BOFIT Weekly Review 3/2024

Russia plans further increases in government spending despite deficits

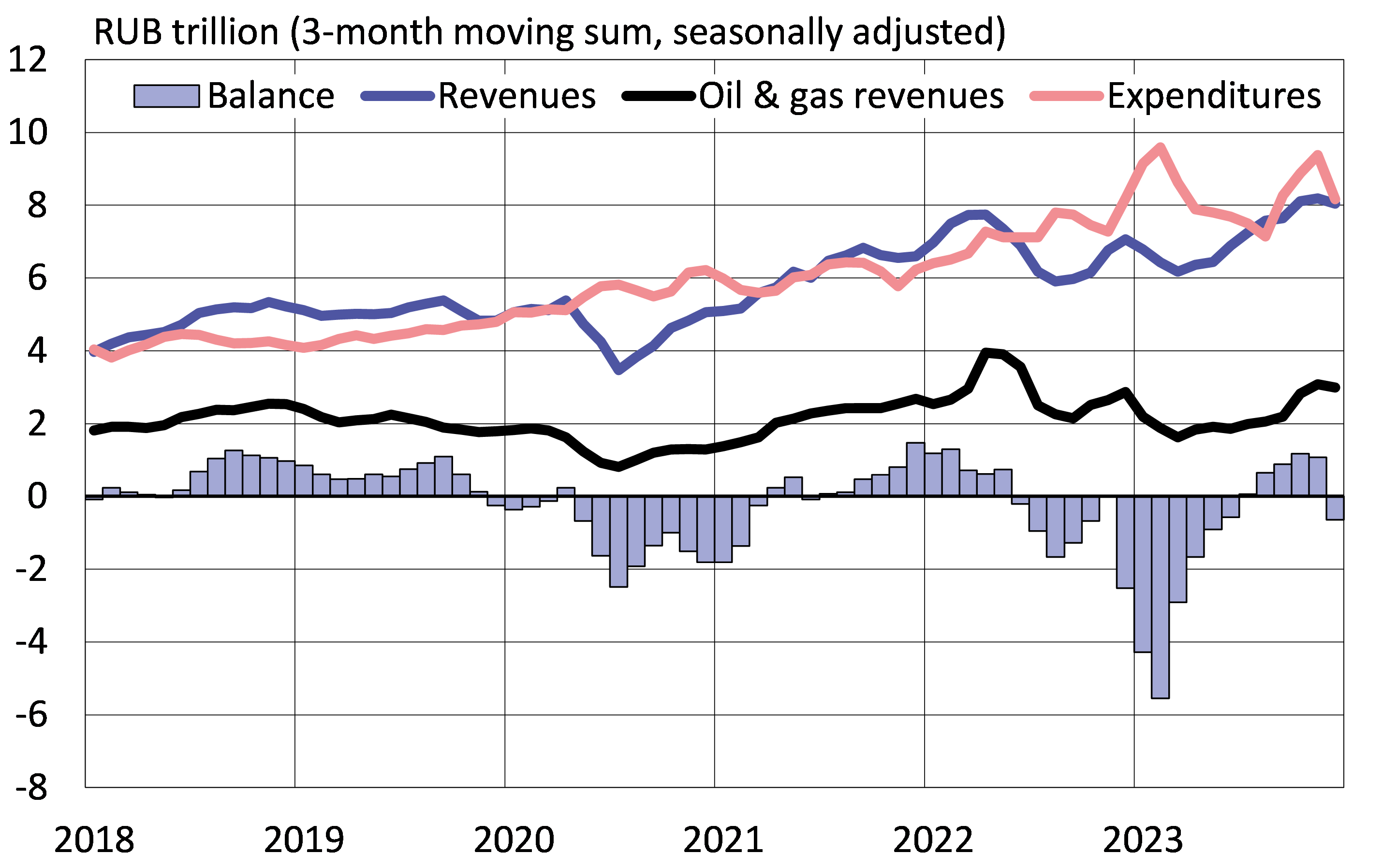

Russia’s federal budget remained in deficit in 2023

According to the preliminary assessment released by Russia’s finance ministry, federal budget revenues grew last year by 5 % and amounted to 29.1 trillion rubles (340 billion dollars based on the Central Bank of Russia’s official average exchange rate). Revenues were also roughly 3 trillion rubles higher than expected under the budget plan approved in December 2022.

