BOFIT Weekly Review 50/2025

Chinese developers enter fifth consecutive year of financial struggles

In recent weeks, China Vanke, once China’s largest property developer, has been making headlines. The Shenzhen-headquartered company recently sought to postpone repayment of two onshore bonds maturing this month (a 2-billion bond due on December 15 and a 3.7-billion yuan bond due on December 28). The company’s financial problems began to spiral in September when the company’s largest shareholder, local-government owned the Shenzhen metro, announced that it was tightening is financing to Vanke. The Shenzhen metro had earlier supported Vanke with substantial capital loans. It appears that Vanke also failed to get a loan from large commercial banks to pay down bond debt.

In previous years, other giant property developers, including Evergrande, failed when they were crushed by indebtedness. In January 2024, a Hong Kong court ruled against Evergrande on a winding-up petition, forcing a liquidation. As the lion’s share of company assets are on the mainland, however, it has been challenging for creditors to make much headway in enforcing the liquidation ruling of the Hong Kong court. This year, however, several Evergrande subsidiaries filed for bankruptcy in mainland China. The Hong Kong court’s liquidators also suspect Evergrande’s founder and chairman Hui Ka Yan of hiding company assets. In September, the court ordered Hui to surrender his personal assets to Evergrande’s liquidators. In addition, the funds of certain persons associated with Evergrande’s management have had their assets frozen.

Many of the other large developers have continued with debt restructurings this year. Among them, Country Garden, Sunac, R&F, Kaisa and Shimao have made forbearance agreements with their creditors. Such debtors have typically been required to significantly reduce and postpone their receivables and in some instances exchange company shares for debt. These arrangements are seen as important in helping these companies secure their futures. For example, Country Garden, which restructured its debt in November-December has been placed in receivership by a Hong Kong court with the matter set to be tried in January 2026.

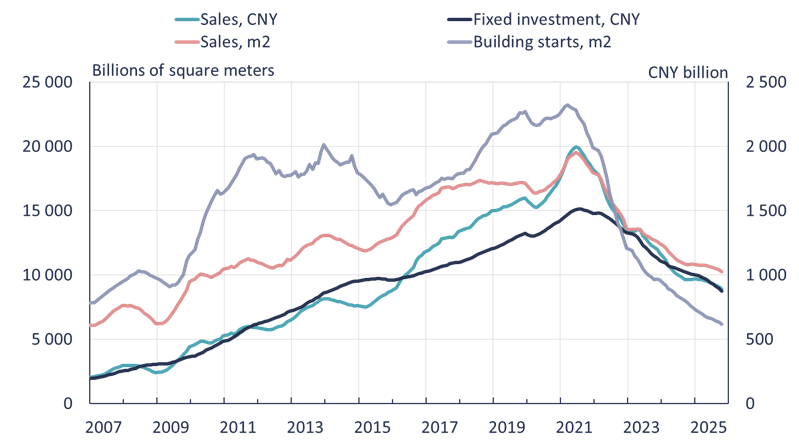

The financial struggles of property developers increased rapidly in 2021 when the authorities imposed three “red line” ratios to limit developer indebtedness (BOFIT Weekly 6/2021) and reduce risk in the sector. The restrictions on the overheated sector caused a severe contraction in the entire real estate sector over the next four years. And the downward spiral continues. In recent months, construction investment has declined by about 20 % y-o-y in nominal terms, while the volume of apartment sales (measured in square metres of floorspace) has also contracted by 20 %. The volume of new building starts has fallen by 30 % y-o-y. At the same time, a large number of properties under construction are still being completed in weak market conditions, and the volume of unsold properties (by floorspace) has continued to grow. The NBS reports new apartment prices have fallen by 10 %, while apartment prices on secondary markets are down 20 % from their 2021 peak. Anecdotal evidence suggests that the drop in apartment prices might have been more dramatic, making conditions in the sector a touchy political subject. In November, two large private housing market data companies were apparently ordered to cease releasing data.

Chinese officials have sought to stem the plunge of the real estate sector for several years with little success. Recently, new ways to support the market have been discussed such as interest subsidies for first-time apartment-buyers, income tax deductions for housing loans and reduction in fees charged in housing transactions. Such measures, however, are likely to be insufficient and contraction of the real estate sector is likely to continue, as available properties are abundant, population is declining and falling apartment prices give little motivation to purchase a new apartment at this time.

China’s real estate collapse continued last year

Note: Observations 12-month moving average.

Sources: China National Bureau of Statistics, CEIC and BOFIT.