BOFIT Weekly Review 19/2024

Russian economy cooled in March; latest forecasts expect GDP growth of 2–3 % this year

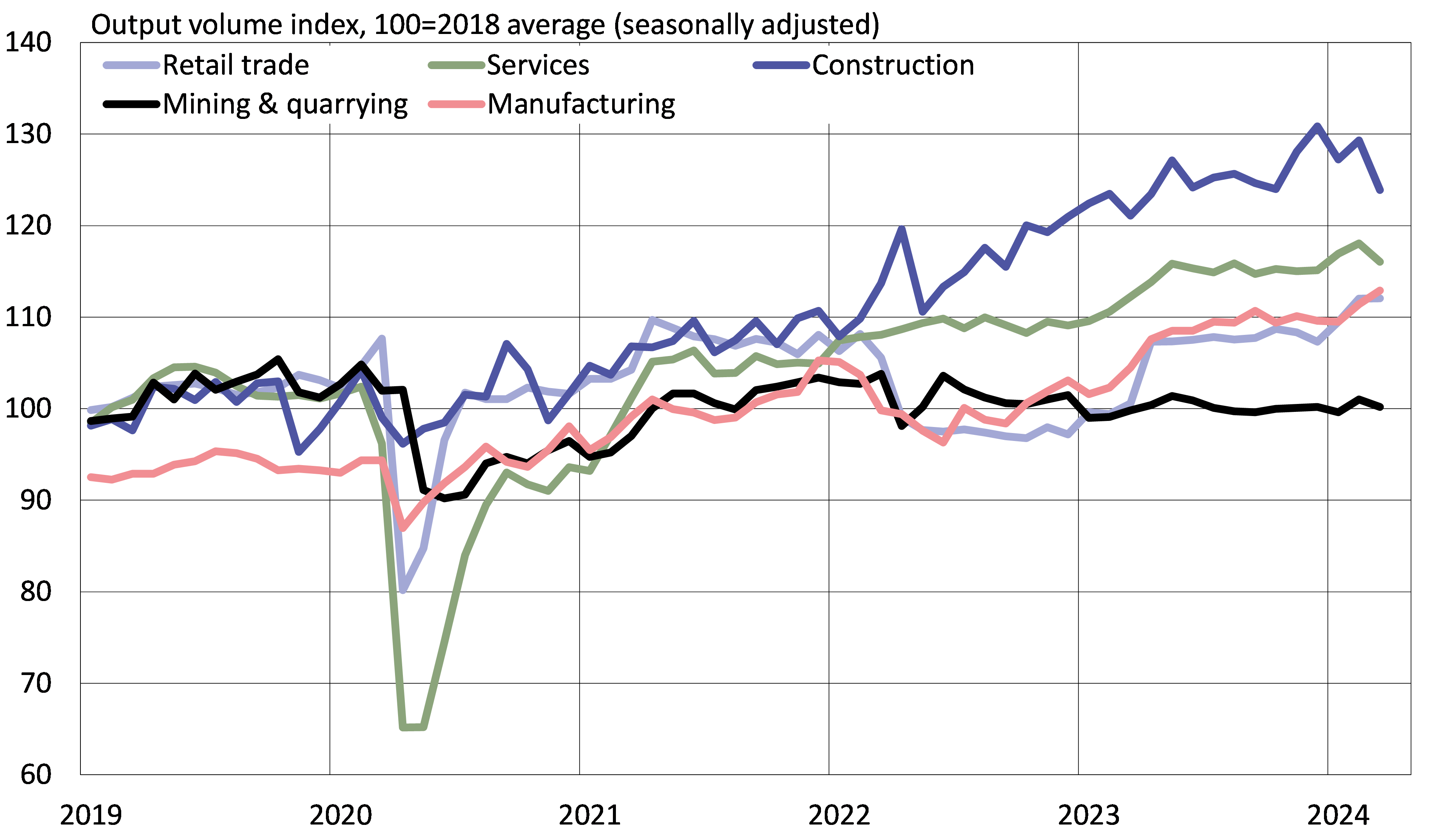

The level of output dipped slightly in March (seasonally adjusted) in nearly all core sectors of the economy. In annual terms, output was still up in most sectors, but the pace of growth slowed.

Growth in construction, which has boomed for months, slowed sharply in March to 2 % y-o-y, its lowest level in over two years. Mining & quarrying output remained at the same level as a year earlier. While retail sales continued to show strong growth (11 % y-o-y), part of the effect still reflects last year’s low basis reference.

