BOFIT Weekly Review 12/2024

Cautious signs of economic recovery in China

The National Bureau of Statistics (NBS) this month has reported a number of figures for January and February. One reason for presenting multi-month numbers is the timing of the Chinese Lunar New Year festivities, which changes from year to year and makes monthly comparisons across years quite challenging. The Lunar New Year holidays this year fell entirely in February, while last year they were in January. The combined figures for January and February indicate some degree of economic recovery despite continuing headwinds facing the Chinese economy.

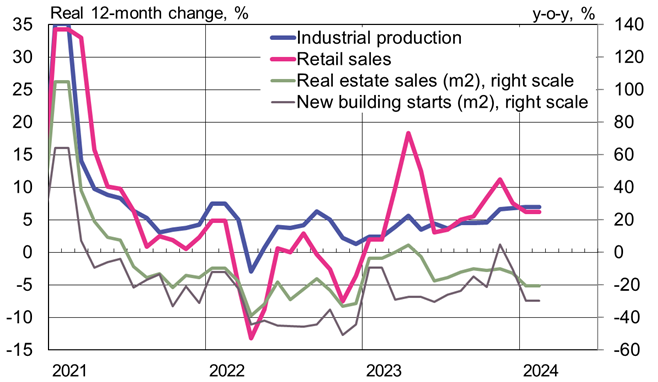

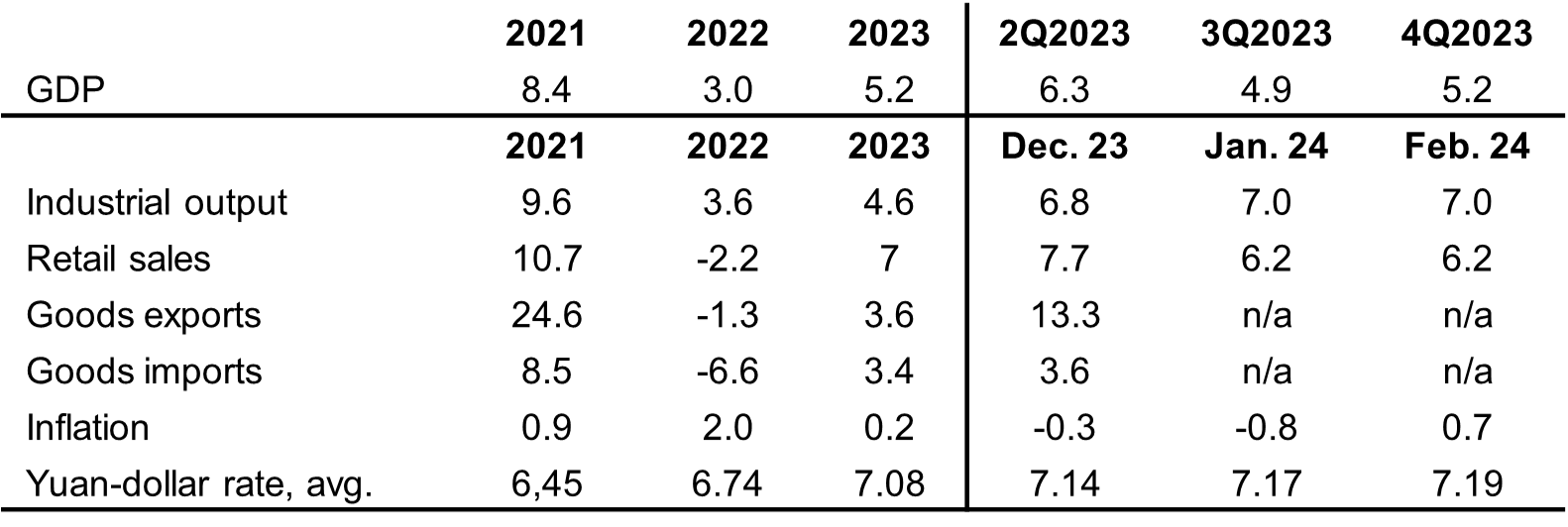

Real growth of Chinese industrial output accelerated slightly to just over 7 % y-o-y (6.8 % in December). Fixed investment in nominal terms grew by just over 4 % y-o-y, up from 3 % for all of 2023. China’s statistical reporting on fixed asset investment is rather limited, making it hard to assess ongoing activity. The pickup in fixed investment is likely due to the government’s stimulus measures. Fixed investment of state-led enterprises was up by over 7 % y-o-y in the first two months of this year, while investment by private firms showed virtually no growth. Industrial investments, in particular, were up by 12 % y-o-y, while the revival in services sector investment was more subdued (up 1 %). China’s foreign trade also picked up in the first two months of this year. The value of China’s goods exports in January-February was up by 7 % y-o-y in dollar terms (10 % in yuan terms). Goods exports contracted by nearly 5 % last year. Import growth was more modest, under 4 % y-o-y (7 % in yuan), yet imports returned to growth territory after last year’s near 6 % drop.

China’s real estate sector has yet to hit a bottom. Real estate investment in January-February was down by 9 % y-o-y and housing sales dropped by 21 % (measured by floorspace). The downturn in the real estate market weakens consumer confidence and willingness to consume as the lion’s share of household wealth in China is tied up in real estate. China’s labour market has softened slightly in recent months and urban unemployment bumped up slightly to 5.3 % in February. Information is not collected about unemployment in rural areas, and there is no information yet available on movements of China’s internal migrants. Retail sales in January-February rose in real terms by 6.2 % y-o-y, slowing somewhat from the final months of 2023. Domestic travel during the Lunar New Year holiday week was brisk; travel (measured by number of journeys) grew by 34 % y-o-y and was up by 19 % from pre-pandemic 2019. Consumption increased during the New Year’s break, with domestic tourists spending 47 % more than last year and nearly 8 % more than in 2019. Nonetheless, consumers appeared more cautious, as spending per journey was below pre-pandemic levels.

