BOFIT Weekly Review 51/2025

Russia’s GDP growth modest and government deficit on the rise

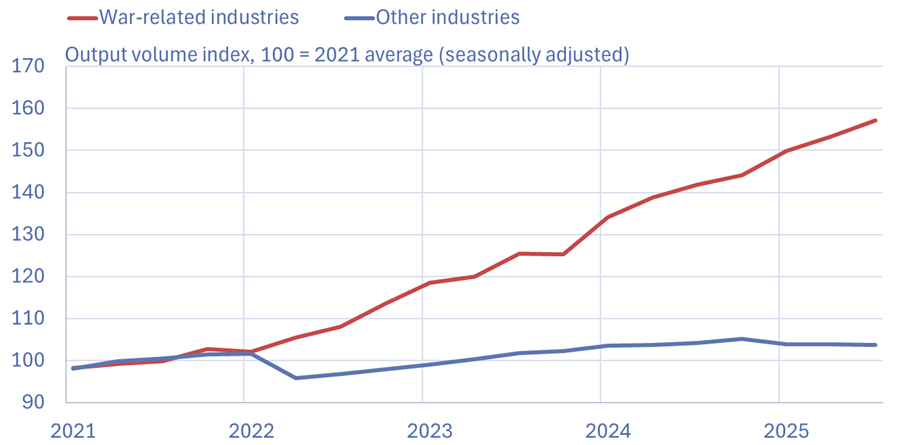

Rosstat figures show that Russian GDP grew by 1 % y-o-y in the first nine months of this year. Preliminary figures from Russia’s economic development ministry suggest that economic growth remained at around 1 % also in January-October. Russian production now follows two distinct paths: industries linked to the war effort have continued to experience rapid output growth in recent months, while other industries have either stagnated or contracted.

The government has sought to sustain output growth also this year by increasing spending, particularly boosting war-related production. Preliminary data show the federal budget spending increased by 13 % y-o-y in January-November. While the pace of spending growth has moderated in recent months, remaining within the government’s spending plans would require a sharp on-year contraction in December spending. This seems unlikely, however, and December spending will probably again exceed plans causing the budget deficit to increase more than expected. After the approved adjustment in November, this year’s federal budget deficit is expected to come in at around 5.7 trillion rubles or 2.6 % of GDP.

Unlike in previous years, this year’s increases in government spending have not translated into higher output, but instead aggravated economic imbalances. Many branches currently suffer from labour shortages and production capacity has been stretched to the limit. Wages and prices of production inputs have risen rapidly. Despite slowing inflation, consumer prices in Russia were still up 7 % y-o-y in November. To keep inflationary pressures at bay, the CBR has been restrained in its recent key-rate-cutting. Markets anticipate that today’s monetary policy meeting will result in another slight reduction in the key rate, which is currently at 16.5%.

The latest forecasts also put Russian GDP growth next year at around 1 %. However, there are many risks associated with economic development as long as Russia continues its war in Ukraine. Several forecasters predict Russian inflation of 5–6 % next year. The budget framework approved in November calls for a nominal increase in government spending next year of roughly 4 %, implying zero growth in real spending. As in previous years, however, the budget framework is likely to be adjusted next year. Among other things, Russian government finances remain vulnerable to shocks from oil prices and changes in oil production volumes (see BOFIT blog in Finnish).

Russian GDP growth continues to follow dual paths, with industries involved in the war effort growing faster than non-military branches

Note: The estimated trends of industries linked to the war effort incorporates three manufacturing branches serving the military, as well as defence-related services.

Sources: CEIC, Rosstat, BOFIT.