BOFIT Weekly Review 23/2025

Russian growth overall slows, in some branches and regions output has declined

Preliminary Rosstat estimates show Russian GDP grew by 1.4 % y-o-y in the first quarter. The Ministry of Economy evaluates that January-April growth was 1.5 %. The slowdown in growth from last year’s 4 % pace was expected, however. Russian output has long relied on ever-increasing government spending to prop up branches critical to the war effort that has resulted in worsening economic imbalances, like severe labour shortages and high inflation. In April, consumer prices were up 10 % y/y and the Central Bank of Russia has kept the key rate at record high level of 21 % for months.

Production capacity is already stretched to the limit, so it is increasingly difficult to maintain output growth with further increases in government spending. Most institutional forecasters expect Russian GDP to grow by 1.5–2 % this year. The aggregate growth is, however, unevenly distributed across branches, regions and social groups.

Sanctions have depressed production in many industrial branches

Manufacturing branches connected to the war effort have posted particularly high growth. The production volumes for certain metal products, computers and electronics, as well as volumes of certain transport vehicle production have soared in recent years. Construction has also seen robust growth.

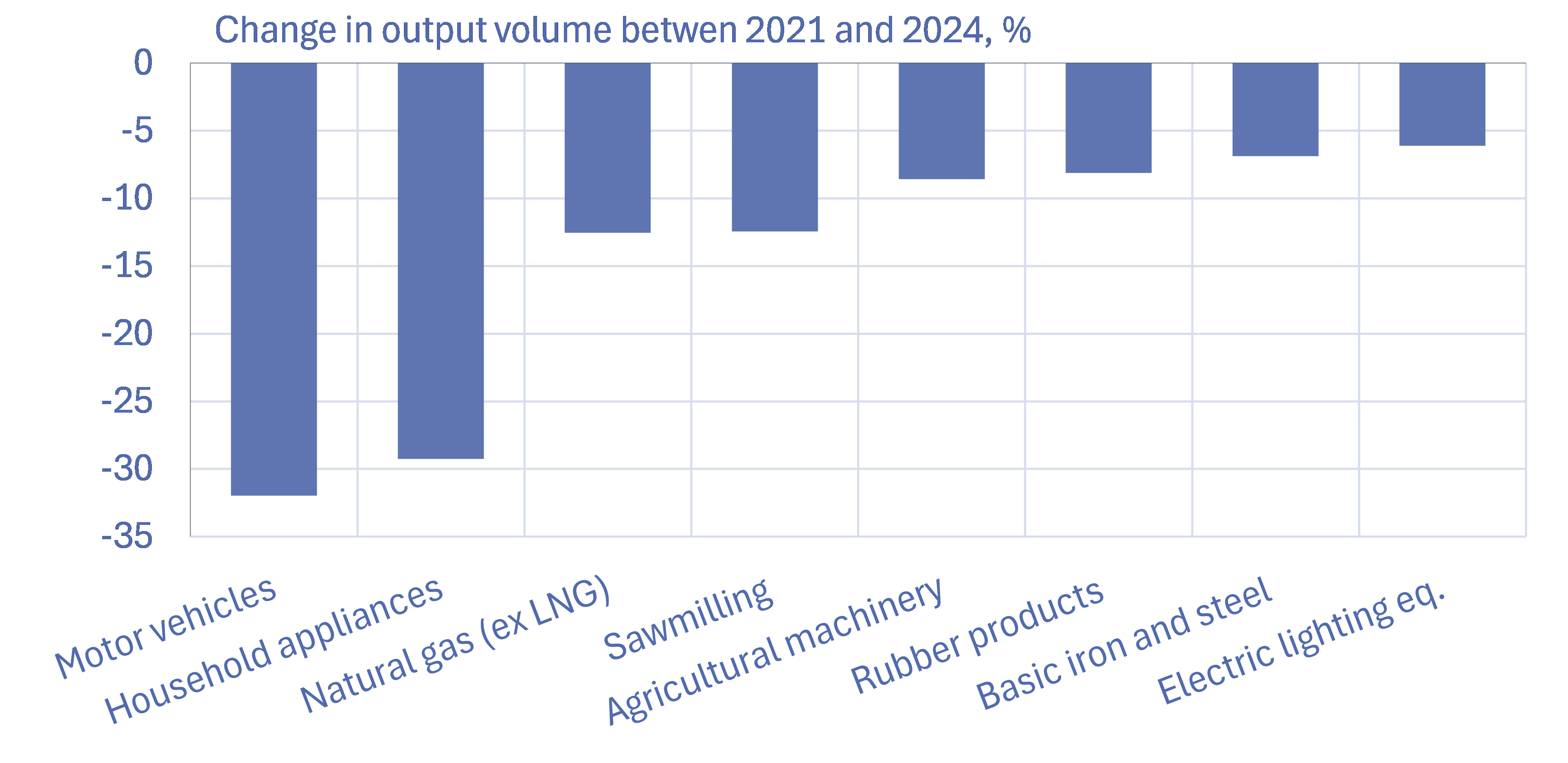

Production has declined in many industrial branches in recent years due to sanctions on Russia and the deterioration of Russia’s economic relations with the EU and many other countries. The car industry has been battered by the departure of foreign carmakers from the Russian market, with 32 % fewer motor vehicles produced last year than in 2021. Restrictions on Russian imports and giving top priority to the needs of defence industries has interfered with domestic manufacturing of machinery & equipment. For example, production of household appliances was last year down 30 % from 2021. Production of general purpose machinery and farming equipment also declined sharply between 2021 and 2024.

The cessation of exports to the EU has particularly affected the timber, coal, natural gas and automobile tire industries. Saw milling, production of base metals, iron ore and rubber products have contracted by about 10 % from pre-war 2021. Coal production has also declined, and especially in recent months coal producers have struggled with the lack of profitable export options. With export prices falling and transportation costs rising, the government has recently compiled a special support package for the coal industry.

Russian Industrial output declined in many branches between 2021 and 2024

Sources: CEIC, Rosstat, BOFIT.

