BOFIT Weekly Review 28/2025

International use of the yuan proceeds slowly, even though it is increasingly used in China's foreign trade

In a speech in Shanghai last month, China’s central bank governor Pan Gongsheng sketched out his vision for the future global currency system in which the yuan assumes greater significance and which would also reduce risks from the current system based on a dominant currency. Achieving this vision seems quite remote, however. Statistics show that international use of the yuan has not increased recently other than in China’s own foreign trade.

According to the Society for Worldwide Interbank Financial Telecommunication (SWIFT), use of the yuan in international payments declined to 2.9 % in May, down from 4.7 % in May 2024. The yuan also fell in the rankings behind Canadian dollar to the sixth-most-used currency in international payments. At the same time, the use of China’s own Cross-border interbank payment system (CIPS) has increased. The value of processed transactions in the system last year increased by more than 40 % from 2023 to 175 trillion yuan ($25 trillion). Over 1,500 foreign banks are already participating. It is estimated that the majority of CIPS payment messages are still handled via the SWIFT system. The financial newspaper Caixin, however, sites a source saying that the use of SWIFT messaging in CIPS has recently declined, which may also explain the decline in yuan use in SWIFT statistics. In recent months, CIPS has averaged around 30,000 payment transactions a day, which is still only a tiny fraction of SWIFT’s over 50 million daily payment messages.

After peaking in 2022, the yuan holdings of central banks have declined. IMF figures show that the yuan represented just 2.1 % of central bank allocated currency reserves as of end-March (2.8 % as of end-March 2022). The values of central bank reserves are reported in US dollars, so yuan depreciation against the dollar in recent years explains about half of the decline. In addition, the dollar’s share has also fallen slightly from three years ago (57.7 % in March 2025), while the euro’s share has increased a bit (20.1 %). Central banks have diversified their reserve holdings and increased the shares of other currencies. Central banks have also boosted their gold reserves.

Foreign investors have been skittish about investing in Chinese bonds. At the end of March, the value of foreign investment in mainland China's bond market was 4.4 trillion yuan ($610 billion), down from 4.6 trillion yuan in August 2024. This likely reflects the low yields on Chinese bonds and increased geopolitical risk. In recent years, Chinese interest rates have fallen to levels below those of most countries. The total holdings of foreign entities is small in Chinese bond markets (2.4 %).

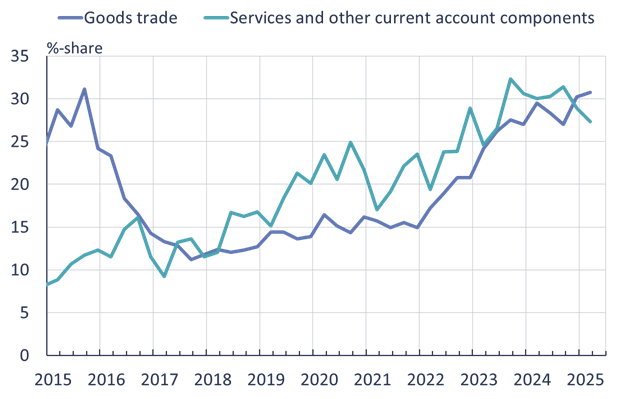

The use of the yuan has increased in China’s foreign trade. Part of the increase reflects trade with Russia, which has shifted away from dollar and euro and into yuan. In April, the People’s Bank of China was reported to have urged state-owned enterprises to prefer yuan in their foreign operations. In the first quarter of this year, 31 % of Chinese goods trade was conducted in yuan. A recent article published by the European Central Bank estimates that the yuan’s share of global exports has increased slightly, but remains very small (less than 2 %). The shares of US dollar and the euro have both remained roughly at 40 %. The yuan’s share of export invoicing has grown fastest in Europe (again, largely due to Russia trade) and in Asian countries (but even in those regions represents only 1.5–2 % of the value of exports). Yuan invoicing of exports in Africa and the Middle East is essentially non-existent. The study found that the use of the euro and dollar has fallen in recent years most in Russia, Belarus and several countries in Central Asia.

The yuan’s use in China foreign trade has again increased, approaching its 2015 peak

Sources: PBoC, SAFE, CEIC and BOFIT