BOFIT Weekly Review 15/2026

Russian GDP growth to remain at last year’s level boosted by higher commodity prices this year, growth will decelerate in 2027 and 2028

Russia’s economic outlook, the costs facing Russia’s wartime economy and the implications of ending the Ukraine war were discussed on March 30 at BOFIT’s annual Russia briefing.

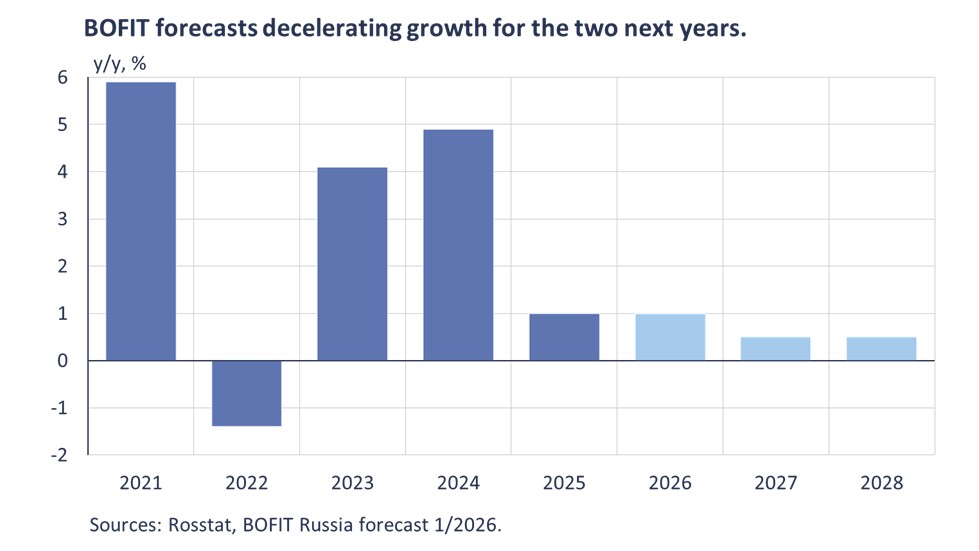

New BOFIT forecast sees Russian economy this year enjoying brief boost from higher commodity prices

The latest BOFIT Forecast for Russia sees GDP growth this year remaining close to last year’s 1-percent pace, with growth slowing to around ½ percent in 2027 and 2028. State stimulus measures applied in previous years yield diminishing returns as the labour force is nearly fully employed. Our forecast assumes that sanctions pressures will remain in place and world-market prices for crude oil will average that of mid-March oil futures during the 2026–2028 forecast period.

The slowdown in growth is explained largely by weak private demand and the slowdown in fixed investment growth. The rise in real wages will weaken, strangled by reduced household purchasing power caused by tax hikes and increases utilities tariffs. At the same time, companies are forced to grant wage hikes in excess of inflation in order to attract workers in a dwindling labour pool.

Throughout our 3-year forecast period, we see increasing bifurcation of the Russian economy into growing industries that serve the war effort and stagnating civilian industries. The ability of firms to invest, even those in the military-industrial complex, is limited, however, by weak profitability and ongoing tight monetary policy. Investment in human and physical capital needed for the war effort will continue, while other fixed investment falters. The activities of private firms not involved in the war effort are unlikely to see any expansion. Even as the rise in commodity prices caused by the Iran war grants the government slightly more room to manoeuvre in the public finance sphere, prolongation of the war of aggression will require Russia to further prioritise state spending. Russia’s consolidated budget overall, even with higher oil prices, is likely to remain in deficit. The impacts of high oil prices on Russian GDP and the country’s public finances are discussed in this recent BOFIT blog post.

The uncertainty associated with this forecast is exceptionally large and with both upside and downside risks to Russia’s economic development. The prices for crude oil in world markets, in particular, could significantly affect economic trends in either direction. Should oil prices remain elevated for a longer period, it would boost government finances and increase export earnings. If oil prices drop to levels prevailing before the Iran war, Russia’s fiscal strain would worsen. The weakening of private demand, the growing financing challenges in public finances and the continued pressure of sanctions pose significant negative risks to our baseline forecast.