Regions in Northwestern Russia hit hard by declining exports

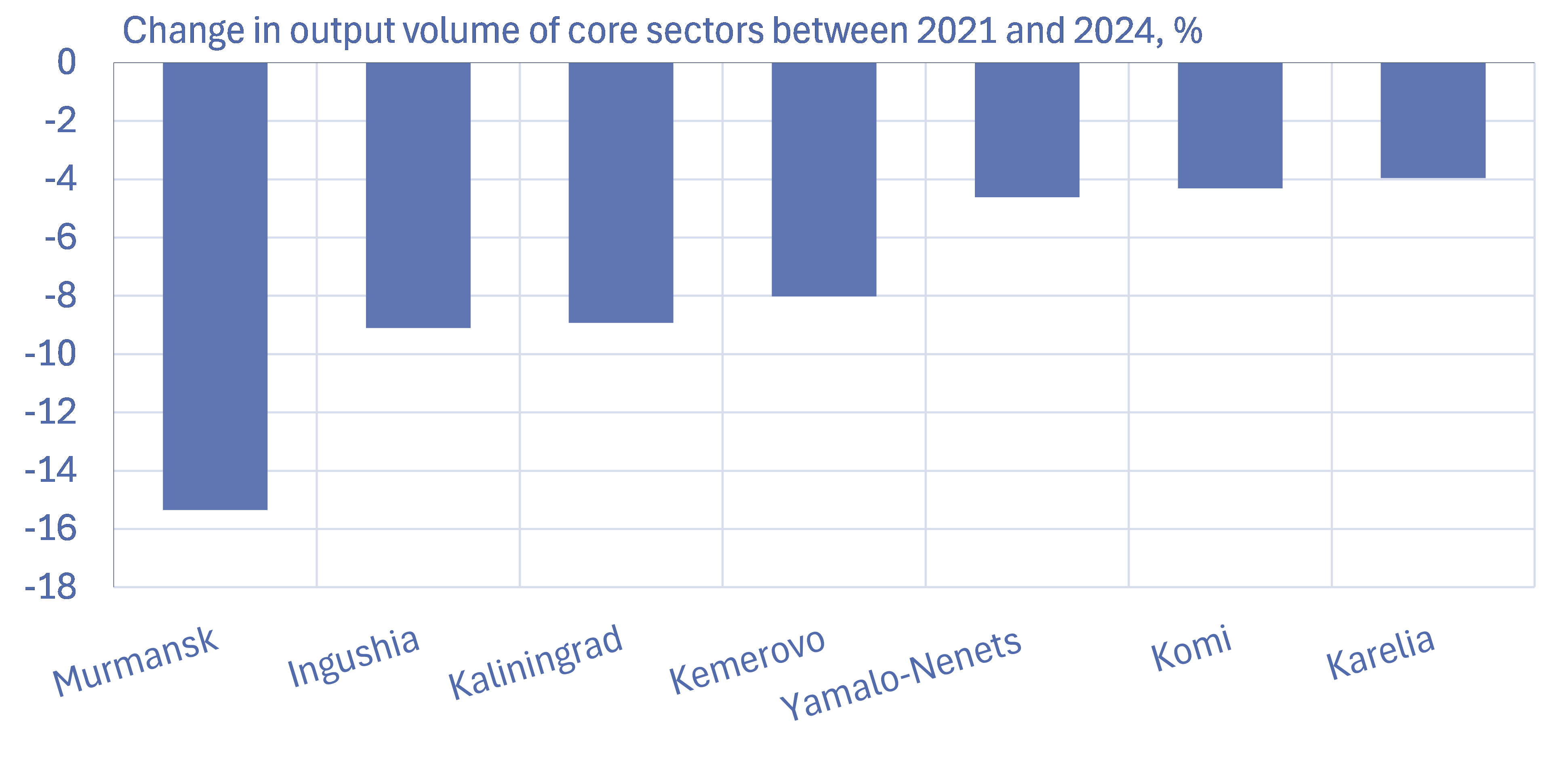

Varying industrial trends are reflected in regional economic growth rates. Rosstat’s most recent figures for regional GDP growth are from 2023, but more recent GDP growth trends can be inferred from 2024 readings of the “five core sectors” index covering industry, agriculture, construction, transportation and retail trade.

Production growth appears to have been highest in regions located near Russia’s southern border, including regions in western Russia and southern Siberia. Many of these regions (e.g. Kurgan) are home to major defence industries. Growth driven by large military-industrial presences is also evident e.g. in the regions of Tula and Tatarstan.

Rapid production growth figures have also been posted by some regions in the Far East Federal District, most notably the Sakha Republic, which produces a wide range of commodities from gold and diamonds to timber and natural gas. Growth overall in the Far East Federal District has been slightly lower than the national average, however. Although the focus of Russian economic relations has shifted sharply to China in recent years (see BOFIT Policy Brief 10/2025), no substantial effects at the wider regional level are so far detectable.

The reading for the five core production sectors has seen particularly large contractions in regions of the Northwestern Russia Federal District (e.g. Murmansk, Kaliningrad, Komi and Karelia), as well as the Kemerovo region (Siberia Federal District), the Kaluga region (Central Federal District), and the Yamalo-Nenets peninsula (Urals Federal District). Sanctions and withering of economic relations with EU partners have hit these regions particularly hard. Northwestern Russia has a large forest industry, while Kemerovo is a major coal-producing region. The Yamalo-Nenets autonomous region accounts for the lion’s share of Russian natural gas production. The Kaluga region is a major production hub for Russia’s car industry.

