BOFIT Weekly Review 12/2018

Chinese economy powers ahead in first two months of 2018

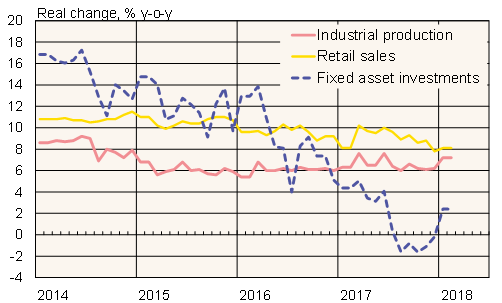

Real industrial output rose by 7.2 % y-o-y in January-February – the highest January-February industrial output figure since 2014. Fixed asset investment (FAI) in urban areas rose about 8 % y-o-y in nominal terms in January-February, or one percentage point less than in the same period in 2017. On-year real FAI growth was around 2 %, assuming that inflation’s impact on January-February investment was slightly lower than in the 4Q17.

Retail sales grew by nearly 10 % y-o-y in nominal terms in the first two months of this year. Online sales were up 37 % y-o-y, with online now accounting for about 15 % of all retail sales of consumer goods. While the nominal growth in retail sales was slightly higher than in the first two months of 2017, higher inflation held real growth to about 8 %.

The rise in consumer prices accelerated in February to 2.9 %, while the January figure was 1.5 %. The Chinese Lunar New Year fell this year in February, causing a rise in prices of certain consumer products. The February core inflation reading, which excludes food and energy prices, rose by 0.5 percentage points from January to 2.5 %. Producer price inflation continued to cool, falling from 4.3 % in January to 3.7 % in February. On-year growth in producer prices slightly exceeded 6 % on average for months in 2017.

Chinese industrial output, retail sales and fixed investment*

* January-February 2018 investment trend based on price estimate

Sources: Macrobond, CEIC, BOFIT.