BOFIT Weekly Review 10/2026

IMF urges China to make more forceful efforts to boost domestic demand

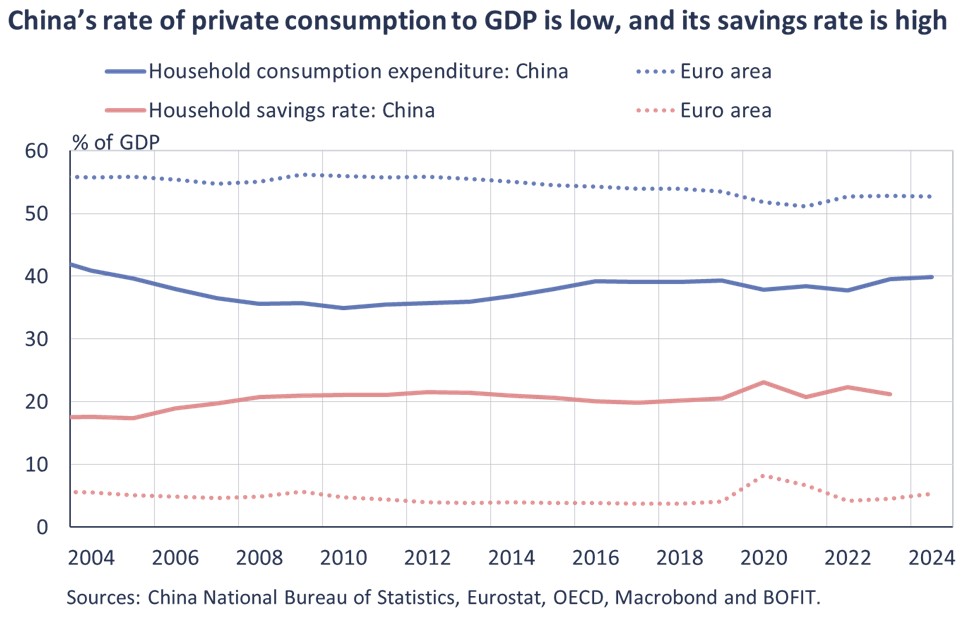

In its latest Article IV consultation for China, the International Monetary Fund (IMF) sees strengthening of domestic consumption demand as the most important and urgent means for reducing the structural imbalances within the Chinese economy. Without more robust measures, China faces the risk of an extended deflation that could lead to a vicious spiral of slowing growth and aggravated debt problems. Stronger domestic demand would also reduce external imbalances and strengthen the yuan’s exchange rate.

The IMF expects the Chinese economy to grow by 4.5 % this year, but notes that the risks are tilted to the downside. Economic slack sustains downward pressure of prices. More-than-expected erosion of domestic demand due to the prolonging crisis in the real estate sector and rising indebtedness could lead to a situation where economic growth remains heavily reliant on exports. Rising trade tensions and the size of the Chinese economy, however, limit the sustainability of export-led growth.

The IMF called for the continuation of expansionary economic policies over the short term to boost consumption and support higher prices. Stimulus measures should focus on consumption and supporting the real estate market, as well as improving the social safety net and it should be reduced in the areas of unprofitable investments and industrial subsidies. The IMF also sees room for more accommodative monetary policies as long as they do not result in further exchange-rate depreciation. The setting of a medium-term inflation target would help China better focus and communicate monetary policy actions. The IMF also called for more flexible exchange-rate-setting and more transparent exchange-rate regime to improve the transmission of monetary policy. The IMF calculates that China’s real effective (trade-weighted) exchange rate, or REER, was undervalued by 12–21 % at the time of its analysis.

The IMF estimates that China's industrial policy support measures amount to 4 % of GDP, significantly higher than the EU average (about 1.5 % of GDP). Industrial policy support has generated oversupply in many sectors, depressed prices and caused China’s current account surplus to balloon. They have also led to investment misallocation, which, according to IMF estimates, has reduced the level of GDP by 2 %. The IMF recommends reducing unwarranted industrial policy measures (such as subsidies and tax benefits) by half and making it easier for unprofitable firms to declare bankruptcy. These changes would enhance productivity, as well as reduce spending pressure and financial risks, especially for regional governments.

China’s financial risks remain elevated. The IMF recommends timely recognition of losses as well as clean-up of corporate balance sheets and improving their transparency. The profitability of the banking sector continues to decline with the ongoing real estate sector crisis and the degraded ability of firms to service their debts, especially in the case of smaller regional banks. Prolonged deflation may also lead to higher real debt burdens and debt‑servicing costs.

The IMF sees Chinese economic growth gradually slowing to around 3½ percent in 2029–2030. Growth over the medium term could be accelerated with market-based reforms, along with improvements in the social safety net and easing movement of individuals within the country. The IMF estimates that increasing social spending especially in rural areas by 1 % of GDP and granting urban residency rights (hukou) to 100 million migrant workers (half of the migrant population) could increase the consumption-to-GDP ratio by three percentage points. Over the longer term, rising public indebtedness must be reined in by cutting back on industrial subsidies and reducing off-budget investments by local governments, as well as broad-based tax reforms. The IMF also reminded that the deficiencies in Chinese statistical data, particularly with respect to GDP and the fiscal data, complicate monitoring of the Chinese economy.