Industrial output growth picked up in the first two months of this year, but real estate sales entered their third year of decline

Note: The calculation for real growth in retail sales is based on consumer price inflation for those months when real growth was not reported.

Sources: China National Bureau of Statistics, CEIC and BOFIT.

Growth in the credit stock slows even with a modest monetary easing

In a press conference during the National People’s Congress in March, People’s Bank of China governor Pan Gongsheng gave assurances that monetary easing to support the economy was still possible and that the central bank has a large policy toolbox for dealing with this. He said that there is still room to further lower reserve requirements. The PBoC eased its monetary policy this year by reducing the reserve requirement for commercial banks by 50 basis points, effective as of February 5. Last month also the over 5-year loan prime rate (LPR) that is used as housing loan reference rate was lowered by 25 basis points to 3.95 %. The measure was intended to boost housing sales. The shorter-term 1-year LPR was kept unchanged at 3.45 %. LPR reference rates have remained unchanged this month. Due to the lack of demand in money markets, the PBoC’s open market operations in January and February drained market liquidity significantly. Interest rates on money markets have also declined this year.

Growth in the bank credit stock slowed to 9.7 % y-o-y in February (10.8 % in February 2023). On-year growth in aggregate financing of the real economy (AFRE) slowed to 9 %. Of the subcategories, government debt grew rapidly (up by 15 % y-o-y). Money supply growth has slowed considerably over the past year. In February 2024, broad money (M2) supply grew by 8.7 % y-o-y, down from 12.9 % a year earlier.

After several months of decline, consumer prices began to rise in February, lifting consumer price inflation to 0.7 % p.a. Core inflation, which does not include prices of food and energy, rose by 1.2 %. The yuan’s exchange rate has remained stable in recent months in terms of its trade-weighted (REER) measure and relative to the US dollar and the euro. One dollar currently buys 7.2 yuan and one euro 7.8 yuan.

After a declining trend last year, consumer inflation picked up in February

Sources: China National Bureau of Statistics, Macrobond and BOFIT.

Real 12-month change and consumer prices, %

Sources: China National Bureau of Statistics, China Customs, WTO, CEIC and BOFIT.