BOFIT Weekly Review 7/2022

Strong growth in bank lending fuels Russian domestic demand

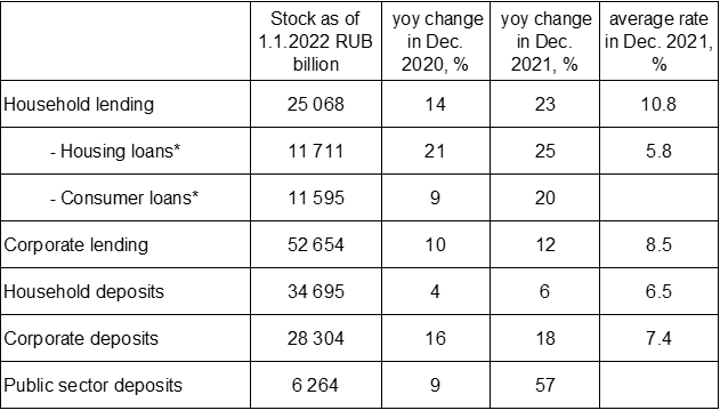

The stock of household loans grew last year by 23 % and the stock of corporate loans by 12 %. Growth in housing loans remained brisk, thanks in part to continued policy measures to support mortgage borrowers. As a result, the interest rate on loans for newly constructed housing has remained remarkably low. In December, a quarter of new housing loans qualified for government loan subsidy programmes.

While rapid growth in consumer credit has supported domestic demand, the pace of growth has heightened concerns about the ability of borrowers to make their payments. The CBR has sought to quell growth in consumer credit through tightened macroprudential regulations. While these measures have yet to have much impact on slowing growth in consumer credit, the combination of macroprudential measures and central bank rate hikes is expected to reduce growth rates in the coming months.

The CBR suggests that the current rapid growth in corporate credit may reflect a revival in fixed investment demand. The household credit stock is almost entirely denominated in rubles, while about 23 % of corporate loans are in foreign currencies (mainly euros or dollars).

Corporate deposits rose significantly last year, partly reflecting improved corporate profitability due to higher export prices. The stock of household deposits grew slightly faster than in 2020. The rise in rates paid on deposits and volatility in stock and bond markets increased the popularity of bank deposits, especially in the final months of last year. About 20 % of household deposits and 30 % of corporate deposits are in foreign currencies.

Increased loan demand helped boost banking sector profitability, which was up by about 50 % from 2020. In addition to growth in income from interest, commissions and fees, moderate level of provisioning boosted the sector’s profits last year. When the covid pandemic hit in 2020, banks significantly increased their loan loss reserves. So far, however, rapid economic recovery and various payment extensions and government interest subsidies have kept credit losses at low levels. The share of non-performing corporate loans fell substantially last year.

Bank lending and deposits were up sharply in 2021

Sources: Central Bank of Russia and BOFIT.