BOFIT Forecast for China 2026–2028

1/2026, published 5 May 2026

Official figures show that China’s economy expanded by 5 percent last year, although actual GDP growth was likely lower. With domestic consumption and fixed investment remaining subdued, economic growth continues to rely heavily on exports. Room for fiscal stimulus has narrowed, and economic policy has been geared to supporting exports. China produces significantly more than it consumes, and the trade surplus is expected to remain large throughout the forecast period. We expect China’s actual economic growth to stay around 4 percent this year, and, due to the reduced boost from exports, growth should slow to around 3½ percent in 2027 and about 3 percent in 2028. Rising internal and external economic imbalances, which add to the risks associated with the forecast, are reflected outside China as intensified competition and heightened trade tensions.

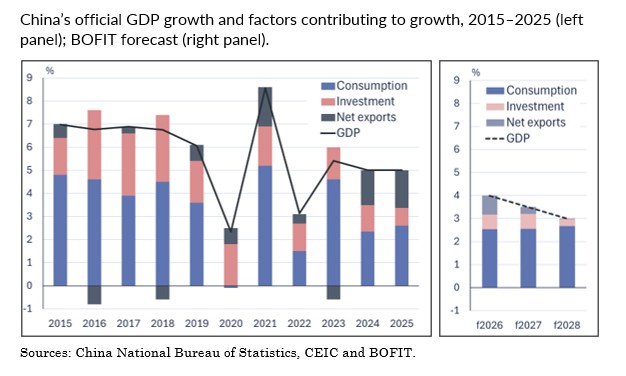

Keeping with the government’s official growth target, China’s National Bureau of Statistics (NBS) reports that GDP grew by 5.0 % in 2025. On-year growth slowed towards the end of the year. According to NBS figures, GDP growth also hit 5.0 % in the first quarter of this year. China’s actual economic growth was likely lower. BOFIT’s alternative estimate suggests that GDP growth last year was about one percentage point lower than the official figure, putting it broadly in line with our previous forecast from November. Alternative estimates suggest that GDP growth continued to slow in the first quarter of this year. Chinese goods exports last year clearly exceeded goods imports, increasing rapidly despite high tariffs imposed by the United States. The current account surplus rose to 3.7 % of GDP ($735 billion). Net exports made an exceptionally large contribution, accounting for a third of overall economic growth. Export growth remained strong in the first quarter of this year, while import growth accelerated significantly.

We expect China’s actual economic growth this year to be around 4 %. Compared to our previous forecast from November, the impact of net exports on growth has been greater than expected. We predict net exports continue to support economic growth this year, although their contribution is likely to be smaller than last year and should weaken further during the forecast period. With no significant revival in domestic demand expected, we see economic growth slowing to around 3½ percent in 2027 and around 3 percent in 2028. Although the government has slightly lowered its official growth target this year to a range of 4.5–5 %, the target still exceeds our actual growth expectation. In addition, China’s declared goal of doubling 2020 GDP per capita by 2035 requires growth averaging about 4 % a year over the next decade. Given the great political importance attached to GDP targets, official statistics are unlikely to report distinctly lower growth. Thus, published figures cannot be trusted to give a true picture of underlying economic performance.

No shift in domestic economic policy; demand growth remains subdued

Consumer confidence has remained weak since the zero-covid lockdowns of 2022. Households remain skittish about spending and uncertainty over employment prospects has increased. Youth unemployment has remained high for several years (youth unemployment was 16.9 % in March 2026). As the bulk of household wealth in China is tied up in housing, the downturn in the real estate market, now in its fifth year, has eroded the financial position of households and forced them to increase savings. China’s remarkably high savings rate is to large extent a manifestation of the flimsiness of the social safety net. The pandemic-era rise in the household savings rate persists to this day. Moreover, due to limited foreign investment opportunities, most Chinese only have the option of parking their savings in low-interest bank accounts or investing in the domestic financial sector.

