BOFIT Weekly Review 2/2026

Brisk trading activity on Chinese stock exchanges last year

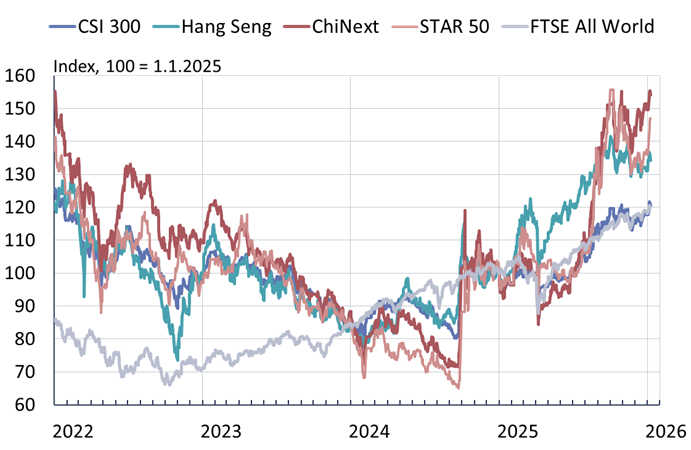

Trading on mainland China stock exchanges grew significantly last year, with share prices rising after a spring downturn. The gains were largely driven by the allure of tech stocks. The Shanghai bourse’s index of top 50 companies in its Science and Technology Innovation Board (STAR 50) rose 36 % in 2025, while the Shenzhen exchange’s ChiNext index of tech and high-growth companies climbed 50 %. The rise continued in the early days of this year. The CSI 300 index that includes Shanghai’s and Shenzhen’s largest companies rose 18 % last year, keeping pace with the FTSE All World index of global stocks.

Trading on the Hong Kong Stock Exchange also picked up significantly, with tech firms leading the rise in share prices. The Hong Kong exchange’s main Hang Seng index rose by 22 % last year, while its index of IT firms gained 39 %. The volume of IPOs rose significantly with 119 new firms listed on the Hong Kong exchange. The value of Hong Kong initial public offerings was the highest in the world (HKD 286 billion; USD 37 billion). The largest listing on the Hong Kong bourse was CATL, the Chinese producer of electrical vehicle (EV) batteries and energy storage systems.

Of the 130 new listings on mainland China exchanges, 24 were listed on the Beijing stock exchange, which is far smaller than the Shanghai and Shenzhen exchanges. There was an effort to accelerate listings of firms involved with artificial intelligence and microchips to increase their funding possibilities. According to the KPMG consultancy group, mainland China exchanges last year accounted for 15 % of the value of the world’s IPOs, behind the US bourses with 25 % and the Hong Kong exchange with 20 %.

The trading volumes on mainland China stock markets hit a record high last year of 421 trillion yuan ($59 trillion). Institutional investors accounted for some of the increase in trading activity. Since 2023, officials have urged state insurance and pension funds to invest more of their assets in domestic stock markets. Low interest rates have also driven some households to put some of their savings in stock markets in pursuit of higher yields. While margin trading on borrowed money has increased, its share of share trading has not risen significantly. Margin trading account for over 10 % of the stock exchanges’ trading volume and less than 3 % of the total value of shareholdings.

Trading activity of foreign investors on mainland China exchanges has also increased. The daily trading volume in mainland exchanges via the Stock Connect programme increased significantly from 2024 to 2025. As data on the value of purchases and sales of shares under the Stock Connect programme are no longer published, the net flow of funds cannot be ascertained. The People’s Bank of China reports that the value of the shareholdings of foreign investors in mainland China as of end-September amounted to roughly 3.54 trillion yuan ($500 billion), an increase of 12 % y-o-y. Foreign ownership represented a mere 3 % of total market capitalisation.

Policies have supported the stock markets, including deregulation in allowing insurance funds to increase their domestic shareholdings. Markets have also been supported after last spring’s dip in share prices through government urging of state-owned entities (“National Team”) to purchase shares. Some observers are concerned that the rise in share prices has ceased to be tied to real economy fundamentals.

Tech firms led last year’s rise in share prices on mainland China and Hong Kong exchanges

Sources: Macrobond and BOFIT.