BOFIT Weekly Review 20/2025

People’s Bank of China eases monetary stance and increases quotas for targeted lending programmes

China’s central bank, the People’s Bank of China continued cautiously moving to an easier monetary policy stance last week. Markets have been expecting the change since late last year. After months of calls by party leaders for a more accommodative monetary stance, the PBoC, China’s National Financial Regulatory Administration (NFRA), and China Securities Regulatory Commission (CSRC) jointly announced new easing measures on May 7.

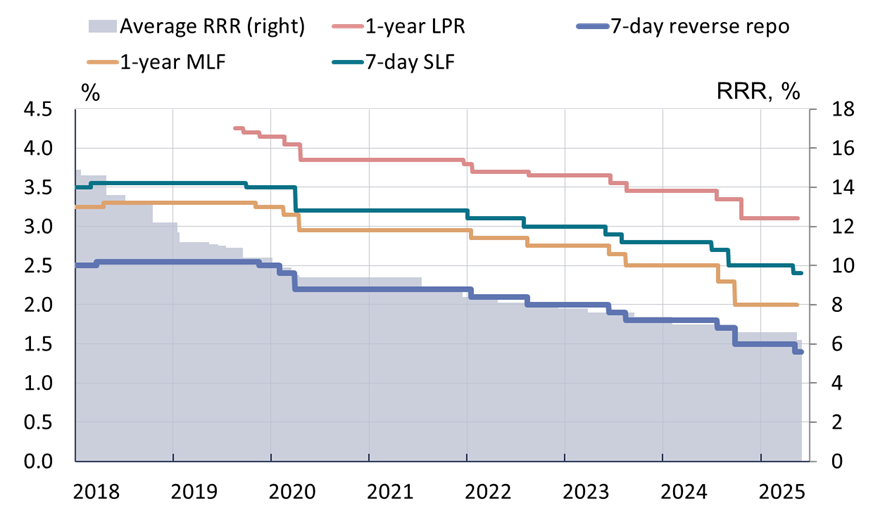

The 7-day reverse repo rate, which is used by the PBoC in its open market operations, was lowered by 10 basis points to 1.4 %. The PBoC has announced plans to adopt the 7-day reverse repo rate as its main policy rate from which other policy rates are priced. When the latest rate cut is included, the PBoC has lowered the 7-day reverse repo rate by a total of 80 basis points since spring 2020. The interest rate on standing lending facility (SLF) loans was also lowered by 10 basis points. Under the SLF programme, the PBoC provides commercial banks with short-term funding as needed. Loans must be secured by collateral and carry relatively high interest rates. Adjustments to the loan prime rate (LPR), which serves as the reference rate for pricing bank loans, are published on the 2oth of each month. A cut in the LPR is also expected.

The PBoC lowered the reserve requirement ratio (RRR) for commercial banks by 50 basis points on Thursday (May 15). China’s smallest banks, however, were not included in the changes as they already enjoy the lowest allowed RRR (5 %). The reserve requirement for firms providing car loans and leasing services was lowered from 5 % to 0 % to bolster car sales. The PBoC noted that the banking sector’s average weighted reserve requirement fell from 6.6 % to 6.2 % and this will increase market liquidity by about 1 trillion yuan.

The PBoC has also expanded its targeted lending programmes. The latest 500-billion yuan lending facility was established to support consumption of services and elder care. In addition, funding for two existing programmes (one to foster technological innovation and the other to support rural development and help small businesses) each received a 300 billion yuan increase in their total quotas. The central bank uses these structural lending facilities to offer commercial banks cheaper financing for specified lending purposes. The number of the facilities has increased in recent years, and there are now a dozen such programmes. Most programmes do not reach their maximum lending quotas. For example, although the quota for the technological innovation facility has been raised to 800 billion yuan, the PBoC’s latest figures from end-September show that total lending only amounted to 700 million yuan at that time. On the other hand, the lending quota for the rural development and small businesses facility has been increased to 3 trillion yuan, and as of end-March the lending balance was already 2.4 trillion yuan. The total balance of the structural lending facilities this year has shrunk. PBoC figures show it was 5.9 trillion yuan (750 billion euros) as of end-March, 22 % smaller than a year earlier.

Interest rates for structural lending facilities were also reduced by 25 basis points. The same rate cut applies to the pledged supplementary lending (PSL) programme for the country’s policy banks. Commercial banks have also committed to reducing the interest rates of the Housing Provident Fund (HPF) by 25 basis points. The HPF is used to offer inexpensive housing loans. The interest rate on loans for first-home buyers with a maturity of over five years was lowered to 2.6 %, while and loans with shorter maturities declined to 2.1 %. Loans for the purchase of a second apartment must be priced at least 42.5 basis points above the first-house rates. Interest rates on market-based housing loans (to borrowers who do not qualify for the HPF) are typically higher.

China’s current economic conditions are conducive to accommodative monetary policies. Consumer price inflation has been slightly negative for the past three months, and consumer prices fell by 0.1 % in April. The relatively swift decline in producer prices has also continued (down 2.7 % in April). With the announcement of a temporary pause in the trade war last weekend, the yuan’s exchange rate strengthened, a welcome trend from the central bank’s perspective. The PBoC has this year slowed down yuan’s depreciation against the dollar. These measures, however, are unlikely to provide support that boosts significantly economic growth. Monetary policy actions can increase the supply of financing available or lower its price. Currently financing demand in China is mostly limited by other factors, such as increased uncertainty and the depressed housing market.

The PBoC has gradually lowered interest rates and bank reserve requirement ratios (RRRs) in recent years.

Sources: People’s Bank of China, CEIC and BOFIT.