Production has declined in several regions of Northwestern Russia in recent years

Note. Core production sectors comprise industry, agriculture, construction, transportation and retail trade.

Sources: Rosstat, BOFIT.

Despite higher GDP, economic conditions for many Russians have worsened

Income trends from impacts of the war vary across demographic groups. While the strong growth in the military-industrial sector and acute labour shortages have driven up wages in many branches, not all Russians have benefited from this development.

A survey conducted in February within the framework of the Chronicles project by Russian independent researchers to gauge Russian attitudes to the Ukraine war found that half of respondents experienced the impacts of the war negatively with respect to their everyday lives. Some 36 % of respondents said that their economic situation had deteriorated over the past 12 months. A recent consumer survey conducted by the Central Bank of Russia also found the share of respondents claiming to be worse off economically has been in the range of 25–30 % this year. The CBR survey noted that 25–30 % of respondents also claimed they had sufficient funds to purchase food, but not enough left over to purchase clothing or other goods.

Rising food prices, in particular, have made life harder for Russia’s poorest households. Nearly half of the spending of households in the poorest decile (bottom 10 %) goes to food, while for households in the top decile food only accounts for about a fifth of spending. Prices for many staple foods have risen rapidly in recent years. For example, Rosstat reports that average kilo prices this year for butter, potatoes and cabbage are double those of spring 2021.

The relative status of the poorest households has also deteriorated in recent years. At the beginning of 2022, the average monthly income of the wealthiest decile (top 10 %) was 15 times greater than that of the poorest decile. By the end of 2024, the wealth gap had widened to nearly 17 times greater for the richest decile.

