BOFIT Weekly Review 42/2023

Growth of China’s economy appears to be stabilising

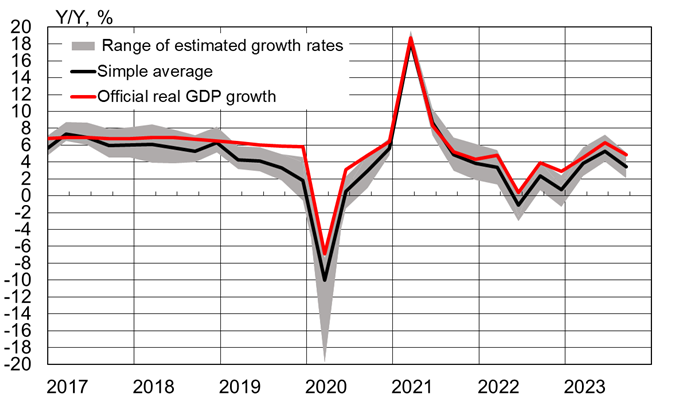

China National Bureau of Statistics reports that the country’s GDP grew by 4.9 % y-o-y in the third quarter, down from an average of 5.5 % in the first six months of this year. Third quarter growth reached 1.3 % q-o-q, well above the on-quarter growth of 0.5 % p0sted in the second quarter. Uncertainty over the reliability of official figures has increased as the economy has slowed. BOFIT’s alternative calculation indicates that real GDP growth slowed substantially in the third quarter and the growth might have been well below the official assessment. Other regularly updated alternative calculations of Chinese growth also undershoot official figures. Fourth-quarter GDP on-year growth is expected to be higher than the third quarter as it will be referenced to the fourth quarter of 2022 when China was in the midst of Covid-19 lockdowns.

BOFIT alternative calculation of Chinese GDP shows a distinct third-quarter slowdown

Sources: China National Bureau of Statistics, Macrobond and BOFIT calculations.

Increased consumption has been the biggest driver of growth this year. It gained more traction in the third quarter, when consumption accounted for 4.6 percentage points of GDP growth. During the pandemic years and first half of this year, households squirreled away larger share of their disposable income than usually. In the third quarter of this year, however, households began to spend a larger share of their earnings. The highest growth was seen in services hardest hit by covid restrictions. Households have spent considerably more on domestic travel, restaurant services, healthcare and cultural activities, entertainment and education. During the Golden Week autumn break at the start of October, tourism was up sharply from a year earlier. The volume of domestic tourism, however, was up by just 4 % from 2019 and consumer spending less than 2 % higher than in 2019.

Contraction of the real estate sector continued throughout the third quarter. For July-September, the volumes of housing sales and new construction starts measured in terms of floorspace fell by 22 % y-o-y. The downturn in property construction put the brakes on investment growth, with investment contributing just 1.1 percentage points to GDP growth in the third quarter. The government’s limited economic support measures have mainly targeted apartment sales. The real estate sector, however, is likely to struggle as uncertainty about the economy continues to depress demand.

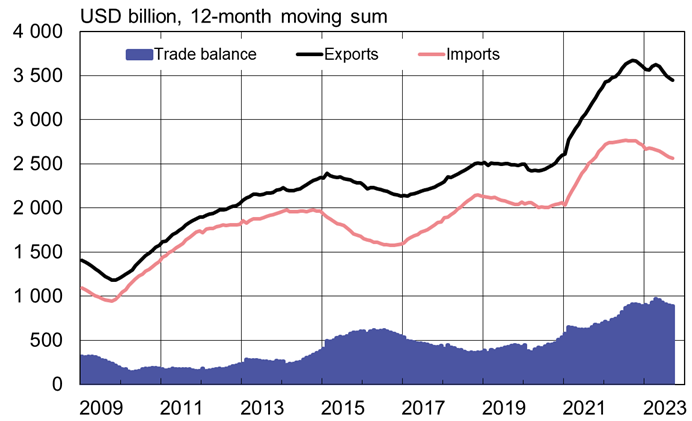

WEAK FOREIGN TRADE PICTURE PERSISTS

The value of Chinese September exports measured in dollars contracted by over 6 % y-o-y. In the third quarter, exports overall fell by 10 % y-o-y. The value of imports in dollars also contracted by over 6 % in September, and was down by 9 % in the third quarter. Even if the trade numbers looked gloomy, the contractions of exports and imports in September were smaller than in August.

