BOFIT Weekly Review 19/2025

Russian economic growth continued much slower in March

Russia’s economic development ministry estimates that the country’s GDP growth fell in March to just 1.4 % y-o-y, and that first-quarter GDP growth was 1.7 %. Growth has slowed significantly from last year’s brisk 4 % pace. Rosstat’s indicator of five core sectors of the economy that typically tracks GDP trends, showed a slight decline in March compared to previous months in seasonally adjusted terms.

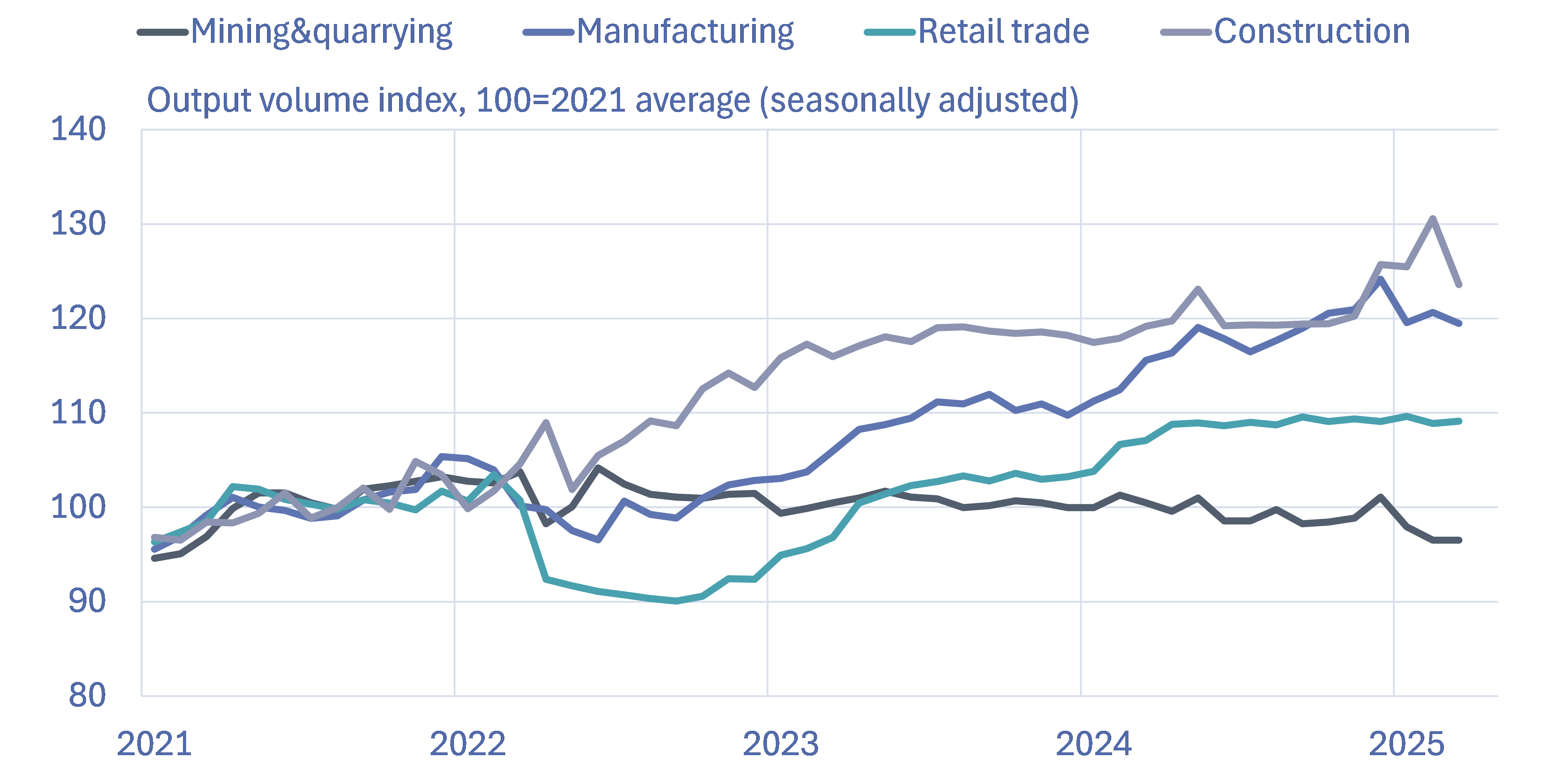

Industrial output and construction turn to a downward trend

Industrial output declined throughout the first quarter, with the situation showing no improvement in March. Mining & quarrying (includes oil & gas production) contracted by 4 % y-o-y in both March and the first quarter overall. Manufacturing has also declined from its peak at end-2024. Manufacturing output, however, was still up by 4 % y-o-y in March.

