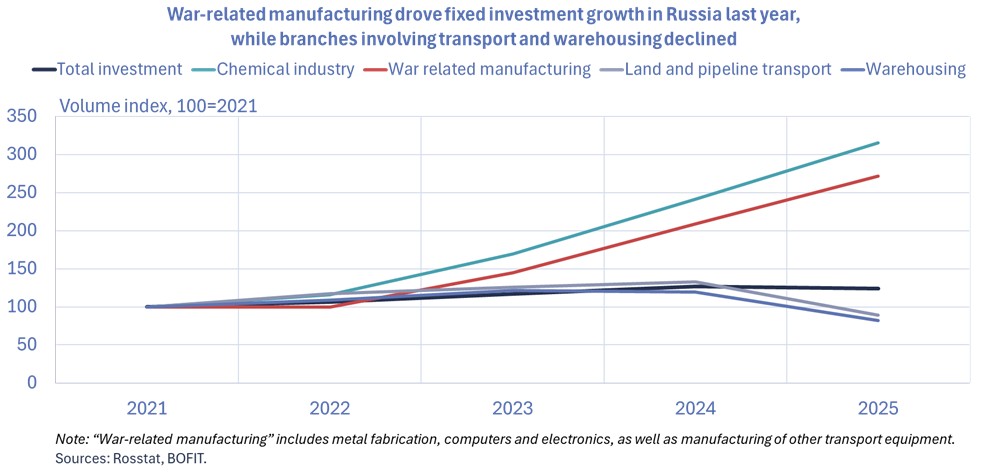

Russian fixed investment experienced across-the-board weakening last year, with completion of budget-funded infrastructure projects in the Far East Federal District having an especially negative impact on investment activity. The structure of investment in the country has changed considerably in recent years. Companies must increasingly finance investment projects out-of-pocket, and government budget funding is more precisely targeted than previously. Foreign financing for investment has dried up almost completely. Investment focuses increasingly on construction activity, while the share of investment in machinery & equipment has decreased. The most robust growth has been seen in manufacturing industries that support the war effort and in the chemicals industry. In addition, infrastructure projects have lifted investment numbers, especially in the Far East Federal District, but many are now completed or reaching completion. Investment trends have been particularly weak in sectors and regions where exports have been hit hardest by Western sanctions.

Investment turned to decline last year

Russian GDP growth slowed significantly last year. The slowdown was broad-based, but gross fixed capital formation even contracted slightly. The years 2022–2024 witnessed historically high fixed investment growth averaging 9 % a year. National accounting figures show investment stalled, contracting by 0.4 % last year. Total fixed investment amounted to around 50 trillion rubles ($600 billion), which corresponds to roughly 23 % of GDP.

Detailed investment figures are prepared using slightly different principles than the national accounts. In the more nuanced figures, the volume of investments contracted by 2 % last year. The total value of investments in 2025 was roughly 43 trillion rubles. Of that, 80 % represented investment by larger firms that report their investment to the statistical office. The remaining 20 % consisted of the Rosstat estimate of investments by small firms or other investments not directly tracked in the data.

There was a general slowdown in investment growth last year. The most dramatic shifts in the numbers reflected completion of large infrastructure projects in regions of the Far East Federal District financed at least partially from budget resources. The transport, warehousing and logistics sector saw investment dry up last year. The volume of investments in land and pipeline transport and warehousing contracted by nearly a third. Investment volume declined in all of Russia’s federal districts other than the Northwestern and Central Federal Districts. The value of investments financed directly from the budget decreased slightly even in nominal terms.

Investment spending continued to increase last year in the chemicals industry and in industries supporting the war effort. Among the fastest growing industries were manufacture of other transport equipment, a category that includes military fighting vehicles (investment volume up by 60 %) and chemicals industry (up 30 %). Regions with the highest investment growth rates included the Leningrad oblast, where growth was led by the chemicals industry, as well as in the Jewish autonomous okrug and the Chukotka autonomous okrug in Russia’s Far East Federal District, which experienced strong growth from the mining industry and infrastructure projects.

