BOFIT Weekly Review 4/2026

In China, official 2025 GDP figure aligns with target; alternative estimate suggests lower growth

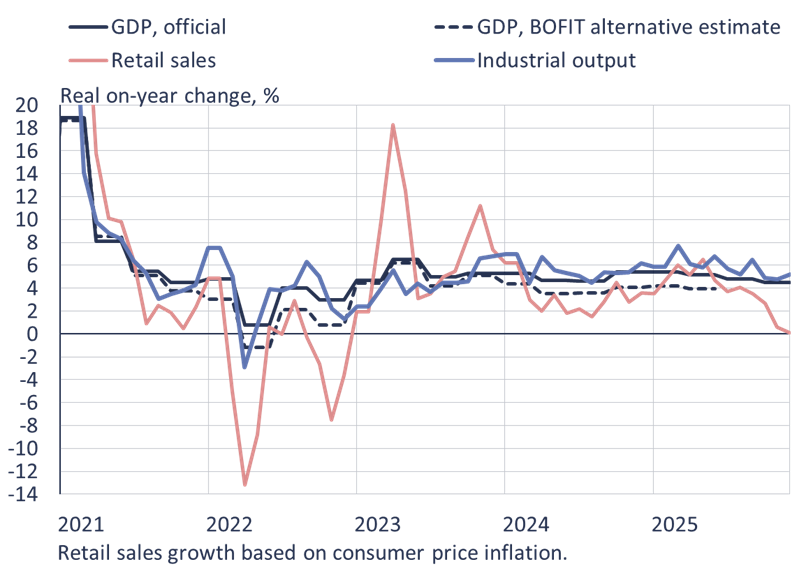

China’s National Bureau of Statistics (NBS) reports fourth-quarter growth of the Chinese economy slowed to 4.5 % y-o-y. Third-quarter GDP growth last year was still 4.8 % and first-half growth exceeded 5 %. The NBS data also indicate that consumption demand accounted for 2.4 percentage points of 4Q GDP growth, while net exports contributed 1.4 percentage points and investment demand 0.7 percentage point. GDP growth for all of 2025 (5.0 %) unremarkably matched the official “about 5 %” target announced at the National People’s Congress last spring.

BOFIT's alternative GDP calculation suggests that economic growth for all of 2025 was roughly 1 percentage point below the official figure. The alternative GDP growth estimate for the fourth quarter was 3.3 %. Industrial output growth accelerated slightly in December from previous months to over 5 % y-o-y. For all of 2025, industrial output rose by roughly 6 % y-o-y. Foreign trade, which is closely linked to industrial output, remained strong throughout the year. Net exports clearly supported economic growth for the entire year.

Domestic demand, on the other hand, remained quite subdued. Real growth in retail sales slowed throughout the year, falling to near zero by December. For all of 2025, retail sales are estimated to have grown in real terms by less than 4 % y-o-y. The finance ministry plans to increase funding this year to support consumption of services in particular. Interest subsidies for households and service-providing firms will be extended, and tax breaks for elderly care, child care and home care services will be prolonged until the end of 2027.

The decline in fixed investment continued to deepen further. Fixed investment declined in yuan terms by about 15 % y-o-y in the fourth quarter, and was down by 3.8 % in nominal terms for the year as a whole. When real estate investment is excluded, however, fixed investment fell last year by just 0.5 % in nominal terms, highlighting the magnitude of real estate’s impact in the overall development. Real estate investment fell last year by 17 % y-o-y, volume of building starts declined by 20 %, and apartment sales dropped by 10 %.

Even if the rise in prices in China has been quite modest, it does not alter the overall picture that real investment growth was tepid at best. Official figures show that investment demand still accounted for about 17 % of total economic growth last year. This is partly explained by the fact that the investment term includes changes in inventories. Firms often increase their inventories when demand is weak, so some of the contribution to growth from investment likely reflects a build-up of inventories rather than productive investments.

While no official growth target for 2026 has yet been released, China Daily, the national English-language newspaper of the Communist Party of China, sees this year’s target settling in the range of 4.5–5 %. The final growth target will be approved at the plenary session of the National People's Congress in March.

Retail sales growth slowed sharply late last year

Sources: NBS, Macrobond and BOFIT.