BOFIT Weekly Review 18/2025

Yuan-dollar exchange rate settles after April plunge

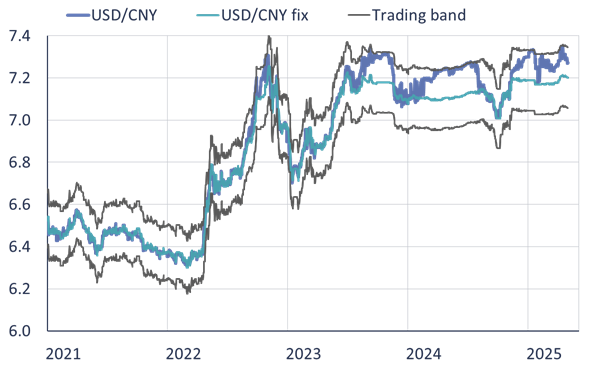

The yuan’s exchange rate against the US dollar fell sharply in early April following president Trump’s announcement of retaliatory tariffs, only to fall again in mid-April as the tariff rhetoric stiffened. Over the past two weeks, the yuan-dollar rate has stabilised at around 7.3 yuan to the dollar. The yuan’s offshore rate (CNH/USD) in Hong Kong forex trading has closely tracked the onshore (CNY/USD) rate. The yuan-dollar rate currently stands at the same level as when Trump took office in January. Because the dollar has recently declined against the euro and the currencies of several other advanced economies, the yuan has lost considerable ground against these currencies. On Friday (May 2), for example, one euro bought 8.24 yuan, a 9 % increase from the yuan’s 7.58 rate at the end of February.

China’s exchange rate policy has long been anchored in the yuan-dollar exchange rate. The People’s Bank of China currently regulates the yuan-dollar rate with its daily fixing rate from which the yuan’s value can diverge by 2 % up or down. In practice, the yuan’s exchange rate against other currencies tracks its performance against the dollar. The yuan’s rapid devaluation forced the PBoC to act as the yuan hit its 2 % bound. The central bank was either forced to sell dollars from its own reserves to prevent excessive weakening of the yuan or provided guidance requiring commercial banks to reduce their dollar positions. Media reports suggest that commercial banks, and possibly others, have been asked to reduce their dollar purchases. The rumour on bond markets that China was selling large amounts of dollar assets to disrupt the US treasuries market, however, is likely unfounded. Even if China has sought to diversify its reserve assets for years, it still holds a substantial portfolio of US government bonds. It is difficult to see China’s policymakers spiting themselves by reducing the value of their holdings. In addition to the central bank, commercial banks and other economic entities hold significant dollar assets.

While China is expected to relax its monetary stance to support economic growth and modestly increase current zero-inflation, the PBoC has been extremely reluctant to adopt accommodative measures. Interest rate cuts could aggravate capital flight as other countries would be offering relatively better yields on capital investment. Capital flight would place downward pressure on the yuan’s exchange rate, a situation the central bank wants to prevent. On the other hand, allowing the yuan to fall in the current situation could mitigate some of the impacts from high tariffs.

Yuan-dollar exchange rates: daily fixing rate (fix) and allowed fluctuation band limits

Sources: People’s Bank of China, Macrobond and BOFIT.