Oil & gas revenues, however, contracted by 24 % to 8.8 trillion rubles and accounted for 30 % of total federal budget revenues. The finance ministry reports that the average export price of Urals blend crude in 2023 was 63 dollars a barrel, down from 76 dollars a barrel in 2022. As global oil prices increased in the second half of last year, Russia’s total oil & gas revenues in 2023 climbed to nearly same level as in 2021. Other federal budget revenue streams grew by 25 % last year. Major revenue streams such as value-added taxes (VAT) were up by 22 % and corporate profit tax revenues by 15 %.

Federal budget spending last year reached 32.4 trillion rubles (380 billion dollars), a 4 % increase from 2022. The spending burst particularly at the end 2022 - start 2023 and again in last autumn. Spending exceeded the amount budgeted in December 2022 by 3.2 trillion rubles. Detailed information on the structure of spending last year was not released.

The federal budget deficit last year amounted to roughly 3.2 trillion rubles (37 billion dollars), which, according to the finance ministry, corresponded to about 2 % of GDP. The deficit was about 300 billion rubles larger than anticipated under the budget framework. The deficit was only slightly smaller than in 2022.

Russia’s federal budget spending peaked around the turn of the year in 2023 and again in the autumn

Sources: CEIC, Russian Ministry of Finance, BOFIT.