War years transform investment structure

The structure of Russian fixed investment has changed in many ways in recent years. The share of construction in investment has increased, last year reaching 55 %, its highest share in 2000s. At the same time, the share of investment in machinery & equipment has declined significantly, representing just a third of investment last year. The share of intangible investment (e.g. software development, R&D) has increased gradually in recent years, reaching around 7 % in 2025.

Companies have increasingly relied out-of-pocket financing for their investments with the share already 59 % last year, the highest share this century. The share of direct budget funding as an external funding source has decreased considerably from its peak in 2022. Foreign financing for investment has collapsed. The share of investment from foreign-owned firms fell to around 1 %, its lowest level of the millennium. The share of bank loans and other borrowed money in investment financing has grown slightly. The share of “other sources” of financing has experienced sharpest contraction in recent years, but detailed information on such sources is unavailable.

Investment trends have varied widely across sectors in recent years. Manufacturing’s contribution, led by war-related technology industries and the chemicals industry, reached an all-time high of 18 % last year. Investment growth was also rapid in construction, programming and engineering services, as well as branches serving the tourism industry. Investment saw a particularly large decline in branches related to the forest industry. Investment in these sectors was down 30–40 % last year in comparison to pre-invasion years. The share of investment in the oil & gas industry has also decreased significantly in recent years.

Certain regions in the Far East and Siberian Federal Districts have experienced some of the country’s highest fixed investment growth in recent years. Other pockets of growth include the Leningrad Oblast in the Northwestern Federal District, the Volgograd Oblast in the Southern Federal District and the Tatarstan Republic in the Volga Federal District. Investment has been boosted by infrastructure projects and military-industrial investments. The government also provided support for development of the tourism sector in Dagestan on the Caspian Sea. Investment have declined particularly in many Russia’s western and northern districts, including the Komi Republic, Yamalo-Nenets Autonomous Okrug as well as the Murmansk, Kemerovo and Lipetsk oblasts. In many of regions with weakest investment development, sanctions have reduced export demand for key industries (e.g. Western restrictions on imports of wood, coal and metals) or made it more difficult to implement investments (e.g. Western restrictions on the sale of LNG production technology to Russia).

Financing challenges and uncertain demand outlook depress investment

One of the most important factors restricting investment mentioned in recent business surveys has been the lack of in-house funds available to finance investments. Corporate profits shrank last year for the second year in a row. Rosstat reports corporate profits overall fell by 4 % last year. At the same time, the tax burden on companies increased as the corporate profit tax was raised from 20 % to 25 % at the beginning of 2025, a change that boosted profit tax revenues to the consolidated budget by 15 % last year. In any case, corporate profits last year were still significantly larger than in the years preceding the Covid-19 pandemic. The government is currently preparing another windfall tax on 2025 corporate profits. That tax would have to be paid this year. The tax as planned would be 20 % of the amount exceeding the firm’s average earnings in 2018–2019.

Respondents also often cited high interest rates as a factor limiting investment. The interest rate on corporate loans over a year peaked at nearly 20 % last year, then gradually declined towards the end of the year as the Central Bank of Russia (CBR) lowered its key rate. The average interest rate on ruble-denominated corporate loans of more than one year was 16 % last year. The state offers significantly cheaper credit or interest subsidies for investment projects of strategic importance.

General uncertainty about economic conditions and lack of demand are also significant factors depressing investment. A regular survey of industrial firms by the Institute of Economic Forecasting of the Russian Academy of Sciences (INP RAN) showed in March that companies considered demand to be the weakest since the pandemic. The CBR’s business survey found that capacity utilisation last year declined in all parts of the economy. A big drop was recorded in manufacturing, especially manufacturing of investment goods and semi-finished products. No detailed branch-specific breakdown is provided. Rates of capacity utilisation have also declined in the transport and warehousing branches. In these industries, the capacity utilisation rate has already returned to pre-war levels.

Fixed investment is expected to remain weak this year. Responses to the latest CBR business survey indicate that investment continued to decline in the first quarter of this year. Companies noted that their investment levels were as weak as at in early 2022. Mining & quarrying firms (includes oil & gas) reported that their investment levels were at their weakest level since the global financial crisis of 2008–2009. The future investment expectations of companies have also weakened significantly this year. In its February forecast, the CBR said it expected fixed investment to increase by 0–2 % this year. The April report from Consensus Economics found that the average investment forecast for this year is 0.4 %.