BOFIT Weekly Review 26/2025

Government-funded consumer rebates drove China’s retail sales growth in May, but housing sales continued to stumble

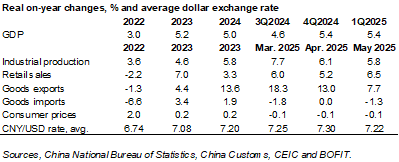

Nominal retail sales grew by 6.4 % y-o-y in May. Real growth in retail sales likely also accelerated as consumer price inflation remained close to zero (-0.1 % in May). The revival in sales is not necessarily long-lasting or evidence of increased consumer confidence, however. Fuelled by government support, consumer interest was particularly strong in upgrading home appliances (sales value up by 53 % y-o-y in May) and communications devices (up 33 %).

The trade-in rebate programme to stimulate purchases of durable goods, which was launched last year, has been expanded this year. Officials say that sales driven by the programme have already surpassed last year’s total this year. The government earmarked 300 billion yuan this year to support sales of durable consumer goods. Of that, 162 billion yuan had already been allocated to regional governments by the end of April. Regions themselves have also committed to providing smaller amounts of support. In any case, some regions have already exhausted the funds available for consumption subsidies, forcing them to either suspend or limit the disbursal of subsidy payments. Home appliances and communications devices worth a total of 850 billion yuan were sold in the first five months of this year. Low-emission cars are included among the goods eligible for subsidies, but car sales (representing about a tenth of total retail sales) were only up by 1 % y-o-y in May. Subsidies outside the consumer trade-in programme have been available for the purchase of low-emission vehicles also in previous years.

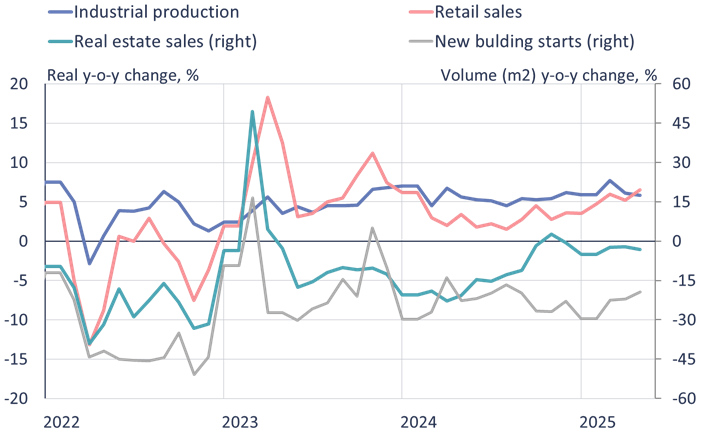

In May, 12-month growth in industrial output slowed slightly to 5.8 %. Growth has been brisk this year in the manufacturing sector, particularly in production of cars and other vehicles, as well as production of electronics. Export demand remained relatively strong in May, with export volumes growing by 8% year-on-year, despite a sharp decline in exports to the United States. The volume of imports declined by 1 % y-o-y. China’s exports have been supported in part by yuan depreciation against the currencies of most major trading partners. With the US dollar continuing its downward slide this year, the People’s Bank of China has allowed the yuan to appreciate only modestly against the dollar. Since the start of this year, the yuan’s nominal effective (trade-weighted) exchange rate (NEER) has fallen by 5 %. In the same period, the yuan has lost about 10 % of its value against the euro and gained about 2 % against the dollar.

Fixed investment growth slowed in May, and the value of real estate investment fell by 12 % y-o-y. The volume of real estate construction measured in terms of floorspace declined by 19 % y-o-y. Property sales also continued their on-year decline. At the on-month level, the downturn in property sales seems to have plateaued since late last year. China’s official statistics show that also apartment prices continued to slide in May. Compared to the 2021 price peak, prices for existing housing are reported to be down by nearly 20 %. Price declines on average have been larger in smaller cities and towns. Regional variations in apartment prices are considerable, however. In some regions, price declines have been considerably larger than the reported national average.

Retail sales growth accelerated in May, but property construction and sales continued to decline

Sources: China National Bureau of Statistics, CEIC and BOFIT. Real retail sales growth calculation uses consumer price inflation.

Lending growth, partly a reflection in the decline in demand for housing loans, has been slowing for several years. The stock of bank lending grew 6.7 % y-o-y in May. While the stock of other household loans continues to grow, the stock of housing loans has been shrinking over the past two years. The stock of loans granted to households grew by 2 % y-o-y in May. Households have found loan repayment more challenging in an environment of falling housing prices and weaker labour market conditions. The share of nonperforming household loans (NPLs) in large bank portfolios has exceeded the overall NPL ratio since 2022. The NPL ratios reported by Chinese banks are still modest, however, and by most estimates do not give a realistic picture of bank lending risks.