BOFIT Weekly Review 22/2025

China’s economic trends remained relatively strong in April

Despite the unprecedented flaring of the US-China trade war in the first half of April, China’s official economic figures released for April show little indication of a significant economic slowdown. The yuan’s weak exchange rate and falling prices continue to boost price competitiveness of Chinese exports. In April, the volume of goods exports rose by 13 % y-o-y, while the volume of imports posted no growth. Industrial output figures were also lifted along with the robust export figures. Industrial output in April grew by 6.1 % y-o-y, nearly matching the pace of growth in January-March (6.5 %) and slightly higher than growth last year. It appears, however, that industrial output growth might be slowing in coming months. For example, the manufacturing purchasing managers index (PMI) reading for April showed a deteriorating corporate outlook.

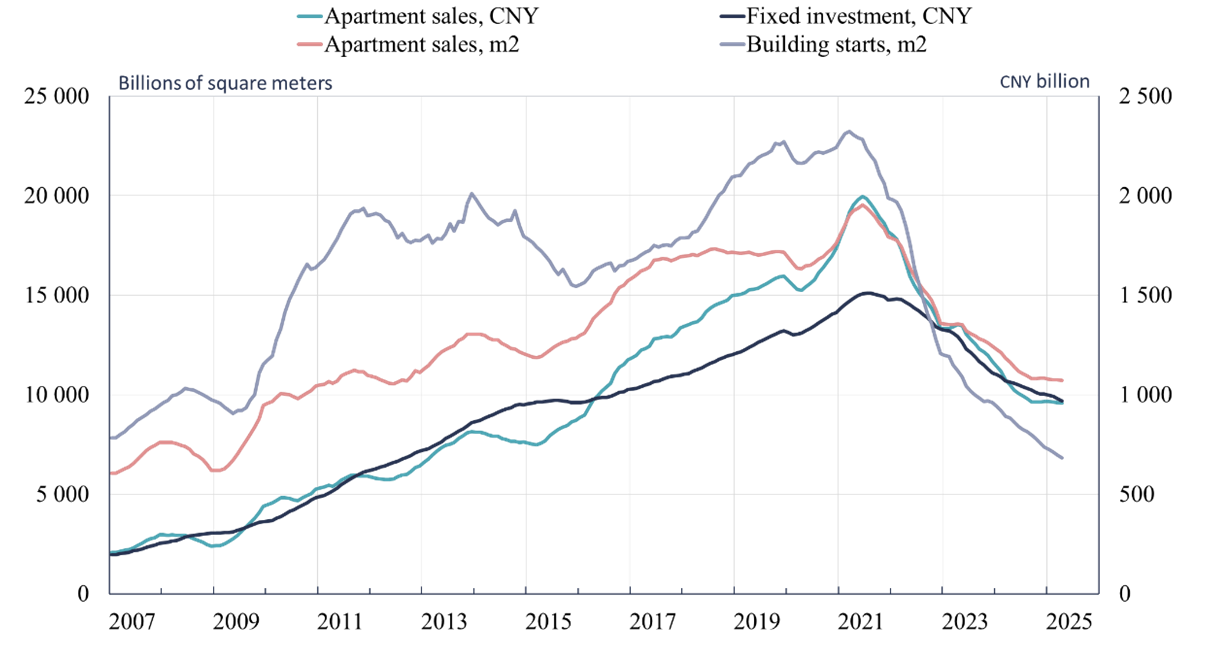

Nominal growth in fixed investment in the first four months of this year generally remained as strong as last year. Nominal investment grew approximately 3.4 % y-o-y in April, a bit off the 4.2 % pace of January-March. Investment by state-connected firms grew fastest, while fixed investment by foreign firms operating in China continued to plummet. Investment in real estate remained in steep decline (down 10 % in January-April) and the volume of new building starts was down sharply (a decline of over 20 % y-o-y in terms of floorspace). On the other hand, apartment sales show signs of stabilising. The volume of sold apartments (floorspace) in January-April was only down by 2 % y-o-y (in the same period in 2024, the drop exceeded 20 % y-o-y). Ending the collapse of the real estate sector has long been a top economic policy priority for the government, and a number of new measures to support the housing market was introduced last autumn.

China’s real estate sales appear to be stabilising.

Note: 12-month moving sum.

Sources: China National Bureau of Statistics, CEIC and BOFIT.

Another area of government policy emphasis has been reinforcing domestic consumer demand. Government efforts to stimulate consumption by offering households rebates for replacing old household appliances with new ones seems to have succeeded. In January-April, sales of household appliances grew by 24 % y-o-y in nominal terms. The value of sports equipment sales also grew by over 20 % y-o-y, while the value of food sales rose by 10 %. Real growth in retail sales overall was quite robust in the first four months of this year (up 5 % y-o-y).

Heavy reliance on exports as a driver of growth and a raging trade war make Chinese decision-makers worry about economic growth, as this year’s GDP growth target was set to ambitious “about 5 %”. To even come near this target, the government has had to resort to fiscal and monetary measures to support the economy. The monetary stance was slightly relaxed at the beginning of May to make it even more accommodative. The central government’s financing deficit in January-April was roughly 0.5 % of GDP larger than a year earlier as expenditures rose by 9 % y-o-y and revenues declined by 4 %. At the same time, local governments have issued an exceptionally large amount of new special purpose bonds for financing investment projects and paying off existing “hidden debts” carrying high interest rates (BOFIT Weekly 46/2024).