BOFIT Weekly Review 50/2025

A weak yuan exchange rate this year has supported China’s exports

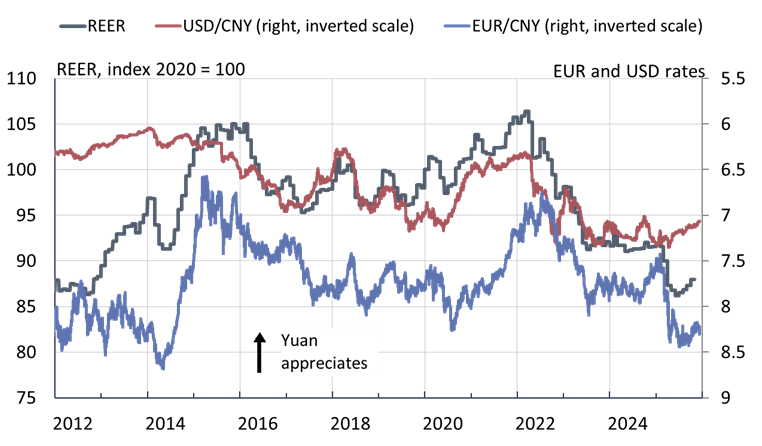

The People’s Bank of China effectively regulates the yuan’s exchange rate in relation to the dollar and in recent months has sought to rein in the yuan’s appreciation. Last week, for example, media reports claimed that China’s large banks had increased their dollar holdings in mainland China, which raised demand for dollars and correspondingly weakens the yuan. Although the dollar has fallen quite substantially since the start of this year (down 9 %), the yuan-dollar exchange rate has only been allowed to appreciate modestly (up 3 %). As a result the yuan has weakened since the start of this year by 9 % against the euro. China’s real effective (trade-weighted) exchange rate, REER, was 4 % weaker in October compared to the start of the year and, this year, has been at its weakest level since 2012.

Yuan weakness reflects such domestic factors as China’s low inflation and interest rates relative to the rest of the world. In November, consumer prices rose by 0.7 % y-o-y, while producer prices entered their fourth year of decline, falling 2.2 % y-o-y. China Customs reports that export prices in yuan terms were down by 4 % y-o-y in October.

Many analysts consider the yuan undervalued at the moment. The weak exchange rate supports exports and thereby economic growth. China’s current account surplus has swelled to a record high this year (four-quarter surplus of $654 billion or 3.4 % of GDP). The international Monetary Fund (IMF) commented this week that the yuan’s decline has contributed to the increase in China’s external imbalances. To remedy these imbalances, the IMF recommends that China boost its domestic demand by easing monetary and fiscal policy, reduce domestic imbalances by cutting back unwarranted industrial policy and overinvestment, as well as increase exchange-rate flexibility. European firms are also worried about their poor price competitiveness against Chinese companies.

The yuan has appreciated modestly against the dollar this year, but has weakened against the euro and in REER terms

Sources: Macrobond, BIS and BOFIT.