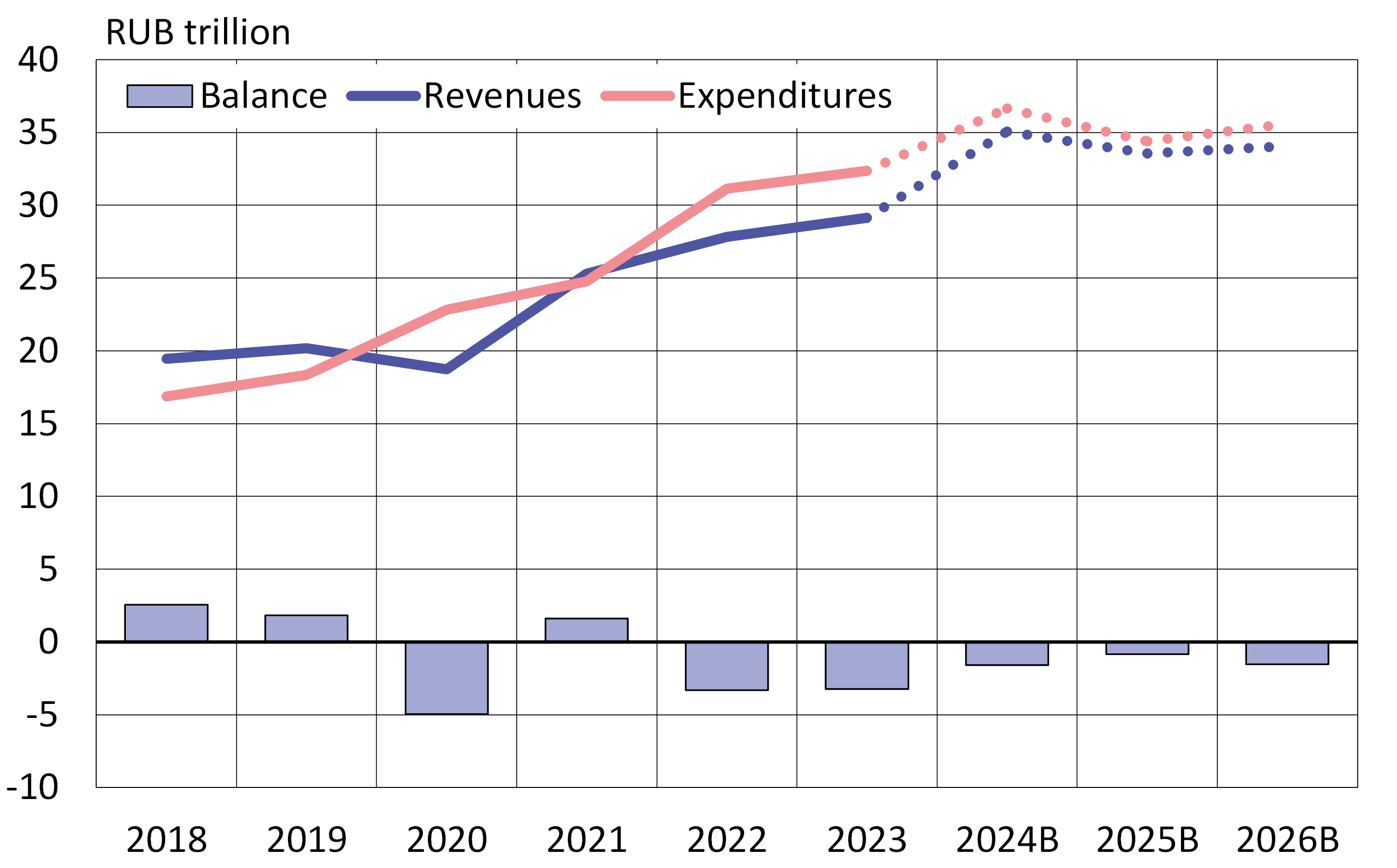

Major spending increases planned for this year focus on defence

Expenditures in this year’s approved federal budget are 13 % higher than the preliminary estimate for realised 2023 spending. Most forecasters expect Russian consumer price inflation to average about 5 % this year, so spending will rise sharply even in real terms. The higher spending levels should give a boost to Russian GDP growth. Public sector consumption last year represented about 20 % of GDP. A significant share of fixed investment was also financed out of the federal budget.

The government is planning for large increases in Russian federal budget spending this year

B = approved 3-year budget framework

Sources: CEIC, Russian Ministry of Finance, BOFIT.

