BOFIT Weekly Review 12/2026

China’s budget promises no major changes from last year; large actual public sector deficit will persist

In conjunction with the March National People’s Congress (NPC), the finance ministry released last year’s budget report and its draft budget for the current year. The report showed that budget revenues last year fell by 2 % to 21.6 trillion yuan (15.4 % of GDP), while spending grew by 1 % to 28.7 trillion yuan (20.5 % of GDP). The difference was made up by withdrawals from state funds, resulting in a budget deficit of 5.7 trillion yuan (4.0 % of GDP). The finance ministry noted that keeping revenues and expenditures in balance this year is likely to be challenging. Budget expenditures are expected to rise by 4.4 % and budget revenues by 2.4 % from last year, clearly underperforming expected nominal economic growth. The deficit should remain at around 4 % of GDP.

Finance ministry concerns focus on falling budget revenues and the rising financial challenges facing local governments as traditional income sources such as the sale of land use rights dry up. Moreover, creation of a single national market remains elusive as some regional governments still grant unauthorised tax exemptions or subsidies to encourage investment. The ministry aims to address the issue this year. Government spending will be directed to technological innovation and industrial modernisation under the current five-year plan. Funds available to support science and technology will be increased by 10 % this year. Defence spending is also expected to rise by 7 %, roughly the same pace as in previous years.

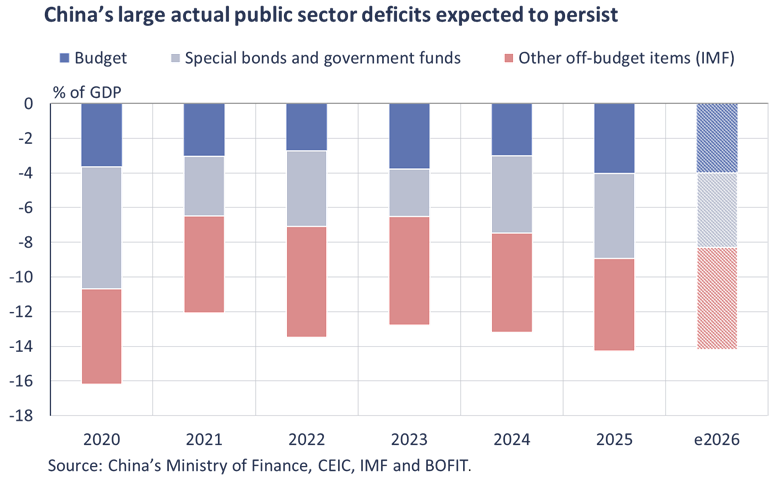

With large chunks of economic activity occurring outside the budget sphere, the budget itself cannot provide a comprehensive picture of Chinese fiscal policy. State funds are the most important off-budget items managed by the finance ministry as they are used to finance, among other things, a large share of investment projects and financial sector support measures, particularly through the use of special bonds (off-budget special treasury bonds from the central government and local government special bond issues). Like last year, the quota for local government special bonds this year is 4.4 trillion yuan. Part of the money raised will go to paying off “hidden” off-budget debt and payment arrears. Like last year, the central government this year plans to issue 1.3 trillion yuan in ultra-long treasury bonds. Of this, 250 billion yuan would go to financing the programme encouraging households to replace old appliances with new ones and 200 billion yuan to support businesses in updating their machinery and equipment. Overall, the combined amount is slightly less than the 500 billion yuan in funding provided last year. Capitalisation of large state-owned banks will be achieved though the issue of 300 billion yuan in special treasury bonds (500 billion yuan in 2025). Taking into account government funds, social security fund and the state capital budget revenues and expenditures, the deficit is expected to contract slightly from last year’s budgeted figures to just over 8 % of GDP. Still, this does not cover all public sector operations. IMF calculations of China’s public sector also include off-budget local government financial vehicles (LGFVs) and government funds, which are not included in the finance ministry’s definitions. Taking these into account, the IMF’s February Article IV consultation report concluded that China’s actual public sector deficit last year equalled 14.3 % of GDP and should remain at roughly the same level this year (14.2 % of GDP).

At the end of last year, central government debt amounted to 41.2 trillion yuan, while the official debt of local governments was 54.8 trillion yuan. Total official public debt at the end of the year was 69 % of GDP. The IMF estimates that China’s actual public sector debt is significantly larger when the “hidden” debt of LGFVs is included (51 % of GDP in 2025) and the debt of special construction and government guided funds, not included in the finance ministry figures (7 % of GDP). The IMF estimates that the actual debt liabilities of the public sector correspond to 127 % of GDP.

The IMF’s estimate of LGFV debt owed by local governments is many times larger than the figure reported by the finance ministry. An NPC presentation on progress in paying down LGFV debt claimed that 74 % of LGFV debt had been paid off over the past two years and that over 80 % of LGFVs are no longer be classified as such. The government has allocated 2 trillion yuan each year since 2024 to pay off hidden regional debt, as well as an additional 800 billion yuan last year to support debt resolution. The same is planned for this year. The finance ministry estimates that LGFV indebtedness at the end of 2023 amounted to 14.3 trillion yuan (11 % of GDP). The IMF, using a substantially broader definition of LGFVs than the finance ministry, found that LGFV debt as of end-2023 amounted to 64.4 trillion yuan and that debt continues to grow (71.4 trillion yuan as of end-2025). IMF experts are concerned that removing companies from the official LGFV list could lead to weaker oversight and potentially allow local governments to keep on increasing their off-budget debt.