BOFIT Weekly Review 2/2016

Russian stock market performance reflects low oil prices and ruble slide

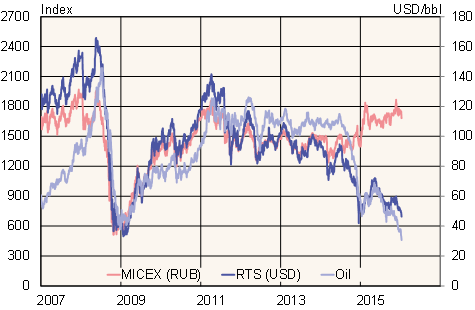

Russia’s main RTS share index, calculated in dollars, fell 4 % last year on the drop in oil prices and the ruble’s weak exchange rate. The decline in the RTS index last year remained modest, however, as it had already fallen 45 % in 2014. The index largely follows the price of oil, as companies in the oil & gas sector account for about half of weight of the index. While the total market capitalisation of companies included in the RTS index has slumped about 50 % from peak years, it was still above $100 billion last year. That amount is about double the RTS market cap during the 2009 financial crisis.

In contrast, the Moscow exchange’s MICEX index, calculated in rubles, rose 23 % last year. Although the price of oil has fallen below 2009 levels, the impact on the ruble-denominated index has been softened by the adjustment of the ruble’s exchange rate. The ruble’s weakening has supported the profitability of export firms despite falling prices for oil and other commodities. Revenues of export firms are mainly denominated in foreign currencies, while most of their spending is in rubles. Moreover, the sub-index for state-owned enterprises was up 31 % last year, beating the MICEX overall. Finance was an above-average-performing category, while metals clearly underperformed the MICEX average.

The year’s trading volume on the Moscow stock exchange contracted slightly last year to 9.4 trillion rubles, about half the peak level of 2011, but still above the 2013 nadir.

Russia’s main share indices and the oil price

Source: Macrobond.