BOFIT Weekly Review 4/2026

Growth of China’s credit stock slowed last year; PBoC moves ahead with targeted monetary easing

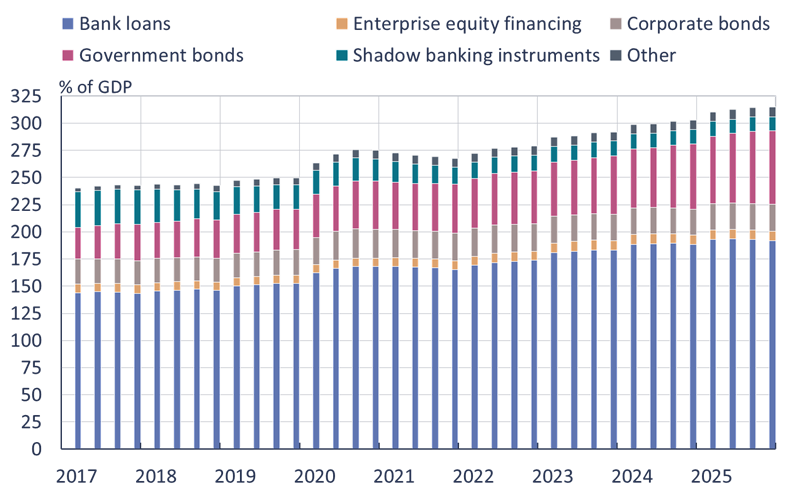

The stock of bank loans grew by 6.2 % last year. While this rate was lower than in previous years, it still outpaced nominal GDP growth (4 %). The stock of household loans shrank by 1 % last year. Despite interest subsidies for consumer loans, the stock of short-term loans to households shrank by 7 % in 2025. Demand for housing loans has also been low as the real estate market crisis drags on.

The central bank’s broad domestic financing measure (aggregate financing to the real economy) rose by 8.3 % last year, reaching the equivalent of 315 % of GDP. Growth in debt issues was led by central and regional government borrowing, which collectively saw their debt stocks increase by 17 %. The central government’s debt stock increased last year by 16 trillion yuan to just over 40 trillion yuan. Correspondingly, local debt issues rose by more than 7 trillion yuan to just under 55 trillion yuan. Local governments, in particular, were active in issuing special purpose bonds, which have been used, for example, to pay off existing high-interest loans incurred by off-budget local government financial vehicles.

Despite slowing growth in the credit stock, the PBoC only moved to a slightly more accommodative monetary stance last year. Policy rates and bank reserve requirements were lowered just once in the spring (BOFIT Weekly 20/2025). Indeed, China’s low inflation rate would have allowed additional easing as consumer prices remained at the 2024 level. Towards the end of the year, inflation accelerated slightly, standing at 0.8 % y-o-y in December.

Despite the PBoC’s announcement this month of easing of the monetary stance in a targeted manner, no significant effect on the real economy is yet expected. The PBoC lowered the interest rate for its targeted structural financing programmes by 25 basis points on January 19. The one-year interest rate, for example, in the programme for rural development and small businesses as well as in relending facility has been reduced to 1.25 %. At the same time, the size of some targeted lending programmes was increased. The combined quota for all programmes can be estimated to correspond to roughly 15 % of the PBoC’s total assets. At the end of last year, the central bank also continued to buy government bonds on secondary markets. Purchases, which began in the summer of 2024, were suspended at the beginning of last year when market interest rates declined. In the final three months of 2025, the PBoC kept its bond-purchasing modest, acquiring just 120 billion yuan ($17 billion) in net terms, well off the pace of the net 1 trillion yuan in bond purchases in 2024.

The finance ministry also began in January to offer interest subsidies on loans to private small firms. The interest subsidy, now raised to 1.5 percentage point for up to two years, is hoped to increase the investment activity of small firms. Interest subsidies for household consumer loans as well as interest support for service-sector firms will continue to the end of this year.

China’s domestic-debt-to-GDP ratio increased slightly last year

Sources: People’s Bank of China, CEIC and BOFIT.