Real growth in retail sales has remained modest, at around 3 % y-o-y in 2025 and slowing to 2 % in the first quarter of this year. Although recent policy guidelines emphasise the need to promote consumption, the measures adopted to achieve this have been modest. Beyond a nationwide subsidy for parents of children under 3 and free pre-school, the government has not made any significant improvements to the social safety net. Support measures have focused instead on stimulating consumer activity, increasing consumption opportunities and subsidising the acquisition of certain durable goods and electronics. Funding allocated to this consumer trade-in program has been reduced this year, and its impact on consumption growth has waned. Consumption is expected to revive slightly during the forecast period, however, supported by increased demand for services from China’s ageing population. Domestic consumption should become an increasingly important driver of economic growth in coming years.

Following decades of investment-driven growth and imbalances accumulated from unprofitable investments, fixed investment growth has slowed markedly. The contraction in real estate investment over the past five years has been particularly large, with 1Q26 investment down by 36 % from 1Q21. The real estate sector’s share of the economy has halved over the past five years.

China’s investment focus has shifted to advanced manufacturing, renewable energy and technological development. The country’s investment in R&D activities has risen rapidly, and now exceeds US R&D spending measured in PPP dollars. China has become a pioneer in an increasing range of sophisticated technologies – a trend unlikely to change. The 2026–2030 five-year plan emphasises support for industrial and technological development, particularly artificial intelligence, 6G technology, robotics, quantum computing and industries supporting the green transition.

Less room for fiscal stimulus

China has run persistently high public-sector deficits as the government has relied on loose fiscal policy to support economic growth for nearly two decades. As a result, additional fiscal stimulus measures are not expected to boost economic growth during the forecast period. Indeed, both this year’s budget and finance ministry plans foresee a slight tightening from last year. The budget deficit is projected to remain at 4 % of GDP (or about 8 % of GDP when state funds are included). Using the IMF definition, the actual public sector deficit, which includes also the activities of local government financial vehicles (LGFVs), is expected to amount to roughly 14 % of GDP, a level similar to last year.

Public sector debt continues to grow rapidly. Including LGFV liabilities, China’s total public sector debt rose last year to 127 % of GDP. Like last year, some of the new debt will be used to reduce financial market risks and recapitalise banks – actions that do not directly generate economic growth. Local governments have taken on new debt to pay down “hidden” debt, i.e. high-interest loans taken by LGFVs. The financial situation of regional governments has been eroded by a severe reduction in income from the sale of land-use rights. In addition, the central government wants to rein in LGFV indebtedness. Despite paying down part of LGFV debt in recent years, a significant number of LGFVs remain outside current government classifications, and total LGFV debt stock has continued to grow.

China has not been spared from rising prices on global energy markets. After over three years of decline, year-on-year growth in producer prices turned positive in March. The government has implemented measures to prevent the full pass-through of energy prices to consumer prices in an effort to insulate households from rising in energy and fuel prices. Weak domestic demand, stiff competition and industrial subsidies should keep overall consumer price inflation modest throughout the forecast period. Despite China’s leaders voicing concerns about involution (slashing prices in the face of excessive competition in industries where market share matters), viable solutions for alleviating the situation have yet to be proposed.

Monetary policy accommodation has remained highly cautious, even if low inflation and macro conditions would permit more robust responses. China’s room to manoeuvre in monetary policy is limited by the fact that domestic interest rates are already considerably lower than those of its main international partners. The People’s Bank of China is likely concerned that any significant rate cut could trigger increased capital outflows. The PBoC lowered its main policy rates once last year, and only by 10 basis points. Monetary policy has become more targeted, with inexpensive financing channelled to selected areas. We expect no major changes in the monetary stance during the forecast period. A further widening of the interest-rate differential relative to the rest of the world would likely increase pressure in China to move capital abroad.