The on-year pace of manufacturing growth slowed to 6 % in March. Manufacturing, driven by industries linked to the war effort, was the only core sector of the economy to post on-month (seasonally adjusted) growth. After a slight slowdown at the end of last year, military-related manufacturing saw a burst of growth in the first quarter. The role of war-related production in Russia’s current economic performance is discussed in a recent post on our BOFIT blog.

Russia’s economic development ministry estimates that 12-month GDP growth slowed considerably in March from February’s robust figure. February growth was boosted, among other things, by an extra leap-year workday. The economic development ministry and the central bank consider growth in the first months of this year faster than expected and have revised upwards their forecasts for 2024 GDP growth. The economic development ministry now expects GDP to rise by 2.8 % this year and 2.3 % next year. The revised forecast of the Central Bank of Russia sees GDP growth in the range of 2.5–3.5 % this year and 1–2 % next year. Among the most recent international forecasts, the OECD last week announced that it expects Russian GDP to grow by 2.6 % this year and 1 % next year. The averages of major forecasts reported in the April Consensus Economics report were 2.3 % for this year and 1.4 % next year.

Output stumbled in March in all core sectors with the exception of manufacturing

Sources: CEIC, Rosstat and BOFIT.

Inflation still high

Russian prices have continued to climb in recent months, with March consumer prices up by 8 % y-o-y. The central bank estimates that 12-month inflation remained at about the same level in April. At its regular interest-rate meeting in late April, the CBR board decided to keep the key rate unchanged at 16 %, where it has remained since December.

The CBR and the economic development ministry have raised their inflation prognoses for this year. The CBR now expects inflation to slow to around 4.3–4.8 % by the end of this year, while the economic development ministry only sees inflation falling to 5.1 %. In its April report, Consensus Economics noted that the average of major inflation forecasts for Russia this year was 5.3 %.

The CBR sees inflation risks still elevated. Economic overheating could persist if productivity fails to keep up with rapid wage increases and supply fails to keep up with demand due to labour shortages and complications in machinery and equipment imports because of sanctions. Fiscal policy is also a risk to fuel faster inflation.

The latest CBR forecast sees its key rate remaining at its current high level for longer than it expected earlier. The central bank now anticipates the key rate to average 15–16 % this year and 10–12 % next year. The CBR does not rule out future rate hikes, even if they are not included in the current baseline forecast. New macroprudential measures to be introduced at the start of July are designed to rein in risks emerging from rapid growth in unsecured consumer credit.

