BOFIT Weekly Review 14/2026

Profitability down for China’s banking sector

China’s National Financial Regulatory Administration (NFRA) reports the aggregate total assets of China’s banking sector rose last year to around 480 trillion yuan (342 % of GDP), an increase of 8 % y-o-y. The total assets of the largest banks grew faster than other banks, collectively accounting for about 44 % of the banking sector’s total assets. The value of the loan stock climbed to 276 trillion yuan (197 % of GDP), an increase of over 6 % y-o-y. The combined profits of Chinese banks last year amounted to 2.4 trillion yuan, an increase of about 2 % from 2024 and approximately the same amount as in 2023. Profitability and earnings have stumbled on weakness in the domestic economy, the real estate sector’s woes, increased competition from non-bank actors operating in the sector, as well as falling interest rates. At the same time, the government has mandated that banks support the economy with inexpensive loans and flexible lending terms.

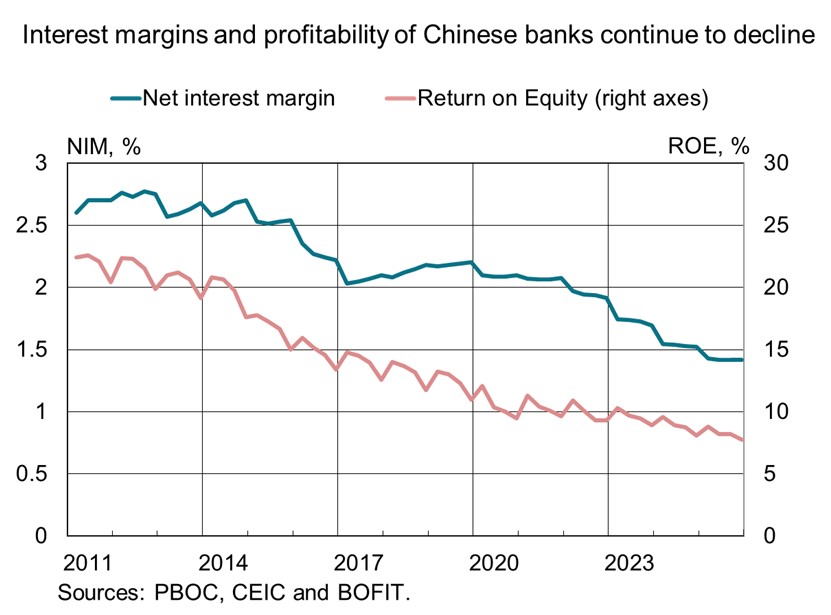

The average lending rate on bank loans fell to around 3 %, causing banks’ main source of income, the net interest margin (difference between lending and deposit rates), to decline to a historically low level of 1.4 %. The structure of the Chinese economy also affects the banking sector’s growth potential, as growth relies heavily on export industries generously funded with cheap loans from state banks. Overcapacity and fierce competition have depressed prices and eroded firm competitiveness. Official figures suggest non-performing loans (NPLs) accounted for an exceptionally low 1.5 % of the loan stock. The composition of these problem loans, however, has deteriorated. Already last year, 44 % of problem loan were classed as loan losses, up from below 25 % just two years earlier. Loan-loss reserves set aside to buffer credit losses grew by nearly 4 % y-o-y, and were equivalent to 2.6 % of the total loan stock at the end of 2025.

Bank profitability continued to decline. Return on equity (ROE), which was still around 10 % a few years ago, fell to 7.8 % last year. Capital adequacy ratios, however, remained stable, with Common Equity Tier 1 (CET1) ratios averaging 11 %, essentially the same level as over the past ten years. Central government officials have long encouraged small and medium-sized banks to merge with larger banks to improve efficiency. Last year saw a record number of bank mergers, even if NFRA figures only cover part of the year. As of end-June last year, 4,070 banks operated in China, 225 fewer banks than at the end of 2024. Almost all institutions that disappeared from statistical monitoring were rural banks or rural financial institutions.

Pressure to strengthen the sustainability of the financial system has been heightened by slowing economic growth and the prolonged struggles of the real estate sector. Earlier in March, officials announced plans to recapitalise large state-owned banks this year through the issue of 300 billion yuan in special sovereign bonds. A similar recapitalisation operation last year issued 500 billion yuan in special sovereign bonds. Tighter ownership rules and limited access to private capital have also increased the reliance of small regional banks on government recapitalisations. Local government special bonds have been used to inject capital into these banks, amounting to more than 500 billion yuan in total over the period 2020–2025.

Chinese officials are currently considering relaxation of ownership restrictions as a way to increase the ability of commercial banks to raise capital. According to the rules adopted in 2018, an investor with holdings of at least 5 % in a bank is considered a “significant shareholder.” Such investors can have significant positions in no more than two commercial banks and can control only a single bank. The possibility that some investors may be allowed to act as significant shareholders in one or two additional banks is now under consideration. The government is also considering easing restrictions on bank investments by large state-owned insurance companies in order to direct capital to smaller urban banks. The influence of large shareholders in financial institutions was tightened in the past after several institutions ran into problems due to shareholder misconduct.