BOFIT Weekly Review 36/2023

China using many small measures to support the economy

With China’s economic growth slowing, most institutional forecasters now see GDP growth falling a bit below the official government target of 5 % this year. To combat cooling growth, Chinese officials have responded with a slew of support measures targeting specific sectors or regions. Most significantly, China seems to have resisted the use of its classic support measure – a massive stimulus programme based on fixed investment. Indeed, the idea of boosting fixed investment is scarcely mentioned, which is a welcome change as more investment-fuelled stimulus would only exacerbate China’s misallocation of capital and increase its already stratospheric debt levels. While it is difficult to assess the cumulative impact of many small actions, the general view is that the announced measures are insufficient to reverse the slowdown in economic growth. Consumer confidence continues to be weak, many branches suffer from overcapacity, export growth has stalled and local governments have limited stimulus options available.

China’s struggling real estate sector has been a central focus of current support efforts. Already last December, the government declared stabilisation of the real estate sector as a top priority for 2023. At end-August, the newly-created National Administration of Financial Regulation (NAFR) and the central bank announced a national minimum downpayment standard of 20 % of the purchase price for first-time apartment buyers and 30 % for buyers of a second apartment. Nevertheless, the required downpayment and most other real estate market regulations still get decided at the local level. After the announcement, several cities have rapidly decided on reductions in their downpayment percentages. An other important change is that China’s biggest cities (Beijing, Shanghai, Guangzhou and Shenzhen) have redefined who qualifies as a “first-time buyer”. First-time buyers in these metropolises now include persons who once owned an apartment in the city, but then ceased for some reason to have their own city abode. This is a large change as the required downpayment for first-time buyers is significantly lower than for second home buyers, and they get a small reduction in the interest rate charged on their apartment loan. The minimum interest rate for first-time apartment buyers is the benchmark 5-year Loan Prime Rate (LPR) minus 20 basis points. For buyers of a second apartment, the minimum rate has just been cut to LPR plus 20 basis points. Many of the real estate sector tax breaks set to expire this year have been extended until the end of 2025.

Local administrations, which typically take the lead in implementation of economic stimulus, now often find themselves struggling with huge debt burdens. To ease their financial distress, the central government has granted local governments the possibility of issuing bonds worth a total of 1 trillion yuan that they can then use to pay down high-interest off-budget “hidden debt”. Some reports suggest that the government has also arranged de facto zero-interest bank loans for troubled local governments by paying interest costs directly to lender banks.

The government is seeking to enlarge disposable household incomes by increasing income tax breaks. The 1,000 yuan-a-month tax deduction for daycare costs of children younger 3 years and school costs for older children has been raised to 2,000 yuan (previously 1,000 yuan). The monthly deduction for caring for an elderly parent has also been increased from 2,000 yuan to 3,000 yuan. The changes are retroactive to the beginning of 2023.

Another important signal is the government’s extension of the tax advantage for foreign workers to the end of 2027. The number of foreign workers in China has fallen sharply, and the previously planned ending of the tax break would have only compounded the problem. The government also decided this summer to extend tax breaks granted during Covid-19 pandemic to sole proprietors and SMEs, as well as suspend certain administrative payments to the end of 2027. In addition, the National Development and Reform Commission (NDRC) announced it is establishing a new office to oversee development of the private sector.

The government wants to revive financial markets using a variety of measures, including a 50 % reduction in the stamp duty on share trades. Firms have been encouraged to buy back their own shares, new rules limit IPOs and large institutional investors such as state funds and banks have been requested to increase their long-term equity holdings. The China Securities Regulatory Commission (CSRC) has announced that it is moving ahead with regulatory changes that will permit insurance funds and pension funds to increase the share of equity holdings in their portfolios. Officials are pondering increasing the time markets are open for trading.

CENTRAL BANK JUGGLES NEEDS TO LOWER FINANCING COSTS AND SLOW YUAN DEPRECIATION

The PBoC slightly lowered the rates at which it provides financing to banks and cut its 1-year LPR by 10 basis points in August (BOFIT Weekly 34/2023). It did not reduce the 5-year LPR, China’s main housing loan reference rate. Observers say the cuts were likely driven by eroding bank profitability. More recently, large commercial banks reportedly began to lower deposit interest rates starting this month. Bank margins will be increased by reducing the 1-year deposit rate by 10 basis points and 5-year deposit rate by 25 basis points. Deposit rates were cut a year ago and again in August. Housing loans in China are typically fixed-rate or adjusted once a year, so the recent rate cuts have yet to affect current housing loans. The central bank has now encouraged banks to renegotiate housing loan terms to help households reduce their interest costs. This move is also hoped to support the housing market.

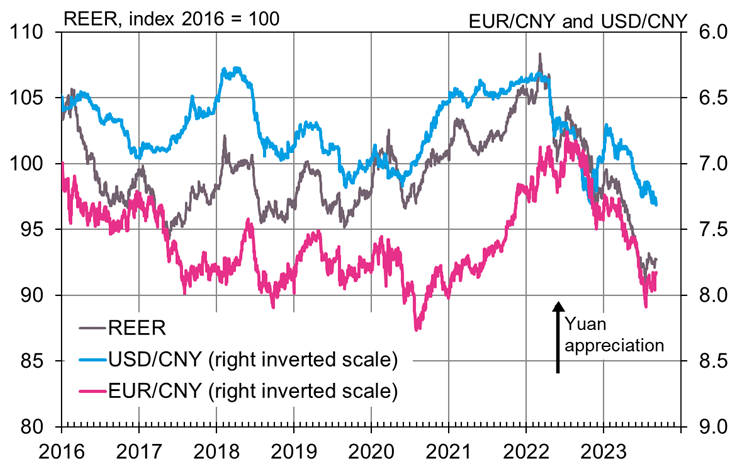

Due in part to dollar strength, the yuan-dollar exchange rate is currently at its lowest point since 2007. The PBoC has tried to slow the rate of yuan depreciation by setting its daily fixing rate above the market rate. The dollar-yuan rate is permitted to fluctuate within a band 2 % above or below the daily fixing on mainland China markets. To slow the weaking of the yuan, the PBoC in July raised its “macroprudential parameter” on cross-border financing. This affects the capacity of financial institutions and firms to borrow overseas. In an effort to support the yuan’s exchange rate, the PBoC announced at the beginning of September that it was reducing its foreign currency reserve requirement from 6 % to 4 % of forex deposits as of September 15 to increase slightly the amount of forex available to mainland China markets. Neither measure, however, is expected to have a significant impact on the exchange rate. According to media reports, the PBoC resorted to providing “guidance” to commercial banks to support the yuan and look into whether domestic firms are speculating on the currency’s further decline. State-owned banks are reportedly supporting also the offshore yuan (CNH) rate used outside mainland China. The central bank in August also issued more yuan-denominated bonds in Hong Kong than were maturing, thereby reducing the yuan liquidity in the offshore market. The measure is seen as an effort to support the CNH exchange rate.

The yuan has been losing value against the dollar for over a year

Sources: Macrobond, BIS and BOFIT.