BOFIT Weekly Review 17/2023

Russian industrial output grew in March; detailed 2022 GDP data released

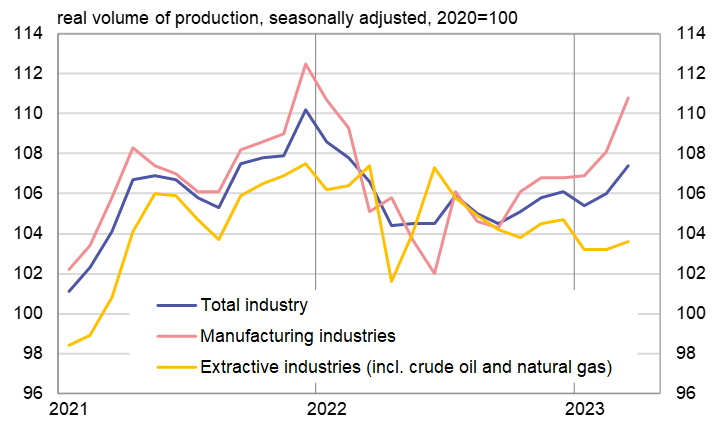

Russian industrial output has increased significantly in recent months. Industrial output was up in March by over 1 % from a year earlier. The gains came largely from manufacturing (up by over 6 % y-o-y). Growth continued to be driven by production of foods, metals and metal products, electronics and vehicles other than automobiles. Much of the growth came from the state orders for e.g. national defence.

Russia’s manufacturing output has risen considerably in recent months.

Sources: Rosstat and BOFIT.

NEW DATA SHOW RUSSIAN GDP BEGAN TO RECOVER IN THE SECOND HALF OF LAST YEAR

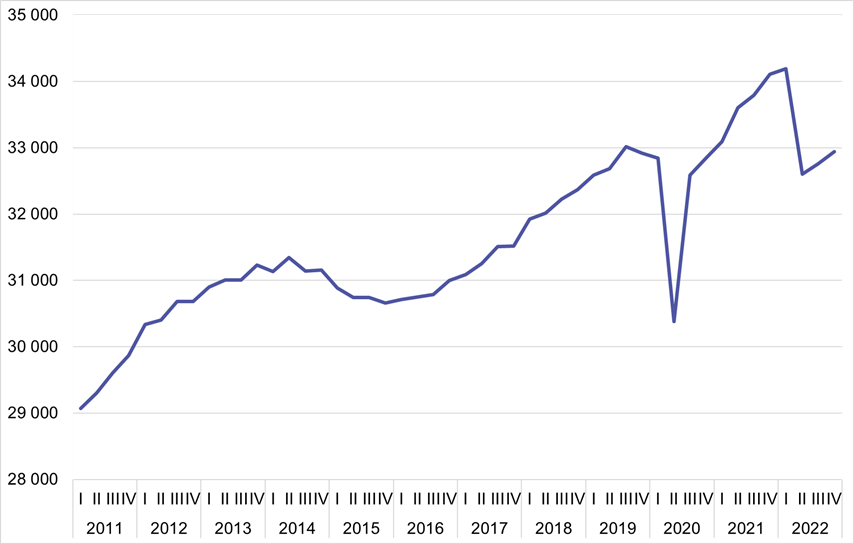

According to just-released Rosstat figures, Russian GDP contracted quite sharply in the second quarter of 2022 following Russia’s invasion of Ukraine and the resulting increased uncertainty and sanctions. Seasonally adjusted GDP fell by 4.6 % from the first quarter. GDP grew by 0.5 % q-o-q in both the third and fourth quarters.

During the first wave of the Covid-19 pandemic in 2020, Russian GDP contracted by 7.5 % in the second quarter, but grew by 7.3 % in the third quarter with the easing of covid restrictions. The latest batch of statistical data is not directly comparable to earlier figures. The newest GDP figures use 2021 prices, while earlier releases are based on 2016 prices.

The development of the Russian economy across production branches was quite uneven in late 2022. In 4Q22, GDP overall contracted by 2.7 % y-o-y. The value added of public services was up by 7.6 % y-o-y, and strong growth was seen in agriculture (up 6.4 %), construction (6.1 %) and hotels and restaurants (6.5 %). Other branches saw sharp declines in value added in the fourth quarter. Retail and wholesale sales were down by 17.3 % y-o-y. The downturn in manufacturing accelerated to 4.8 % and the drop in transport was 4 %.

Russia’s seasonally-adjusted GDP in the fourth quarter of 2022 fell by 3.7 % from the first quarter of 2022.

(RUB billion in 2021 prices)

Source: Rosstat.

INCREASES IN CERTAIN CONSUMPTION CATEGORIES MODERATED LAST YEAR’S DIP IN PRIVATE CONSUMPTION OVERALL

In the revised 2022 GDP figures released this month, some features of last year’s economic performance stick out, including the remarkably shallow dip in private consumption. According to adjusted figures, consumption contracted by just 1.4 %. The large drop in retail sales, the largest private consumption category, was partly offset by growth in other consumption categories. Growth in sales of services softened the real term pullback in household spending on domestically sold goods and services to about 4.5 %.

Travel imports, i.e. the goods and services purchased by Russians abroad, rose at least by one half in real terms as the number of Russians travelling from the country was far above normal. They also bought more and stayed abroad for longer times (in national accounts the persons staying abroad remain households of their home country until they reside more permanently in another country).

The figures for total private consumption and the abovementioned categories of private consumption indicate other consumption categories saw significant increases in 2022. The other items first and foremost include natural (in kind) consumption, consisting essentially of household agricultural production for own final consumption, services arising from living in one’s own home as well as labour income received in the form of goods and services. The share of the other categories in private consumption is significant (about 15 % in 2014−2020 and 17 % in 2021).

According to the latest GDP data, fixed investment rose by 3.3 % y-o-y (down from the increase of more than 5 % announced earlier). This bolsters the view that while government budget sector investment increased sharply investment by other sectors, i.e. companies and households, performed tepidly and may have declined.

SOME DIFFERENCES IN FORECASTS FOR RUSSIA

Differences in recent forecasts for the Russian economy largely reflect the current uncertainty. In its April forecast, the IMF said it expects GDP growth to recover from last year’s roughly 2 % drop to a rise of 0.7 % this year, and GDP attain the 2021 level by 2024. The March forecasts of the OECD and European Bank for Reconstruction and Development (EBRD) see Russian GDP declining by 2.5−3 % this year. April consensus forecasts also predict a mild contraction in GDP though also with differences (Consensus Economics expects a drop of 0.9 % this year, while the consensus forecast compiled by the Bank of Russia only sees a decline of 0.1 %).

One reason for the IMF’s rather favourable outlook is an expected easing in government finances when measured in terms of the budget deficit. The IMF expects the deficit to increase to over 6 % of GDP this year (-2.2 % last year). The consensus forecasts see smaller deficits (the CBR consensus forecast for the balance of the government budget sector overall is -2.6 %, while the Consensus Economics forecast for the federal budget shows a deficit of 3.6 %). The federal budget, which is where the government budget sector deficit is concentrated, showed the deficit widening sharply in January-February. In March, the deficit of last 12 months was about 4.5 % of GDP.