BOFIT Weekly Review 11/2026

Growth in bank lending slowed last year in Russia

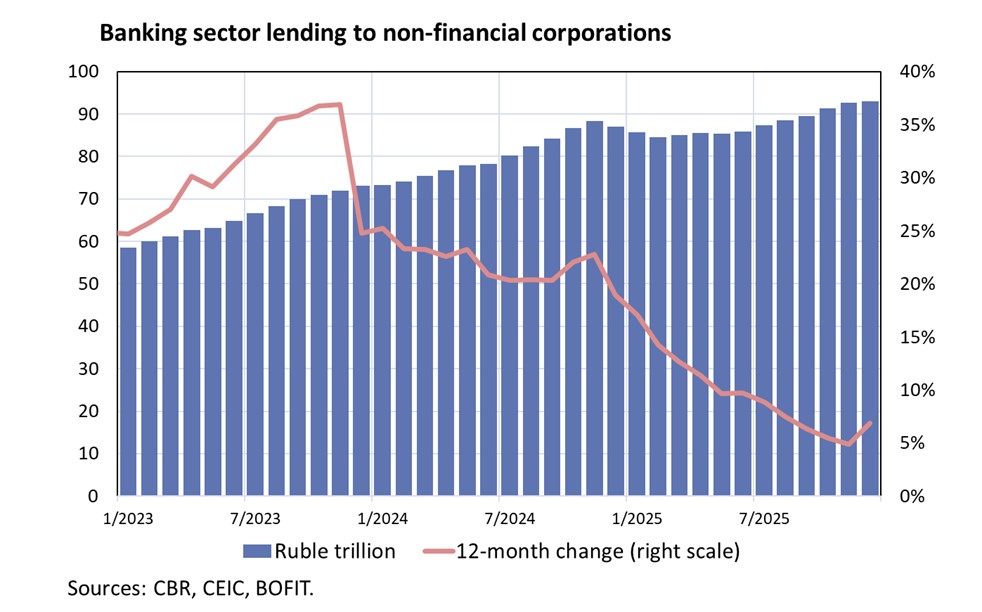

Russia’s financing system, which already relies heavily on banks, has seen the importance of domestic bank financing increase further due to Western sanctions. Additionally, a large share of government support is channelled to firms and households in the form of bank loans. Bank lending has grown rapidly since the summer of 2022, but the pace slowed markedly last year. In 2025, banks’ loan portfolios increased by 17 % compared with the previous year.

Companies took out fewer loans than last year

The total corporate loan stock amounted to 96.6 trillion rubles as of end-December 2025, an increase of 12 % y-o-y. Of that, 86 trillion rubles represented lending to non-financial corporations. The volume of new loans to non-financial firms last year declined slightly from the previous year. The slowdown in credit growth reflected both sustained high interest rates and an overall deterioration of Russia’s economic growth prospects. According to the Central Bank of Russia (CBR), credit growth in the second half of last year was largely driven by large state-owned enterprises seeking funding for their investment programmes.

Adjustable-rate loans constitute roughly 65 % of the stock of loans granted to companies. Most adjustable-rate loans are tied to the CBR’s key rate. Thus, the series of CBR cuts in the key rate since last summer have also lowered the interest rates on new corporate lending. The average rate in December for new short-term loans (under a year) was 18 %, while the average for loans over a year was 13.7 %. In the first half of 2025, the average interest rate on short-term loans was well above 20 %. Short-term loans constituted about 45 % of new corporate lending.

The rise in interest rates and other costs has eroded the financial buffers of firms, which is reflected in the rise in payment defaults. The volume of overdue corporate loans increased slightly last year, reaching 2.7 % of the total loan stock as of December 2025. Loan losses recorded by banks, however, remain modest. A large proportion of non-performing loans involve loans to the real estate, construction, and retail sectors.

The stock of problem loans last year increased from 10 % to 11 % of the corporate loan stock, amounting to 10.4 trillion rubles as of end-December. Loan loss provisions of the banking sector covered 54 % of these problem loans, which can be considered a reasonable level. The true number of non-performing loans may be higher than reported as authorities have temporarily relaxed certain practices such as how restructured loans are recorded.

Housing loan market dependent on government subsidies

The total stock of bank loans to households rose by 6 % to 38.67 trillion rubles at the end of December. Around 60 % of household loans are mortgages, which continued to grow last year. Mortgage lending increased by 9 % y-o-y, although fewer new housing loans were issued than in 2024.

The overwhelming share of Russia’s housing loan market relies on government interest subsidy programmes. As of December, only about 20 % of new housing loans were based on prevailing market interest rates. Due to government subsidy programmes, housing loans growth during 2022-2024 was particularly rapid, bringing banks many first-time borrowers. The slowing growth in household incomes last year was also reflected in rise payment delinquencies and defaults. The share of non-performing housing loans rose last year from 1 % to 1.7 %. Although average household indebtedness remains modest, a stagnation in wage growth could significantly increase the risk of loan losses. Higher interest rates and tighter lending conditions caused the stock of consumer loans to decline last year. The consumer loan stock stood at 12.7 trillion rubles at the end of December, a decline of about 5 % y-o-y.