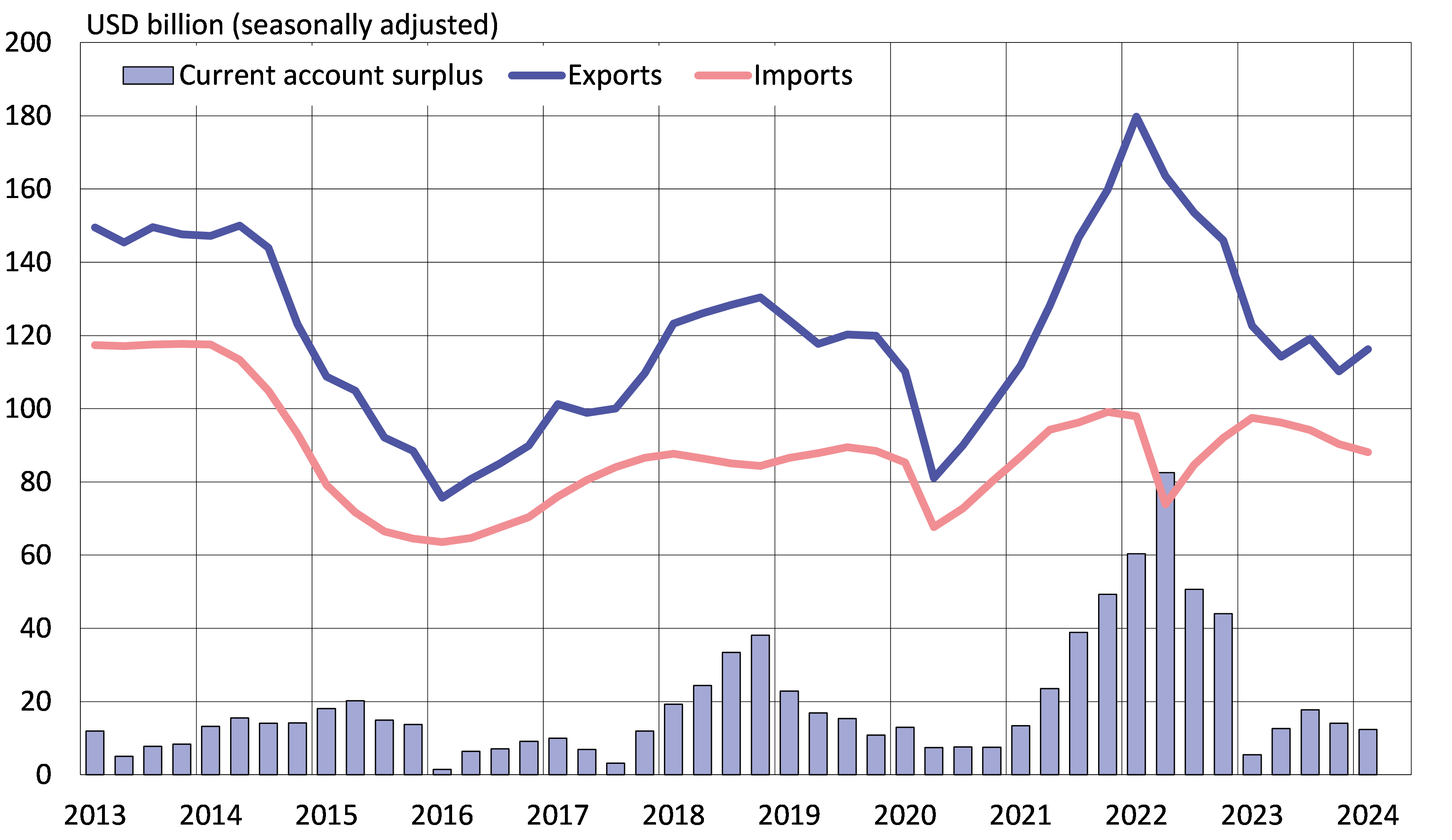

Export earnings flat; imports continue to dwindle

According to preliminary balance-of-payments figures released by the CBR, the seasonally-adjusted value of goods and services exports in the first quarter was close to the level of previous quarters. The International Energy Agency estimates the export price of Russian crude oil averaged about $70 a barrel in January-March, or about the same level as in the fourth quarter of last year. The volume of exported petroleum products contracted in the first quarter with the reduction in Russia’s refining capacity from Ukrainian drone strikes and the government’s ban on gasoline exports at the beginning of March. The reduction in exports of petroleum products, however, has been offset by increased exports of crude oil. Prices of many of Russia’s top export commodities have fallen and Western sanctions have been imposed on new categories of Russian goods such as precious stones. The redirection of Russian exports to Asian markets continues. Russian Customs reports that Asia accounted for 77 % of Russian goods exports in January-February.

Imports were still close to pre-invasion levels at the beginning of 2023, but the drop in the value of goods and services imports that began last year extended into the first quarter of this year. The value of imports in 1Q24 was roughly the 2019 average. The CBR notes that the contraction in imports reflects multiple factors, including weakening of the ruble, a build-up of inventories and difficulties in settling international payments. In addition, imports appear to have been slowed by tighter enforcement of Western export restrictions. The biggest factor in reducing services imports has been the decline in foreign travel. Nearly half of Russian tourists travelling abroad last year went to Turkey. The CBR estimates that the rapid depreciation of the ruble and Turkey’s galloping inflation dampened demand for travel to Turkey. Asian countries continued to increase their dominance as suppliers of goods to Russia. Russian Customs figures show that Asian supplies accounted for 68 % of Russian goods imports in January-February.

Russia’s current account has continued on surplus this year. The surplus for the first quarter of 2024 amounted to $22 billion. The CBR said the surplus was augmented by the contraction in imports, reduced payment of dividends to investors abroad and a reduction in transfers by private persons to accounts abroad. On the financial account, the established trend of a net outflow of capital from the country continued in the first quarter. On the other hand, the net withdrawal of assets from Russia by foreign investors moderated from previous quarters, falling to around $4 billion. Russian receivables from abroad increased to $23 billion in the first quarter. The CBR reports that some of the rise reflects an increase in export receivables caused by longer lags in payments from foreign buyers.

Russia posted another current account surplus in the first quarter of this year

Sources: CEIC, Central Bank of Russia and BOFIT.