The yuan’s depreciation explains some of the contraction in the dollar-value of China’s foreign trade. Yuan-denominated trade statistics show a smaller decline in both the value of exports and imports. Nevertheless, China’s foreign trade unquestionably has been struggling with weak demand on the both the domestic and international fronts. The United States and Europe, China’s most important export markets, are experiencing lower economic growth while uncertainty about China’s economic prospects and weak domestic demand are reflected in reduced imports.

A closer look at China’s individual trading partners reveals that the rising trend in China’s trade with Russia is at odds with the declines seen for practically all other countries. In dollar terms, the value of China’s exports to Russia rose by 28 % y-o-y in the third quarter, while imports held steady at last year’s level, growing at about 1 %. Another interesting outlier shows up among China’s foreign trade product categories. Although exports overall are declining, China’s global vehicle exports are booming. Annual growth measured in dollars exceeded 50 % y-o-y in the third quarter.

China’s foreign trade has decreased from last year

Sources: China Customs, CEIC and BOFIT.

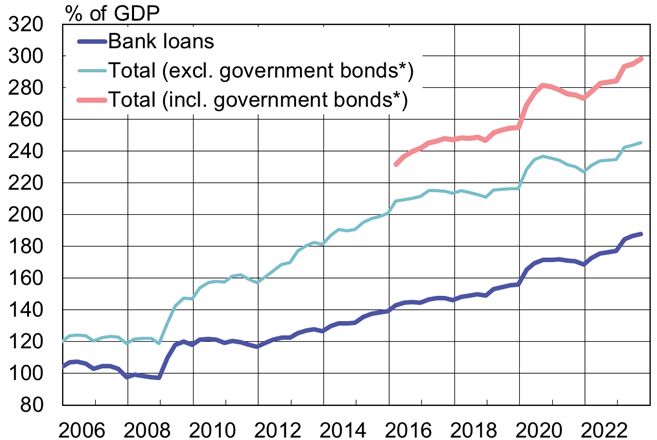

Public indebtedness Drives UP debt-to-GDP ratio

Despite a modest easing in monetary policy during August and September, growth in China’s domestic indebtedness remained relatively flat due to low demand for financing. Because nominal GDP grew by just 4 % over the previous 12-month period, the ratio of borrowing to GDP still rose. In September, the People’s Bank of China’s total domestic debt measure – aggregate financing to the real economy (AFRE) – grew as in previous months at a pace of 9 % y-o-y and exceeded 298 % of GDP. On-year growth in the stock of yuan-denominated bank loans remained just over 11 % in September. A quarter of the lending stock is consisted of household loans, which only grew by about 3 %.

Government debt in the AFRE measure includes general bonds issues of the central and local governments, as well as special-purpose bonds issued by local governments. The stock of government bonds grew by 12 % y-o-y in September to a level equivalent to 53 % of GDP. The IMF notes that when the off-budget debt of local governments and indebtedness of state funds are taken into account, China’s public debt is considerably higher (estimated at 110 % of GDP as of end-2022). The government has recently sought to deal with off-budget indebtedness of local governments by a debt-swap program, making it possible for local governments to pay off off-balance-sheet debt by issuing bonds to make the situation more transparent. According to media reports, the government also this month encouraged large state banks and policy banks to increase lending at attractive rates to local governments and their off-budget local government financial vehicles (LGFVs) to pay off their high-interest loans. According to state media, the agenda of the CPC standing committee meeting that began today (Oct. 20) includes a discussion of provincial finances and the possibility of again allowing local governments to use next year’s quotas in advance. Provincial finances are typically stretched in the second half of the year. As of end-August 2023, local governments had already issued 76 % of their annual quota of 720 billion yuan in general bonds and 83 % of their 3.8 trillion yuan quota for special-purpose bonds. Earlier in October, Bloomberg reported that China’s central government was considering issuing additional sovereign debt of at least 1 trillion yuan.

China’s aggregate financing to the real economy (AFRE) currently stands at nearly three times gross domestic product

*) Bond issues of central and local governments. The IMF estimates China’s actual public liabilities as of end-2022 at 110 % of GDP.

Sources: PBoC, CEIC and BOFIT.