Growing foreign trade surplus increases external imbalances

China continues to increase its global market share. Despite rising international trade tensions, goods exports grew briskly last year. Exports to China’s neighbours and other emerging economies grew rapidly, while a growing share of China’s production for the US market is routed through third countries to avoid US tariffs. Export prices have fallen for three years in row, and export volumes have grown even faster than export values. Growth in goods imports has lagged behind exports due to subdued domestic demand and the government’s emphasis on increased self-sufficiency.

Exports are also expected to grow faster than imports this year. China has invested heavily in fields such as advanced technology and the green transition. Global demand in these fields is expected to climb rapidly, increasing many countries’ dependence on China. In coming years, growth in Chinese exports is expected to fall back to levels closer to global trade growth, while import growth is expected to lag behind growth in domestic consumption. We expect China’s current account surplus to increase further this year and the high surpluses persisting throughout the forecast period.

The strong competitiveness of Chinese producers and ballooning surpluses have increased tensions with trading partners. Industrial policy has been strengthened, which is expected to continue under the current five-year plan. Direct and indirect industrial subsidies in China are clearly larger than most of its trading partners. Subsidies granted by regional governments to local enterprises have intensified domestic competition and given Chinese firms an unfair advantage in international markets. Trading partners are likely to rely on tariff increases and other trade policy counter-measures to level the playing field.

While yuan strengthening would help to reduce external imbalances, significant appreciation of the Chinese currency is unlikely as exports remain an important source of economic growth. The PBoC has kept the yuan’s exchange rate relatively weak, which, combined with low interest rates, has made China less attractive as an investment destination. In recent years, net foreign and domestic capital flowing out of China roughly corresponds to the amount of the China’s foreign trade surpluses. The value of China’s foreign exchange reserves has increased only slightly to around $3.3 trillion.

Rising energy prices could increase the value of imports. Although China is the world’s largest energy consumer and oil importer, the Iran war has had a smaller impact on its economy than most other Asian countries. Oil and natural gas represent a relatively small share of China’s total energy consumption. In addition to significant domestic production, China has taken advantage of lower global oil prices in recent years to build up its strategic reserves, which are currently helping blunt the impact of the global energy shock.

Ample domestic and external risks

As China has made no significant reforms to its economic structure or growth model, the risks generated by rapid indebtedness and unprofitable investments continue to mount. Moreover, local governments remain shouldered with the bulk of public spending. The economic outlook for local government finances has weakened and their buffers for dealing with problems have shrunk. Deficiencies in statistical reporting, heavy-handed political guidance and censorship of economic discussions further complicate efforts to form an accurate picture of current economic situation or produce reliable economic projections. This problem also complicates domestic policymaking and increases the risk of policy errors.

Financial market risks have increased. Banking sector profitability continues to decline, particularly among smaller banks, which are obliged to provide financing to priority sectors and local governments. The banking sector has accumulated a large body of low-quality loans resulting, among others, pandemic era payment deferral policies and ongoing construction developer difficulties, even if such loans are not formally recorded as non-performing. In any case, it is difficult to estimate the true extent of risks due to the Chinese financial sector’s lack of transparency and baroque financing and ownership structures.

The return of consumer confidence through e.g. improved labour conditions or a recovery in the housing market could increase domestic consumption to levels above our baseline forecast (especially in light of the substantial savings accumulated by households). Continued investments in technological development in such fields as artificial intelligence and robotics could also boost productivity growth more rapidly than expected.

Trade and geopolitical risks, along with their related uncertainty, are expected to remain high during the forecast period. In addition to the capriciousness of US trade policy, China's own measures such as export restrictions, as well as countermeasures by other countries, aggravate uncertainty. A prolonged crisis in international energy markets and declining global demand would also restrain Chinese growth. Unilateral actions by China in the South China Sea or towards Taiwan carry the risk of confrontational escalation. An intensified conflict in the region would have serious international implications and detrimental economic impacts for China and the world.