Construction activity also began to decline in March following a burst of growth in previous months. In annual terms, construction output was still up by 3 %, however. As housing construction growth remained robust, it appears that growth in other construction categories was distinctly weaker.

The volume of retail sales, which has remained unchanged for several months, showed little change in March as well compared to previous months. In annual terms, retail sales were, however, still up by 2 % y-o-y. The average real wage continued to rise in the first months of the year, but at a much slower pace than before. High inflation has eroded the purchasing power of consumers. Consumer prices were up by 10 % y-o-y in March.

The Central Bank of Russia noted that slowing economic growth has apparently reduced inflationary pressures a bit. Inflation has been fuelled mainly by rising prices for food and services. High interest rates have reduced demand for consumer credit, however, and this has dampened increases in prices for non-food goods. Inflation expectations remain in general elevated. Taking these various trends into account, the CBR board decided at its April meeting to keep the key rate unchanged at 21 %.

Many sectors in Russia saw weaker development in March

Note: Figures for the core sectors of “Mining & quarrying” and “Manufacturing” are also workday adjusted.

Sources: Rosstat, CEIC, BOFIT.

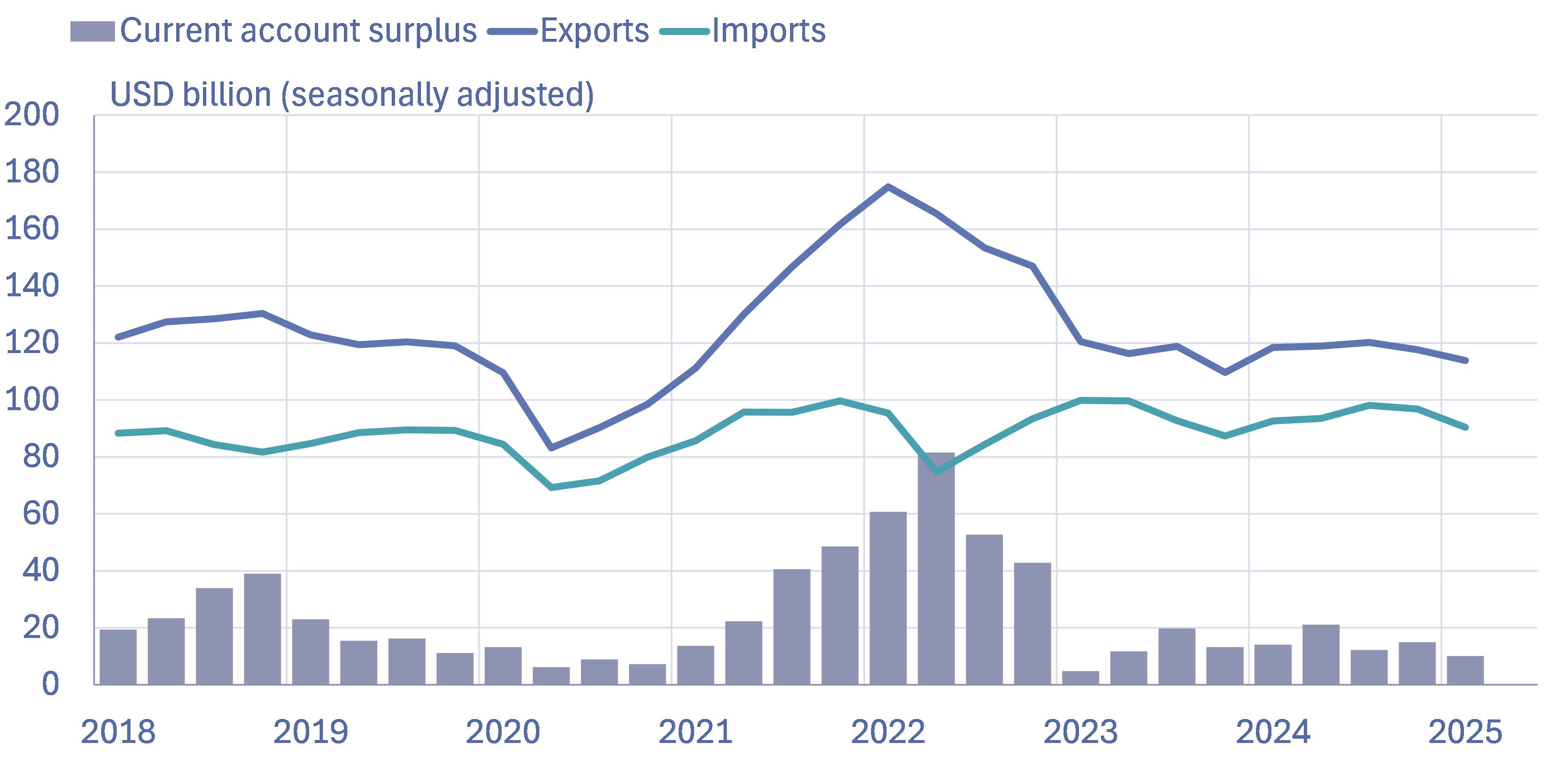

Foreign trade contracted in the first quarter; current account surplus down slightly

The value of Russian exports of goods and services contracted by 4 % y-o-y in January-March. The main cause of the decline was the poor performance of Russia’s oil exports. The International Energy Agency (IEA) estimates that Russian oil export earnings fell by 14 % y-o-y in 1Q2025, due both to reduced export prices and lower export volumes. The discount on Russian oil compared to similar blends increased in the first quarter to an average of $12 a barrel. The US and EU both tightened their sanctions on tankers transporting Russian crude. The CBR estimates that the change has further raised shipping costs for Russia and encouraged buyers to demand larger discounts.

Export of natural gas to EU countries declined further due to the cessation of gas pipeline transmission via Ukraine. In contrast, higher prices have raised the value of exports of chemical products and metals. According to the CBR, export volumes have been limited by the latest sanctions imposed by the US and EU on sea shipments and payments traffic.

The value of Russian goods and services imports declined by 3 % y-o-y in January-March. The main reason was a contraction in imports of machinery, equipment and transport vehicles. Automobile imports fell due to another sizeable hike in the vehicle recycling fee for imported cars at the start of this year. Growth was registered in imports of foodstuffs and tourism services.

