BOFIT Weekly Review 18/2025

BOFIT forecast anticipates weaker Chinese economy as trade war escalates

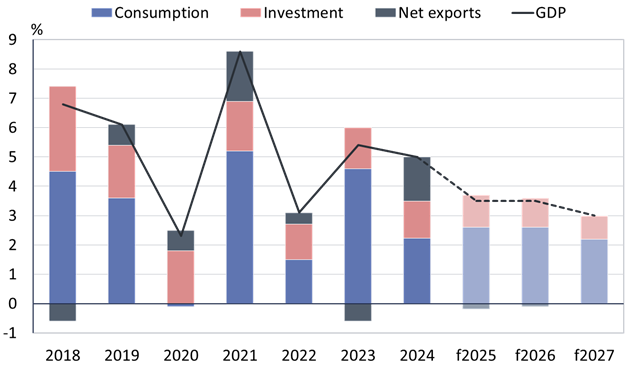

On Monday (Apr. 28), we released our latest BOFIT Forecast for China 2025–2027. The overall outlook has not changed from our earlier forecasts. China’s economy continues to slow, mainly due to the structural realities of its domestic economy. The heating up of the trade war with the United States, however, has fostered considerable uncertainty, degraded export prospects and impaired the domestic growth outlook. We expect actual GDP growth of around 3½ percent this year and next, then a decline to around 3 percent in 2027, the final year of our forecast period.

Domestic consumption in recent years has remained modest and domestic production growth has outstripped demand growth. Fixed investment has been directed to manufacturing, increasing China’s production capacity. China exports the excess production, which is well reflected in the rapid growth in exports that supported economic growth last year and the first quarter of this year. The combination of the US-China tit-for-tat imposition of unprecedentedly high tariffs on each other last month and uncertainty caused by erratic US trade policies have been a major shock to export demand. Growth in global demand, not just in US, is expected to slow this year due to US tariff policies and increased uncertainty. The situation for Chinese firms is significantly more difficult that in president Donald Trump’s first term. We expect China’s export growth to slow during the forecast period. The contribution of net exports to GDP growth should remain negative this year and well into next year.

We expect China to increase economic stimulus measures, thereby also increasing the magnitude and risks related to its public sector imbalances. We expect fiscal policy to be eased more than what was envisioned in the budget approved at the National People’s Congress in March. Policymakers at the politburo’s economy meeting last week (Apr. 25) predictably called for additional stimulus as needed and monetary easing over the course of this year in order to deal with the rising negative impacts on growth caused by external shocks. The readout from the meeting repeated the need for increasing incomes of middle- and low-income households in order to boost domestic consumption. Nothing about concrete measures or their possible timing was mentioned, however. Recovery in domestic demand under current economic conditions is critical for maintaining sustainable growth.

Our forecast reflects high uncertainty. External risks have increased significantly due to an extremely fluid trade policy situation and heightened geopolitical risks. Financial market risks are rising due to decreased profitability in the banking sector and a poor outlook for regional finances. Economic growth could also exceed our expectations for the forecast period if the government decides to apply more stimulus than currently envisioned or the US and China somehow manage to smooth over their trade differences. China remains committed to its ambitious “about 5 %” GDP growth target for this year. As a result, official growth figures are likely to show growth higher than in our current forecast.

China’s GDP growth, main factors contributing to growth and BOFIT’s China forecast for 2025–2027

Sources: China National Bureau of Statistics and BOFIT.