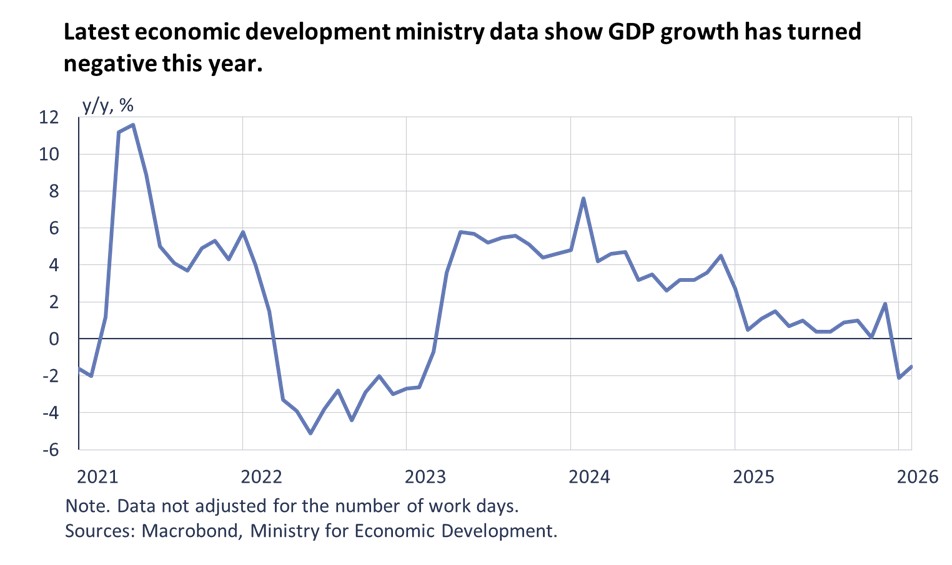

Preliminary data show Russian economy contracted in the first two months of this year

The preliminary GDP assessment from Russia’s economic development ministry shows that the Russian economy in February experienced negative 12-month growth for the second consecutive month. The last time such weak growth was seen was in early 2023. Industrial output stumbled in February, with manufacturing contracting by nearly 3 % y-o-y. While there was still positive growth in branches serving the military-industrial complex and pharmaceuticals, output in other industries contracted. The output of the mining & quarrying sector (includes oil & gas) rose by nearly 1 %.

On-year growth in real wages accelerated to 8.6 % in January, but consumer caution and increased value-added tax rates depressed growth in retail sales and consumer services at the start of the year. The brisk gains in real wages largely reflect Russia’s tight labour market and record-low 2 % unemployment rate.

US-Iran ceasefire brings momentary respite to energy markets

Prices soared in March for crude oil, natural gas, many petroleum products, and some fertilizers, due to the closure of the Strait of Hormuz. The ceasefire between Iran and the US announced on Wednesday (Apr. 8) raised hopes that the situation in the Strait of Hormuz would normalise, but the situation remains highly uncertain. Drone and missile strikes on regional oil & gas production facilities and Gulf ports could long cripple exports of energy products andfertiliser.

Similarly, estimates on the extent of damage to Russia’s ports on the Gulf of Finland are still quite vague. At the end of March, Ukraine hit Russia’s export harbours on the Gulf of Finland repeatedly, causing at least a temporary drop in Russian oil exports. In more normal times, over 2.6 million barrels of crude oil and petroleum products are loaded daily at the Primorsk (Koivisto) and Ust-Luga (Laukaansuu) harbours (about half of Russia’s oil exports shipped by sea). According to media reports, crude oil exports from the Primorsk and Ust-Luga harbours contracted in the final week of March to about a third of normal levels. Ukraine has also continued to hit Russia’s Black Sea oil ports.

Producers in the Middle East (Saudi Arabia, Iraq, Qatar, Kuwait, UEA, Bahrain and Iran) account for about 30 % of the approximately 100 million barrels a day of global oil production. Many of the large non-OPEC oil producers such as the US and Russia, refine and consume most of their production. Globally, crude oil exports are over 40 million barrels a day, while petroleum products amount to about 20 million barrels a day. Countries surrounding the Persian Gulf account for about 35 % of crude oil exports and about 25 % of petroleum product exports. Russia holds a roughly 10 % share in both cases.

Before the war, around 20 million barrels of crude oil and petroleum products passed daily through the Strait of Hormuz. The Strait of Hormuz is also the region’s sole shipping route for exports of liquefied natural gas (LNG). Qatar accounts for about a fifth of global LNG production. The war has brought sea traffic moving through the Strait almost to a complete halt and forced producers to cut back production. The situation caused oil and natural gas prices to soar in March.

Rising prices are good news for some commodity-producing states. Russia, in particular, has benefitted from rising market prices and a temporary easing of sanctions by the US. The average export price of crude oil, which is used in setting oil taxes in Russia, fell in the December-February period to below $45 a barrel. The March price then rose to an average of $77 a barrel. Despite everything, the price spread on a barrel of Russian export crude and benchmark Brent has remained around $30.