BOFIT Weekly Review 7/2026

Russian economy lost steam in 2025

Russia’s economic growth slowed sharply in 2025 with on-year GDP growth of only 1 %. Growth faded last year despite a rapid increase in government spending and widening government deficit. Labour shortages and strained capacity utilisation limited the possibilities for further increases in output and increased inflationary pressures. Inflationary pressures were restrained through severe monetary policy. Even if the Central Bank of Russia (CBR) started last summer to gradually cut its key rate it was still high at 16 % in end-December. Although inflation slowed towards the end of last year, consumer prices on average were still up 9 % for all of 2025.

Broad-based slowdown

Preliminary Rosstat figures show Russian GDP grew by 1 % in 2025. The slowdown in domestic demand growth was broad-based. Household consumption grew by about 3 %. Growth was slightly slower than in pre-pandemic years (2017–2019). Growth in public sector consumption also slowed. Most of the increase in public sector spending last year apparently went to fixed investment. Investment growth overall slowed sharply last year to around 2 %, implying weak private sector fixed investment.

Russia no longer releases national accounts data on volumes of foreign trade. It did report, however, that the value of goods and services exports contracted by 14 % last year and the value of goods and services imports declined by 9 %. Much of the drop in the value of exports reflects reduced oil prices. The International Energy Agency (IEA) estimates that the average export price of Russian crude oil last year was around $56 a barrel, a decrease of 18 % from 2024. The IEA also said the volume of oil exports declined by about 2 %. According to Russian Customs, the drop in imports was led by declines in the “machinery, equipment and transport vehicles” category. The increase in recycling fees for imported cars provoked a sharp decline in car imports to Russia last year.