Russia’s 1Q25 current account surplus amounted to $20 billion, a slight decrease from 1Q24. The cumulative current account surplus of last four quarters was about $60 billion, just under 3 % of GDP.

Russian foreign trade has declined this year

Sources: CEIC, Central Bank of Russia, BOFIT.

This year’s budget plan revised to account for lower oil prices

Russia’s economic outlook has been clouded by the recent sharp decline in crude oil prices. In response, Russia’s finance ministry last week announced changes to this year’s budget framework. The latest revenue projection assumes an average oil price this year of $56 a barrel (down from $70 earlier). The RUB-USD exchange rate has been raised from 96.5 to a slightly stronger rate of 94.3. The revised assumptions significantly reduce estimated federal budget revenues.

Although oil revenues are expected to contract compared to earlier expectations, the finance ministry slightly boosted its forecast for tax revenue streams other than oil & gas earnings. Spending will also increase slightly. The predicted federal budget deficit under the new budget framework is significantly larger than earlier. The federal budget deficit in this year’s approved budget framework was only 1.2 trillion rubles, but under current projections now rises to 3.8 trillion rubles (1.7 % of GDP).

The impacts of declining oil prices of Russia’s government finances are discussed in this recent BOFIT blog post.

Russia’s growth expected to slow further this year even as inflation remains high

Despite falling oil prices, Russia’s economic development ministry has retained its previous forecast, which was already considered quite optimistic at the time it was released. The economic development ministry expects GDP to grow by 2.5 % this year and 2.4 % next year. The CBR forecast released at the end of April also remains largely unchanged from the central bank’s previous forecast, and still anticipates GDP growth of 1–2 % this year and 0.5–1.5 % next year. The CBR estimates that the rise in consumer prices this year will average 9–10 %, and then decline to the central bank’s inflation 4 % target in late 2026. This scenario, however, requires maintaining the key rate at high levels. The CBR currently expects the key rate to average 19.5–21.5 % this year and 13–14 % next year.

The outlooks of most international forecasting institutions largely align with the CBR’s forecast. The IMF’s latest World Economic Outlook (WEO), published in April, sees Russian GDP growing by 1.5 % this year and 0.9 % next year. The IMF anticipates inflation running at 9 % this year and slowing to close to the CBR’s 4 % target at the end of next year. The average of key international forecasts compiled in April by Consensus Economics predicts that Russian GDP will grow by 1.7 % this year and 1.2 % next year. Inflation was expected to average 7 % this year and 5 % next year.

The impacts of war and sanctions on Russia’s long-term economic growth potential and business environment are discussed in this recent BOFIT blog post.