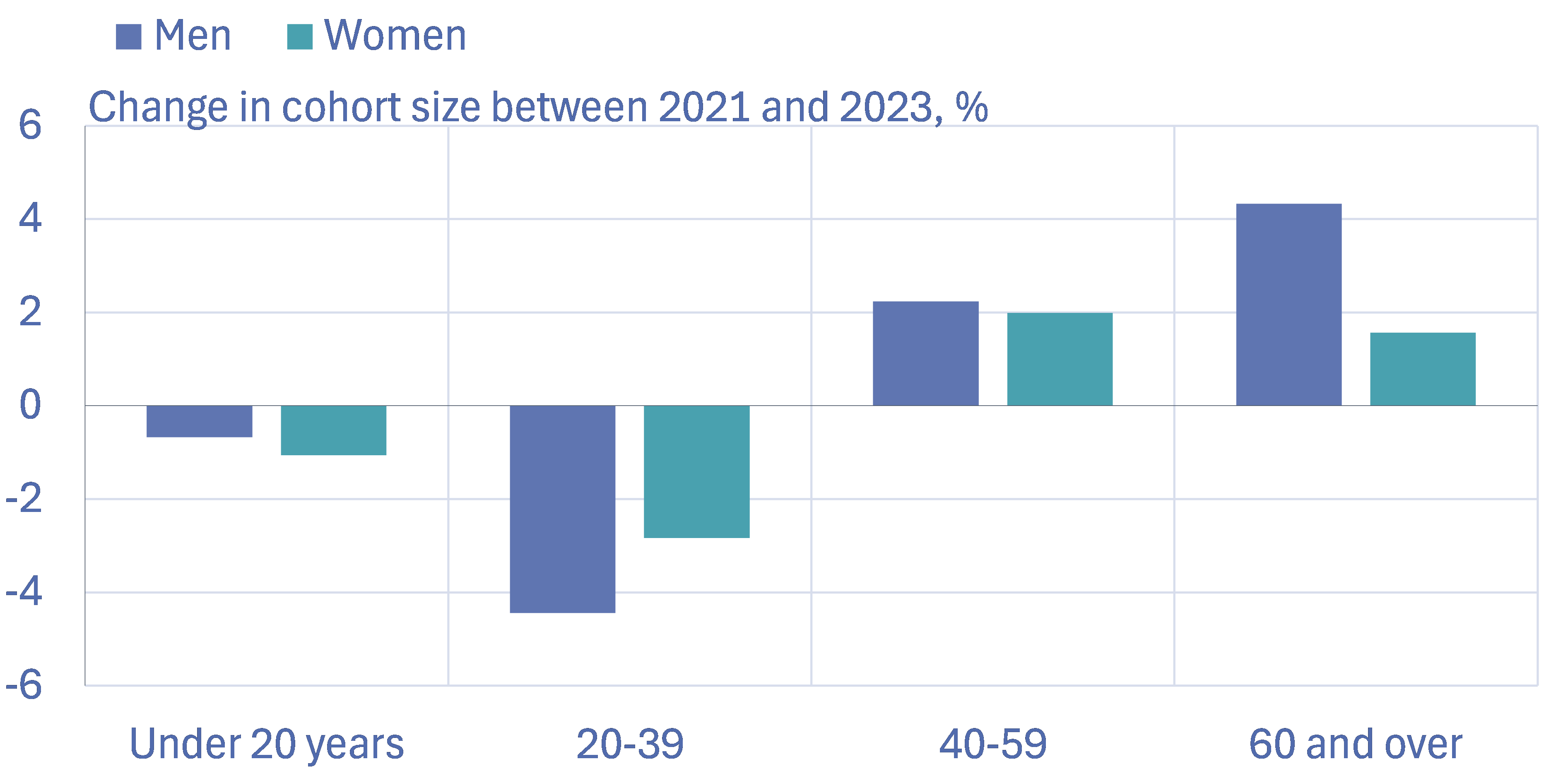

Unsurprisingly, the war appears to have affected also Russia’s demographic trends. While a shrinking trend for younger cohorts has long been established, the decline has become steeper in recent years and the number of young men has declined more than young women. Most estimates of Russian soldiers killed in the war range between 150,000 and 200,000. In addition, hundreds of thousands of Russians have moved abroad to avoid the war. Russia’s birth rate has also fallen to an all-time low this year. Russian government has been particularly worried about the birth rate and tried to come up with measures to push for higher birth rate. It has become increasingly difficult to get information on population trends in Russia as Rosstat has ceased to publish many of the data series related to demographic topics.

The cohort of men under 40 in Russia has shrunk the most in recent years

Sources: CEIC, Rosstat, BOFIT.