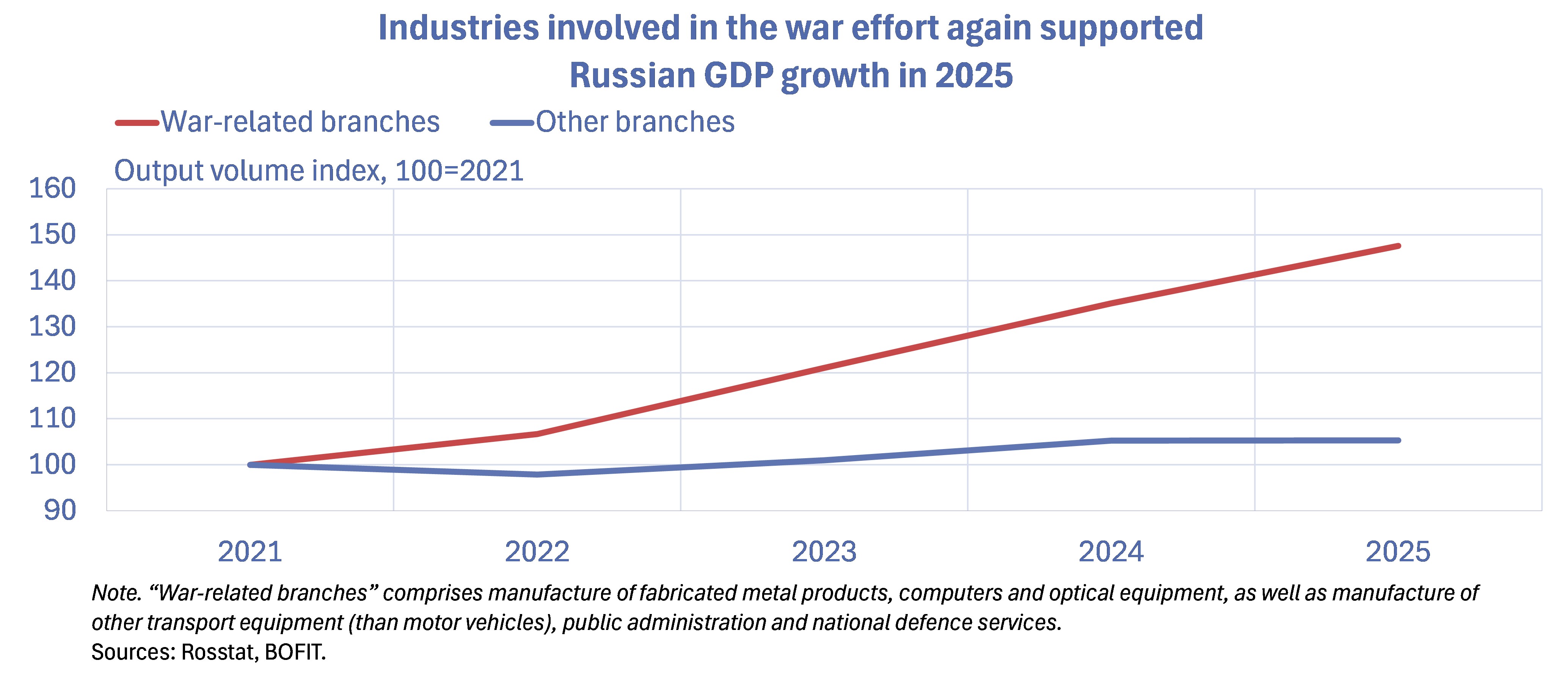

Output data in the national accounts show that GDP growth last year was again driven by industries linked to the war effort. While other industries combined stagnated last year, there were huge differences across core sectors. Growth in retail sales and construction remained positive, but slowed significantly from previous years. Agricultural output also increased by 2 % last year. On the other hand, production declined in many industries. Output in the extractive sector (includes oil & gas) fell for the third consecutive year, with output down by 2 % y-o-y in 2025. Numerous manufacturing categories showed output declines, including automotive, machine-building and manufacturing of electrical equipment. Services saw declines in such categories as car trade and wholesale trade, as well as services related to water transport and warehousing.

Transient factors largely accounted for the end-year growth spurt

Preliminary figures suggest that the Russian economy picked up slightly late last year following a weak autumn. Although third-quarter GDP growth was a mere 0.6 % y-o-y, preliminary fourth-quarter data indicate that GDP rose by about 1 %. Detailed 4Q GDP figures have yet to be published. According to preliminary figures from Russia’s economic development ministry, GDP grew by nearly 2 % y-o-y in December.

Monthly data highlight the growth contribution from retail sales in December. As in October and November, retail sales volume again rose at 4 % y-o-y. The 4Q retail revival largely reflected transient factors: the increase in the auto recycling fee at the start of December, and the general increase in value-added tax (VAT) rates at the start of this year. Wages continued to rise at the end of last year and unemployment remained low. Construction activity, which returned to positive growth in the final months of last year, rose by 5 % y-o-y in December. The recovery in housing construction helped lift growth in the construction sector.

Industrial output growth, boosted by manufacturing, also picked up in December. In contrast, trends in the extractive sector faltered, with production falling by 3 % y-o-y. Production of natural gas and coal fell by 4 % y-o-y in December. For all of 2025, natural gas production was down by 3 %, while the coal production remained at the same level as in 2024. Although Russia no longer publishes information about oil production, deputy prime minister Alexander Novak said that oil production contracted by about 1 % last year. This estimate is similar to the IEA estimate.

