BOFIT Weekly Review 29/2023

Yuan’s role in Russia’s foreign trade continues to grow

As a result of sanctions and the decision by many Western firms to sever ties with Russia, most major Russian banks no longer can handle payment traffic in dollars and euros. During the war, Russia has tried to move away from the main global trading currencies in its foreign trade. President Vladimir Putin has decreed, for example, that natural gas contracts should be invoiced in rubles. To develop a new export customer base, Russia is offering deep discounts in crude oil and petroleum products, with the option of paying for the purchases in other currencies.

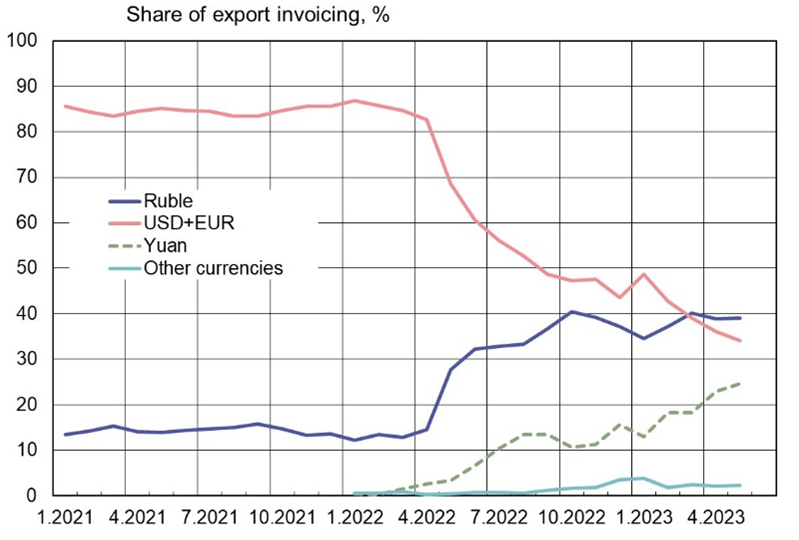

For the first time since Russia’s invasion of Ukraine last year, the Central Bank of Russia has released a breakdown of Russia’s foreign trade payments. According to the data, the share of currencies of “unfriendly” countries (mainly the US dollar and euro) in invoicing exports of goods and services had declined to about a third, while the ruble’s share had climbed to nearly 40 %. All other currencies accounted for just under 30 %.

There has been a substantial change over the past two years. Before the invasion, the combined share of the dollar and euro in export invoicing was about 85 %, with the ruble’s share at just over 10 %. The “other currencies” category, which includes the Chinese yuan, the Indian rupee and the UAE dirham, was close to zero, but today exceeds 25 %. The “other currencies” component is especially large for Russian exports to countries in Asia (34 %) and Africa (32 %). Elsewhere, “other currencies” are rarely used in trade with Russia. The trading currency data release in conjunction with the CBR’s latest financial market stability report suggest that Chinese yuan’s portion of the “other currencies” in payments was overwhelming. Indeed, the yuan’s share in export invoicing already reached 25 % in May.

The data also fit with reporting on the shift in oil exports to Asia (including China and India) to the use of currencies other than the US dollar in payment. It is worth remembering that Russia’s main export products are still basic commodities, the price of which at generally set in US dollars. Therefore, in many cases, the invoicing currency in Russian exports differs from the currency used in price-setting. Moreover, payment of oil & gas taxed to Russia’s federal budget are still based on oil prices in US dollars. The US dollar remains unchallenged as the global reserve and pricing currency, so even large changes in Russia’s foreign trade practices can only have a negligible impact.

In the last 15 months, there has been a significant shift in Russian foreign trade payments in favour of the ruble and yuan

Sources: CBR balance-of-payments payment currency data (CBR credit statistics Excel file download) and CBR financial market stability report 6/2023 (in Russian).

Sources: CBR balance-of-payments payment currency data (CBR credit statistics Excel file download) and CBR financial market stability report 6/2023 (in Russian).