Market-based funding plays only a limited role

Banks’ funding relies heavily on deposits. Specifically, high deposit interest rates and rising real incomes last year continued to support growth in household deposits. Household deposits grew by 16 % last year (28 % in 2024) to 67 trillion rubles as of end-December 2025. Household investment in domestic securities last year also increased quite rapidly.

Growth in corporate deposits slowed significantly in 2025. Corporate deposits in banks only grew by 8 % y-o-y, reflecting declining corporate profits and lower export earnings. The share of foreign-currency-denominated deposits continued to shrink, falling to 16 % of corporate deposits as of end-December. The stock of household deposits at the end of December surpassed corporate deposits, which amounted to 63 trillion rubles. Overall, the banking sector’s total deposit stock is currently larger than the total loan stock.

Banks show generally good levels of capital adequacy

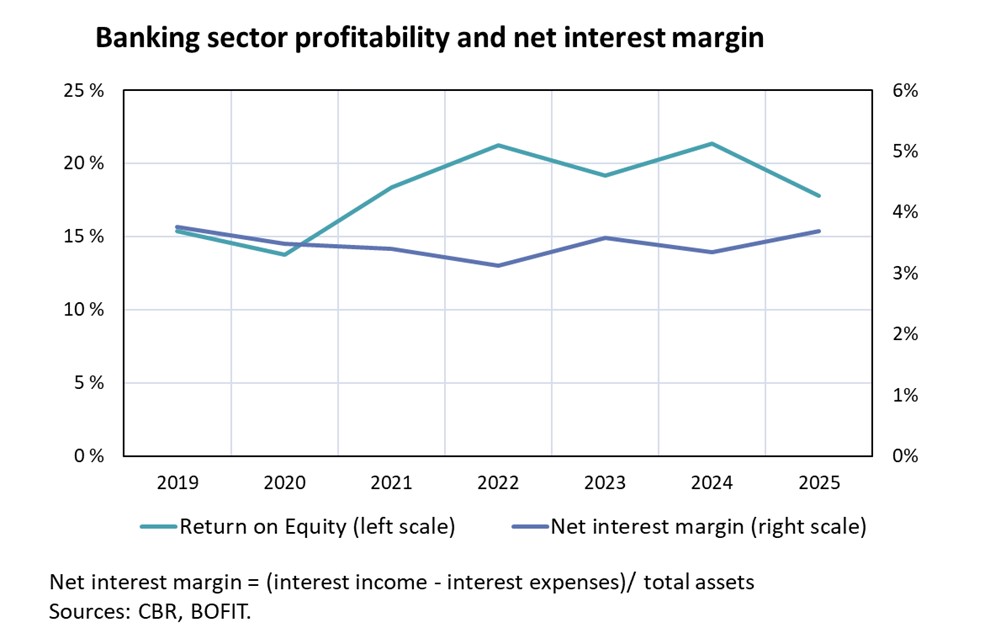

Banking sector profitability generally remained at a decent level last year. The sector’s combined 2025 profits amounted to around 3.5 trillion rubles (3.8 trillion rubles in 2024), while return on equity (ROE) was 18 %. Banks paid out dividends totalling 1.6 trillion rubles, over a third of which went directly to government coffers. The 2025 net profit of Sber, one of Russia’s largest banks, was 1.7 trillion rubles.

Bank equity rose by roughly 10 %, which was slightly faster than growth in bank total assets. The average bank capital adequacy ratio (N1) increased from 12.9 % to 13.4 %. The capital adequacy ratios of large, systemically important, banks were slightly lower. As of end-December, the capital adequacy ratios were below 11.5 % for five Russia’s major banks.

Credit risks are increasing

Although the banking sector is quite well capitalised on average and loan-loss provisions are at tolerable levels, bank-level differences can be large. Of particular concern to regulators is the banking sector’s focus on lending to heavily indebted large enterprises. According to CBR financial stability reports, lending to Russia’s seven largest borrowers accounted for over 10 % of the entire corporate loan stock. Financial statements from 2024 already revealed that the interest payments of many large firms exceeded their financial year earnings before interest, taxes, depreciation and amortisation (EBITDA). Most of the bank loans of Russia’s biggest corporations are likely carried on the balance sheets of the country’s largest banks.

Rising costs and weakening demand may depress corporate earnings and lead to significant impairment losses for some banks. Some problematic loans will likely be restructured to avoid more severe difficulties. Increased credit losses would weaken the ability of banks to grant new credit, although the likelihood of an abrupt crisis remains very small. The banking sector’s foreign exchange risk has decreased, as both financial institutions’ and corporates’ foreign-currency liabilities have shrunk substantially due to sanctions.