BOFIT Weekly Review 45/2025

Russian economic growth remains sluggish and subject to structural imbalances

The Russian economy has continued to grow slowly in recent months, with the overall economic picture remaining unchanged in September. Even with slowing growth, structural economic imbalances have so far shown little signs of easing. The labour market situation remains tight and inflationary pressures are increasing. Recent sanctions packages imposed on Russia by the West have degraded conditions in the Russian economy.

Low output growth persisted in September

Russia’s composite index based on output from five core sectors of the economy (industry, agriculture, construction, transportation and retail trade) rose by 0.8 % y-o-y in September. Growth was slightly higher than in previous months, but there were no signs of broader economic recovery. The index rose by 0.9 % y-o-y in January-September. The preliminary estimate from Russia’s economic development ministry suggests that Russian GDP also grew by 0.9 % y-o-y in September. In the first nine months of this year, economic output growth was up 1 % y-o-y according to this indicator.

After spiking in August, growth in retail sales volume slowed in September to 2 % y-o-y . Consumption continued to be supported by rising wages (average monthly wages were up by 4 % y-o-y in real terms in August) and the strong employment situation. Russia’s unemployment rate has long remained at historically low levels of around 2 %.

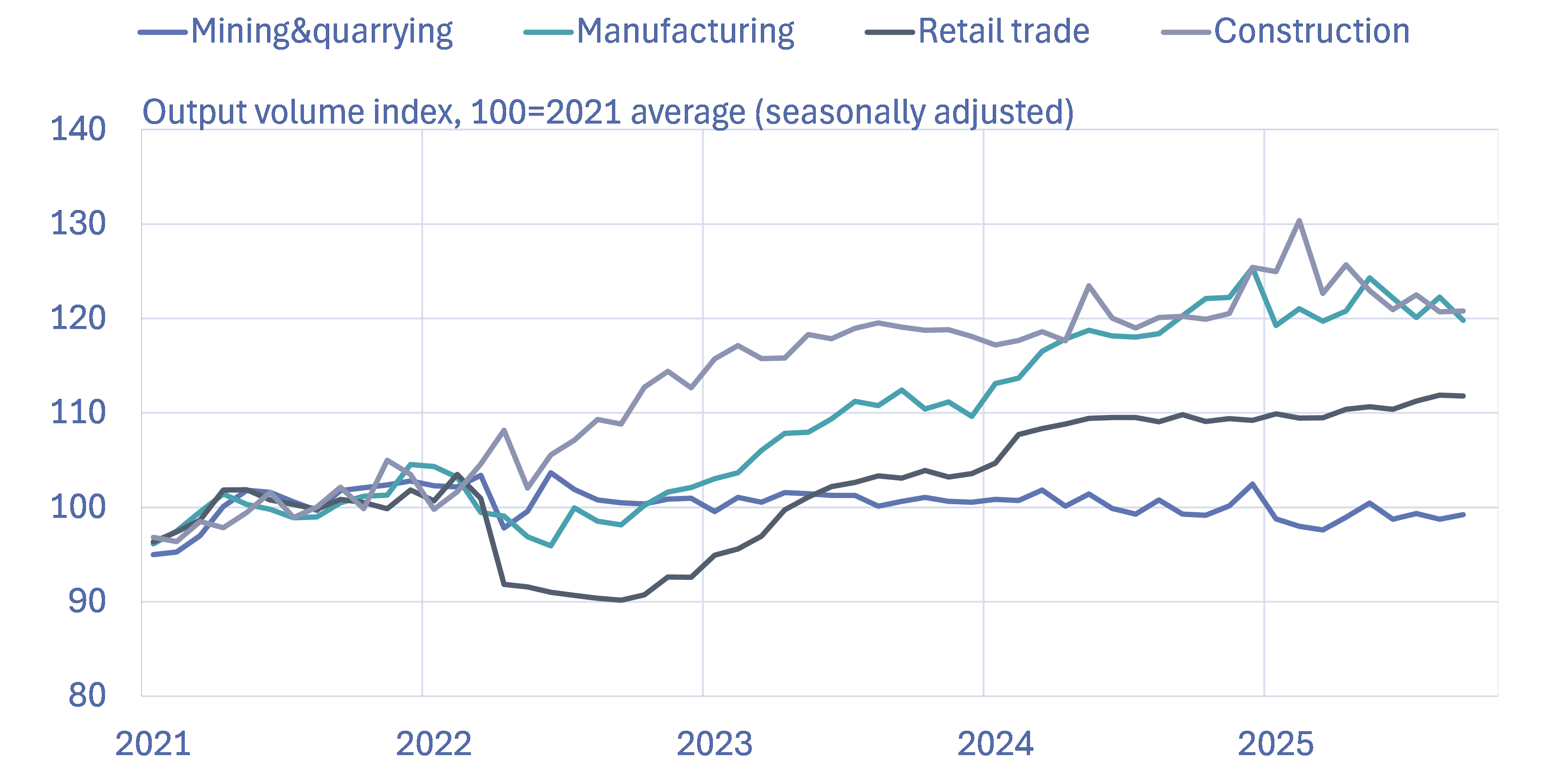

The decline in the mining & quarrying sector came to a halt in September, but for January-September as a whole, production was down by 2 %. Growth in manufacturing this year has only occurred in branches linked to the war effort and in the pharmaceuticals industry. Nearly all other manufacturing industries experienced negative on-year growth in January-September. Construction activity overall was stagnating in September. Housing construction in particular has developed weakly in recent months, declining by 12 % y-o-y in the third quarter.

Production volumes have been nearly flat in recent months in core sectors of the Russian economy

Sources: Rosstat, CEIC, BOFIT.

CBR concerned about rising inflation pressures

At its regular interest rate meeting in October, the board of the Central Bank of Russia decided to again lower the key rate, this time by 50 basis points. The key rate presently stands at 16.5 %. The CBR expects inflation to keep declining gradually, but more moderately than it had previously anticipated. The central bank noted that the key rate needs to average 13–15 % next year to achieve the 4 % inflation target by December 2026. Consumer prices rose by 8 % y-o-y in September.

