BOFIT Weekly Review 40/2023

China and US governments attempt to increase communication to heal frayed economic relations

The leadership in both China and the United States have recently stepped up their frequency of meetings and contacts. The hope is to relax the tense relations between the two countries, increase the exchange of views and reduce the likelihood of a mutual misunderstanding. At the same time, economic “decoupling” of the two nations continues, with US firms operating in China also feeling the pressure.

The US and China announced in late September the launch of two new working groups to deal with bilateral economic and financial market issues. The US treasury department reports that the Economic Working Group, in cooperation with China’s finance ministry, will look into ways to bring bilateral relations back into balance and address global issues such as debt restructuring for poorer countries. The Financial Working Group, which involves cooperation with the People’s Bank of China, will pursue regulatory and financial stability issues. Regular economic discussions ended in 2018 after the Trump administration pulled out of the talks. This month’s announcement of renewed discussion was preceded by the August visit of US commerce secretary Gina Raimondo to China. As part of her visit, the countries established a separate working group to deal with bilateral commercial issues and information exchange mechanism on the use of export controls. The commercial issues working group will meet twice a year, with its first meeting taking place in early next year. China earlier this summer hosted visits by US secretary of state Antony Blinken, treasury secretary Janet Yellen and presidential climate envoy John Kerry.

Even with the improved dialogue between the two countries, bilateral business relations continue to degrade. In addition to last year’s restrictions on the export of sensitive technologies, US president Joe Biden issued an executive order in August that permits banning or restricting new US investment in Chinese firms involved in quantum computing, artificial intelligence or the manufacture of advanced microchips. The executive decree is due to enter into force next year. China, among other things, has invoked “national security” by banning the use of US chipmaker Micron’s products in critical infrastructure and, in July, restricted the exports of germanium- and gallium-related compounds used in microchip production. Bilateral tensions have also been inflamed by US claims that Chinese firms are providing Russia, either directly or indirectly, with technology used in its war of aggression on Ukraine. In September, the US placed ten more Chinese firms and one person on its Entity List. The firms were accused of providing military assistance to Russia and Iran. In August, the US removed 27 Chinese firms from being added to the Entities List after officials announced that they had completed their end-use investigations into the firms and established that they were competent to receive US exports, such as technology.

In September, the American Chamber of Commerce in Shanghai (AmCham) released its annual report, which showed that US companies in China have become more pessimistic about the Chinese markets and operating environment. Only 52 % of respondents said they were optimistic about the upcoming five years of operation in China, which was the lowest AmCham survey reading in its 25-year history. Only 40 % of respondents expected their medium-term revenue growth in China to exceed their global revenue growth. Over the medium term, the biggest challenge will continue to stem from tensions between the US and China. Most firms said that they had experienced pressure from government authorities to manifest efforts at decoupling. Two-thirds said that the most pressure was coming from the US government, while the remainder said it was coming from the Chinese government.

China was the top supplier of US goods imports up until last year. Mexico surpassed China this year. China currently provides about 14 % of US goods imports, while China takes about 8 % of US goods exports. The punitive import tariffs imposed in 2018–2019 during the Trump administration remain in force, and there has been little change in the tariff scheme in recent years. According to the Peterson Institute for International Economics (PIIE), the average US import duty rate on Chinese imports is currently 19 % and the average Chinese duty on imports from the US is 21 %. PIIE estimates show that the US has imported little in the way of goods from China in categories subject to higher duties throughout the trade war. The imports of such goods from the rest of the world has increased. The highest 25 % import duties, which target such products as semiconductors and consumer electronics, have caused imports from China to fall significantly. By the same token, higher imports from China are almost exclusively in categories not subject to the additional duties. Some of the drop in the Chinese imports is likely explained by the fact that also some Chinese companies have moved US export production out of the country (to Mexico for example) to avoid the higher tariffs.

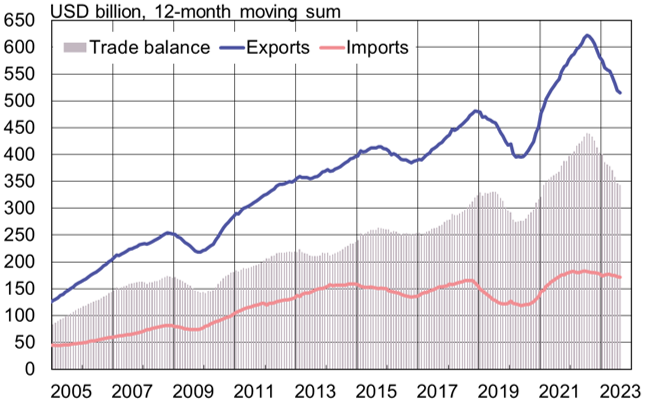

In 2017, the US accounted for 19 % of China’s goods exports. That share has fallen currently to 15 %. US share in China’s goods imports are now less than 7 % (over 8 % in 2017). China Customs figures show that China’s goods exports to the US fell in January-August by 17 % in dollar terms (total exports down by 5 %). The value of goods imports from the US contracted by just 5 % (total imports down by 8 %), and the goods trade surplus started to shrink. The biggest export categories were machinery & equipment (42 % of the value of exports), clothing & textiles (10 %), as well as certain types of manufactured goods (14 %). During January-August, exports in these categories fell at roughly the same pace as total exports. Chinese imports from the US are more diverse. Machinery & equipment accounted for about 20 % of the value of goods imports, vegetables (mainly soybeans) 15 %, minerals (about a quarter of which is crude oil) 15 %, chemicals 13 % and transport vehicles 9 %. Of these groups, only the on-year value of mineral product imports grew during the January-August period.

China’s goods trade surplus with the US has contracted over the past year, but is still substantial.

Sources: China Customs, Macrobond and BOFIT.