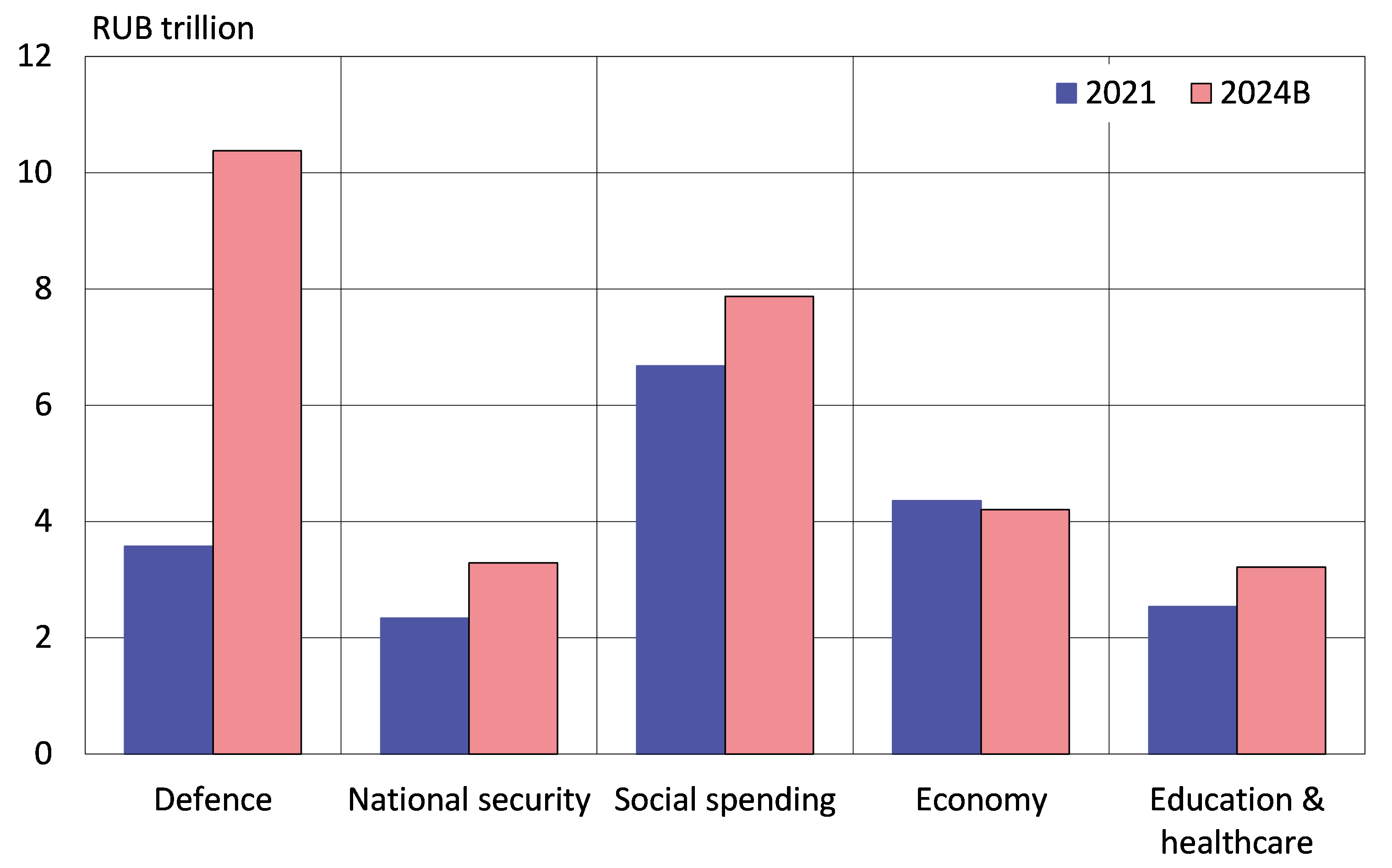

Although Russia no longer publishes information on the structure of realised budget spending, the spending categories for future budgets are set out in the budget framework. Defence, at 10.4 trillion rubles (about 120 billion dollars), is the largest spending category in this year’s budget. Defence spending represents about 28 % of total federal budget spending. Spending related to the war effort is included also in other spending categories, like national security, which represents 9 % of budget spending this year. Social spending, the next largest spending category after defence, represents 21 % of total federal budget spending. This year’s defence spending is nearly triple that of 2021, while the amount of spending on economic development is slightly less than in 2021.

Russia plans to nearly triple 2024 defence spending from 2021 levels

Sources: Russian Ministry of Finance, BOFIT.

Revenues to this year’s federal budget are expected to surpass the preliminary estimate of 2023 revenues by 20 %. Oil & gas revenues should increase by 30 % and other revenue streams by 16 %. The budgeting process for oil & gas revenues uses an assumed average export price of 70 dollars a barrel for Urals crude. As the basis for oil taxation this year, the average world market price of a barrel of Brent crude minus a 15-dollar discount will be used. Futures markets currently predict an average Brent price this year of around 77 dollars a barrel. Based on current market projections, the price of oil should come in below the budget assumption.

This year’s federal budget plan calls for a deficit of 1.6 trillion rubles. The finance ministry estimates that such a deficit would correspond to roughly 1 % of GDP this year.

Considerable uncertainty surrounds 2025–2026 budget plans

Russia’s latest budget framework extends through the 2025–2026 budget. There has often been, however, much uncertainty related to the plans for years further ahead. The current risks arising from war are exceptionally large.

The proposed 2025 federal budget would show a deficit of just 830 billion rubles (0.4 % of GDP). This figure, however, is based on a roughly 6 % cut in nominal spending. The reduction in purchasing power of spending due to inflation is larger, of course, and would have a significant negative impact on GDP growth. As a result, such a large spending cut seems unrealistic at the moment.

Federal budget spending in 2026 would increase slightly. Thus, the 2026 deficit is predicted to be about 1.5 trillion rubles (0.8 % of GDP).

Russia still has options in financing its budget deficits

Russia’s total 2022–2023 federal budget deficit amounted to roughly 6.5 trillion rubles. The shortfall was financed out of funds set aside from oil & gas earnings and the issuance of domestic bonds. The government plans to resort to the same measures in financing future budget deficits. For the 2024–2026 period, the budget deficit is expected to amount to roughly 4 trillion rubles.

Although Russia deposited no oil & gas income in the National Wealth Fund (NWF) last year, ruble depreciation supported the value of the NWF in ruble terms. Most of the total 3.5 trillion rubles withdrawn from the NWF last year went to covering the federal budget deficit. Since March 2022, roughly 6.5 trillion rubles in assets have been drained from the NWF. Besides being used to finance budget shortfalls, NWF assets have been used to purchase equity and debt securities of Russian firms.

The total value of the NWF at the end of last year was 12 trillion rubles (about 133 billion dollars or 8 % of GDP). About 5 trillion rubles in NWF assets at the end of last year were considered “liquid,” i.e. assets that can be accessed quickly to finance budget deficits as they arise. About 60 % of liquid assets are invested in Chinese yuan-denominated assets and the remainder is held in gold. Non-liquid NWF assets are mostly invested in shares and obligations of large Russian firms such as Sberbank.

The Russian state has increased its borrowing in recent years. Although domestic debt (including government guarantees) rose by a total of roughly 6.7 trillion rubles in 2022–2023, it is still relatively small by international standards. As of end-2023, Russia’s government debt amounted to about 18 % of GDP.

Russia should have little difficulty covering its budget deficit this year, even if it is larger than expected. Indeed, the projected deficit for the 2024–2026 budget framework could be covered entirely out of NWF withdrawals. The 2024–2026 budget plan currently seems rather optimistic as the ongoing war in Ukraine and other geopolitical instability pose large risks to government finances.