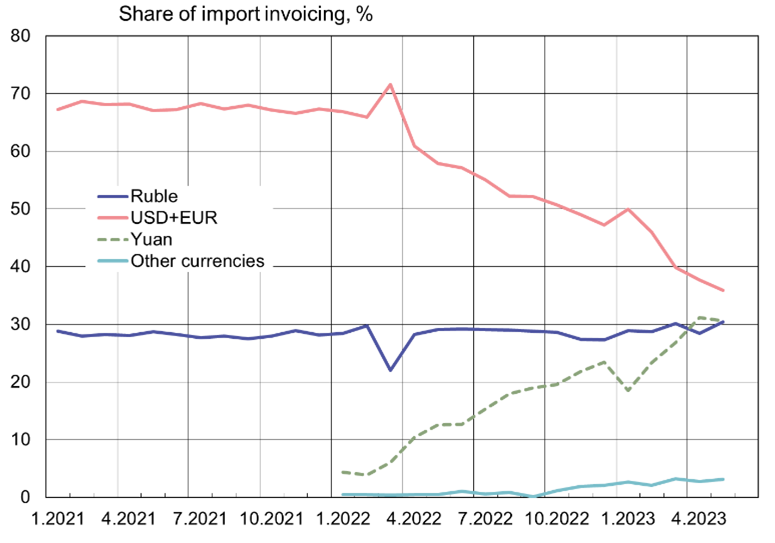

Yuan increasingly used as invoicing currency for Russian imports

With the shift in geographic emphasis of Russian imports to Asia, the use of the yuan as an invoicing currency has grown significantly. Prior to the war, the dollar’s share of imports was about 35 %, the euro’s share approximately 30 % and all other currencies only a few percent at most. In May, the combined share of the dollars and euro in import invoicing was only a bit more than a third, while the yuan’s share had climbed to about 30 %. The change highlights the geographic shift in trade; Russia’s EU imports are only about half their pre-war levels.

The yuan appears to have replaced Western currencies in Russia-China bilateral trade. While Russia currently has stopped releasing country-level data, about 70 % of Russia’s imports from China in 2021 were paid for in Western currencies and about 25 % in “other currencies” (mostly yuan). The CBR reports that only about half of May imports coming from Asian countries were invoiced either in rubles or Western currencies. Unlike in exports, Russia has not succeeded in increasing ruble use in imports. For the months of April and May, the yuan’s share in invoicing was already larger than the ruble’s share. Most payments for imports coming from member countries of the Eurasian Economic Union have historically been paid for in rubles.

Use of the dollar and euro in Russian imports has also decreased steadily over the past 15 months

Sources: CBR balance-of-payments payment currency data (CBR credit statistics Excel file download) and CBR financial market stability report 6/2023 (in Russian).

Sources: CBR balance-of-payments payment currency data (CBR credit statistics Excel file download) and CBR financial market stability report 6/2023 (in Russian).

The CBR reports that at the monthly level payments for imports in euros and yuan have been larger than export revenues in these two currencies, implying that a portion of ruble- and dollar-based export revenues have been converted to yuan and euros. Russia’s efforts to move away from dollar-based trade and find different import providers have clearly boosted demand for Chinese yuan inside Russia. The yuan was only introduced as a traded currency on the Moscow Exchange’s foreign currency market a year ago, but its share of trading has grown steadily. In June this year, ruble-yuan trades represented 36 % of currency market trading in Russia. The other top currency pairings still involve dollar or euro. In addition, the CBR’s forex operations under the government’s fiscal rule are currently conducted in yuan.

The yuan’s importance in the banking sector is still limited, but growing. For example, corporate forex deposits not denominated in dollars or euros have risen from close to zero last year to about 40 % at present. While the stock of forex loans has generally shrunk, its composition has changed considerably. Share of loans issued in “other currencies” has risen to about 20 %. Although the reporting does not give a detailed breakdown of currencies, the yuan apparently dominates the “other currencies” category. Broader use of the yuan is impeded by the fact that the yuan is not a freely convertible currency. The yuan only accounts for a few percent of global currency trading and over-the-counter (OTC) derivatives trading conducted by banks (BOFIT Weekly 24/2022). In addition, large Chinese banks are extremely wary of doing business with counterparties subject to sanctions.