CBR governor Elvira Nabiullina recently defended the need for a tight monetary stance before a Duma hearing. Reminding Duma representatives of the experiences of the 1990s, she warned that lowering the key rate too quickly could ignite a hyperinflationary spiral. Even if inflation is down this year, the seasonally adjusted annualized rate of inflation (SAAR), which describes the latest price trends, accelerated in September. The inflation expectations of firms have risen and household inflation expectations remain high. Although the pickup in inflation largely reflects transient factors (increased food and fuel prices, as well as one-off hike in educational services), they nevertheless can feed through to inflation expectations. Inflation will also be boosted at the start of next year when one-time increases in VAT rates and administratively set rates for municipal services go into effect.

According to Nabiullina, state-backed loans account for about a fifth of growth in Russia’s bank lending since 2020. She noted that higher amount of subsidised credit requires higher policy rates to keep inflation in check. Credit growth has generally accelerated in recent months, and the CBR now expects the loan stock to grow by 8–11 % this year. Nabiullina called for government support to be reallocated from bank lending to companies to encouraging firms to raise more of their financing from the bond and stock markets.

Nabiullina said she sees no evidence that the Russian economy is slipping into recession. Despite slowing growth, the labour market remains strong. Real wages continue to rise and unemployment has remained at record lows. Although the situation has deteriorated in individual companies, the central bank assesses that e.g. companies that have moved to a four-day working week schedule only employ 0.2 % of employed persons. The lion’s share of firms continues to suffer from labour shortages.

Latest round of sanctions hits Russia’s stock market

The stock market capitalisation of the Moscow Exchange collapsed in February 2022 following the market panic caused by the full-on invasion of Ukraine, sanctions, foreign investors exiting the country and the general increase in uncertainty. Even if valuation levels have partly recovered since, they are still far below pre-war levels. The main MOEX index now stands at a level roughly 30 % below that of January 2022. Both the Moscow Exchange and the Central Securities Depository have been on the US sanctions list since June 2024. As connections to international markets are extremely limited, stock exchange trading is mainly conducted among Russian parties.

After recovering a bit at the start of the year, the MOEX has sunk steadily in recent months. At the end of October, the index was down by 12 % y-o-y. Share prices have been depressed by declining domestic demand and ever-tightening Western sanctions. For example, following the US sanctions announcement on October 23, the price of Lukoil shares fell by 14 % in a week. The volume of Lukoil share trades nearly tripled which suggests that small investors, in particular, dumped their holdings.

