BOFIT Weekly Review 12/2026

In China, industry and foreign trade drove growth at the start of this year; direct impacts from Middle East war still modest

China’s industrial output in the first two months of this year rose by 6.3 % y-o-y, a slight increase from late 2025. Manufacturing output grew by 6.6 %, led by soaring growth in production of industrial robots, lithium batteries and 3D printers. Goods exports continued to enjoy buoyant growth in January-February: the value of exports in dollar terms was up 22 % y-o-y. Exports to the United States continued to slide (down 11 %), while exports to the European Union, ASEAN countries, Australia, South Korea, as well as exports to Taiwan, grew by nearly 30 %. Goods imports also rose by 20 % in dollar terms. While imports from the US declined by nearly 30 % y-o-y, imports were higher from the EU (up 12 %), Japan (26 %), Taiwan (19 %) and South Korea (35 %).

The timing of the Chinese New Year, which is set according to the traditional lunar calendar, varies annually between January and February. In addition, official holidays are often combined with weekends, which can also affect the length of the holiday period. This year’s Lunar New Year holiday week fell in mid-February and lasted nine days. The variation of the mercurial celebration time is inevitably reflected in the statistical data and makes comparison of January-February data from different years challenging. Nominal growth in retail sales was 2.8 % y-o-y in January-February 2026, a slight increase from last year. China's official purchasing manager index (PMI) for services held below the 50-point threshold indicating growth in January-February, while readings of the S&P Global index, which places more weight on private businesses, rose to 52 points in January and 57 points in February. Compared to pre-pandemic 2019, the number of domestic tourists during the 2026 New Year holiday was up by 15 % and tourism earnings by 12 %.

The downturn in China’s real estate sector is now in its fifth year. Official volume figures based on floorspace show that apartment sales in January-February declined 14 % from a year earlier, while new building starts decreased 23 % y-o-y over the same period. Construction investment fell by 11 %.

Inflation averaged 0.8 % in the first two months of this year, nearly unchanged from the pace of inflation in the final months of last year. Core inflation, which excludes volatile food and energy prices, rose by 1.3 %, up a tenth of a percent from the December figure. The decline in producer prices continued. Average producer prices in January-February were more than 1 % lower than in the same period last year. The decline was less pronounced than last year, however, when producer prices fell by nearly 3 % for the entire year. With the attacks of Israel and the US on Iran, oil prices have risen in recent weeks. A prolonged war would inevitably be reflected in Chinese inflation, even if the government can limit the rise of energy prices for end consumers.

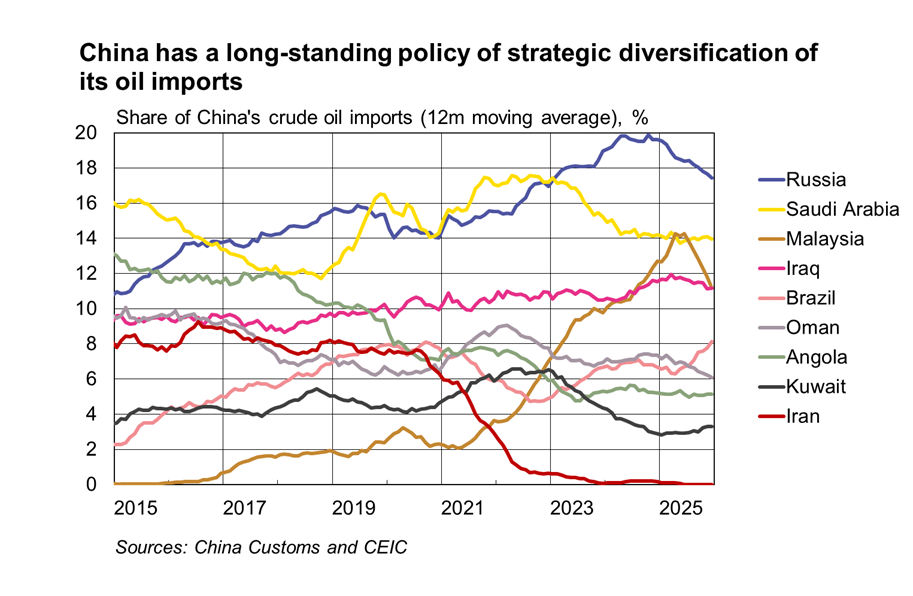

The Middle East is an important source of China’s oil imports: 40–50 % of crude oil imports come from the region, even though not all of it is shipped via the Strait of Hormuz. There is no precise data available for China’s purchases of Middle Eastern oil as China’s smaller refineries routinely purchase discounted Iranian oil from traders in e.g. Malaysia in order to circumvent sanctions. Even with incomplete official figures, sea traffic tracking data indicate China is by far the largest purchaser of Iranian oil. While China is the world’s largest oil importer, oil accounts for less than 20 % of the country’s primary energy consumption. Oil plays its least significant role in electrical power generation and its biggest roles in the petrochemical sector and transport (even with the push to electrify the economy). China also has its own buffers: domestic oil production is sufficient to cover well over a quarter of consumption, and China has some of the world’s largest strategic oil reserves (by some estimates, China’s strategic reserves are equivalent to over 100 days of imports). In response to the war, China last week halted fuel exports until at least the end of this month. Natural gas accounts for less than 10 % of China’s total energy consumption, and more than half of this is covered by domestic production. About 20 % of natural gas consumed in China is imported in the form of liquefied natural gas (LNG). China’s main LNG suppliers are Australia (over 34 %), Qatar (just under 30 %), Russia (10 %) and Malaysia (10 %). In other words, Qatari LNG only accounts for about 6 % of China’s total gas consumption.