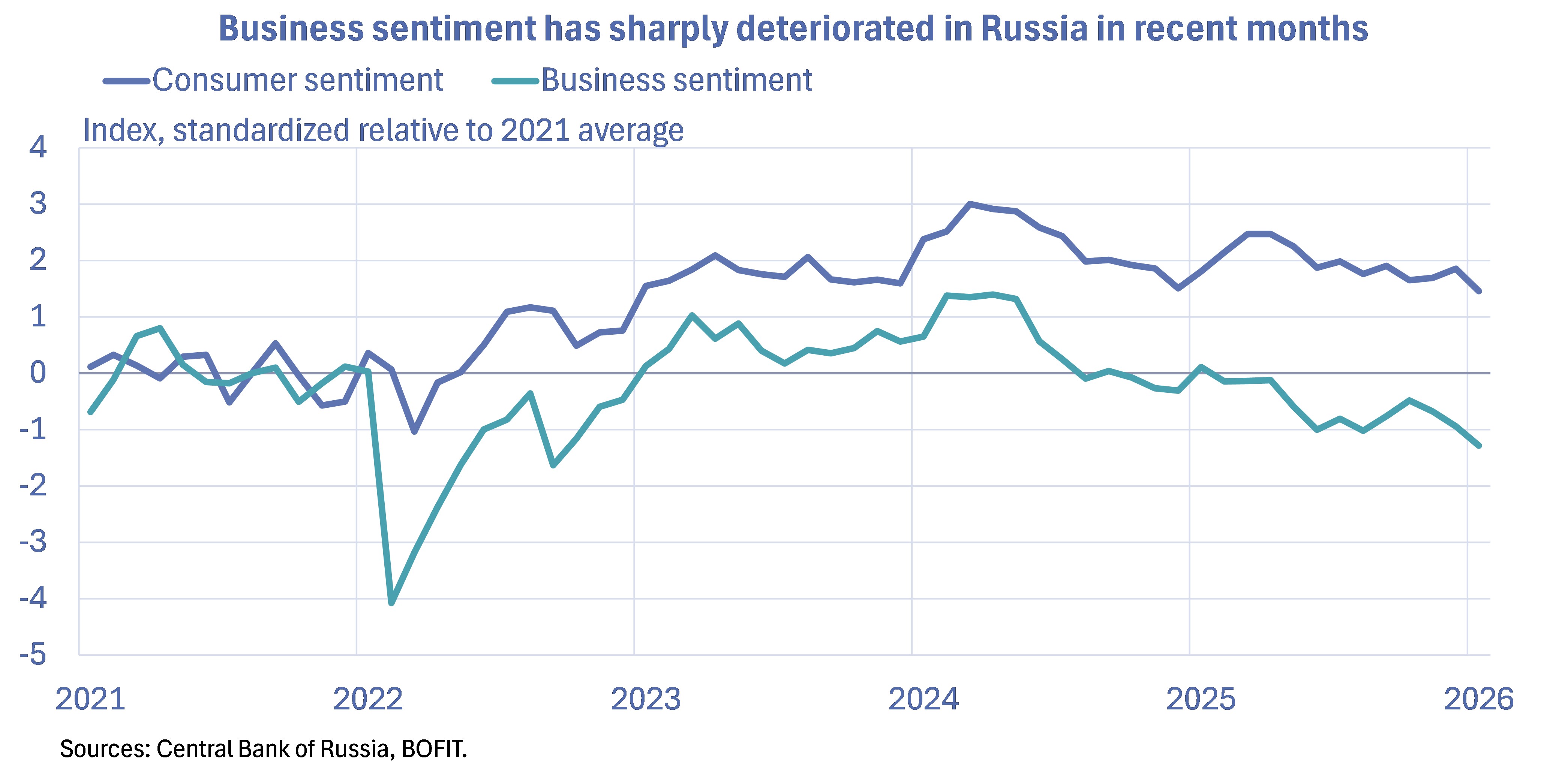

Forward-looking indicators predict fading economic growth in the months ahead. Confidence of both consumers and businesses has eroded, with businesses especially concerned about the degraded business environment. The January index reading from the CBR’s survey of business sentiment was its lowest since 2022.

The most recent forecasts anticipate modest Russian GDP growth this year. The January update of the International Monetary Fund (IMF) outlook predicts Russian GDP will grow by 0.8 % this year and 1 % in 2027. Consensus Economics, which compiles and averages estimates of private sector international forecasters, said in its January report that the average expectation for Russian GDP growth was 0.8 % this year and 1.3 % in 2027. These forecasters see a more than 70 % likelihood that Russia GDP growth this year will fall within the range of 0.2–1.1 %. The latest CBR forecast sees Russian GDP growing by 0.5–1.5 % this year and 1.5–2.5 % next year. The CBR releases its latest forecast today (Feb. 13) in conjunction with its scheduled monetary policy meeting.

Loose fiscal policy and tight monetary policy prevailed in 2025

Although government spending growth remained high last year, revenue growth was depressed by reduced oil & gas earnings. The government deficit was the largest during the full-on invasion of Ukraine four years ago.

Preliminary finance ministry figures show that Russia’s federal budget revenues grew by 2 % last year, surpassing 37 trillion rubles. Oil & gas revenues fell by 24 % last year, while other revenues rose by 13 %. Federal budget spending increased by 7 % to 43 trillion rubles. Federal spending growth was front-loaded, and at the end of the year spending turned to decline compared to the previous year. The federal budget deficit was 5.6 trillion rubles, or 2.6 % of GDP.

Consolidated budget data figures, which provide an overall picture of government finances, have yet to be released. The federal budget accounts for about half of total government revenues and expenditures. Consolidated budget spending grew by 18 % y-o-y in the first 11 months of 2025. This year’s budget framework foresees a 4 % increase in consolidated budget spending.

In contrast to generous fiscal policy, Russia’s monetary stance remained tight all last year with the CBR’s key rate averaging 19 %, a slightly higher average rate than in 2024. The CBR, however, began to lower its key rate gradually in the second half of the year, eventually bringing it down to its current level of 16 %.

Russia’s galloping inflation rate was gradually tamed last year through the application of tight monetary policies. Consumer prices rose 9 % on average in 2025. By December, the pace of 12-month inflation had slowed to below 6 %. Inflationary pressures continue this year, however, e.g. due to the increase in VAT rate. Business inflation expectations, in particular, have risen substantially. The most recent international and Russian forecasts see annual inflation slowing gradually to around 5 % by December of this year.

The CBR will announce next interest rate decision today afternoon. Going into the meeting, most Russian analysts expected the CBR to keep the rate unchanged, but a 50-basis-point reduction was also considered possible. The CBR, which has signalled it is pursuing a cautious line with respect to rate cuts, stated in its most recent forecast that it expects the key rate to average 13–15 % this year.