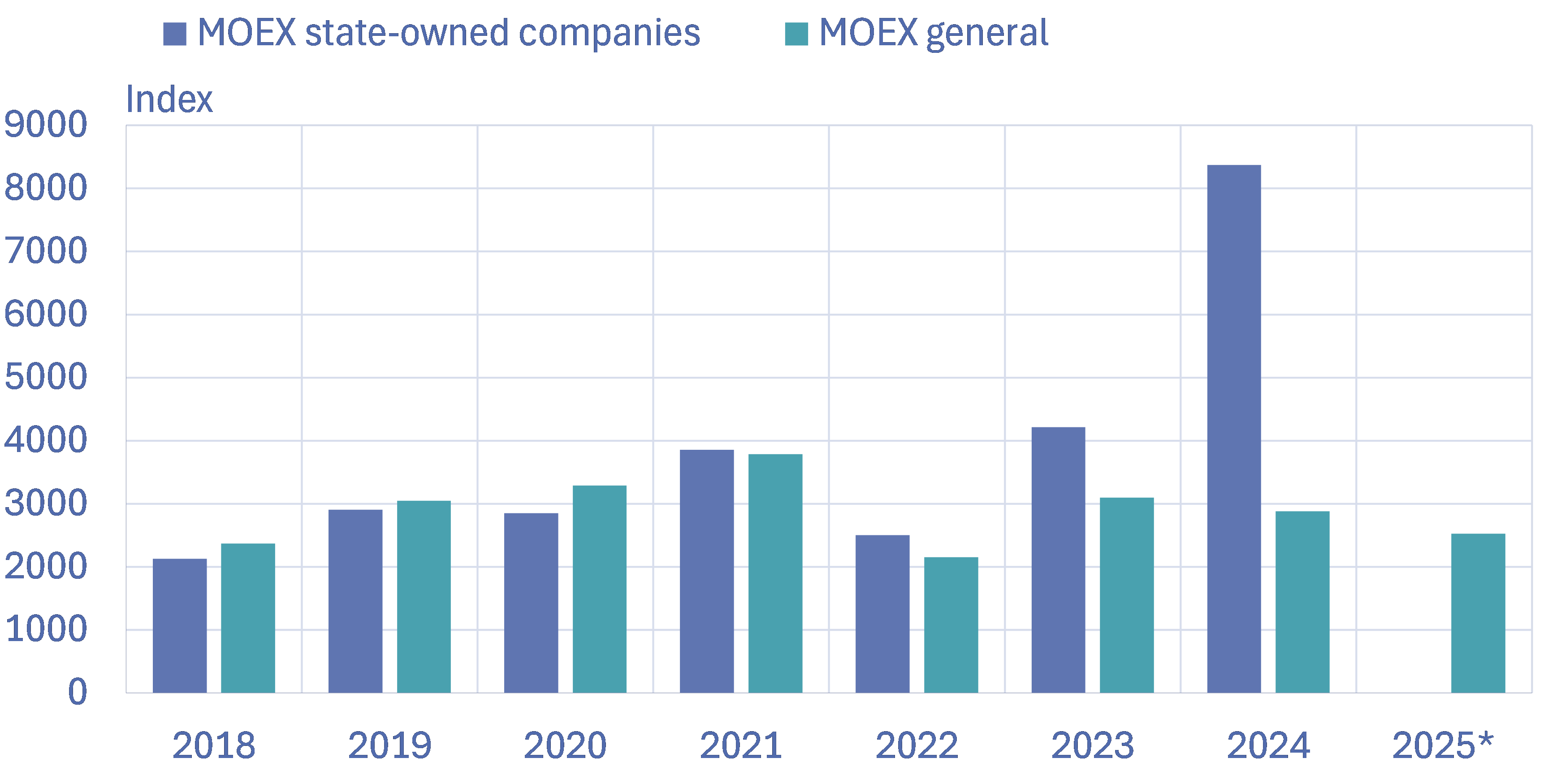

Large state-owned enterprises (SOEs) have been the winner in this bear market. SOEs have the dual advantage of close relations with the country’s leadership and indirect support from the state to prop up their share prices. Since the invasion of Ukraine, the trend for share prices of state-owned enterprises has diverged sharply from the general share index. In 2024, to ruble-based MOEX general index fell by 7 %, even as the State-Owned Companies Index (SCI) rose by 99 %. In the future, share prices could also be supported by recent finance ministry guidance encouraging state-owned companies to invest their liquid assets in shares or bonds of Russian companies.

The State-Owned Companies index (SCI) has outperformed the the Moscow Exchange’s general index (MOEX) in past years

* 2025 refers to end-October. MOEX releases its State-Owned Companies Index (SCI) once a year. The weighting of the index is not published, and figures for this year have not yet been released.

Sources: MOEX, BOFIT.

New sanctions packages overshadow prime minister Mishustin’s visit to China

Russian prime minister Mikhail Mishustin visited China this week for a regular high-level meeting and met also with president Xi Jinping. A number of cooperation protocols and roadmaps were signed, and the two countries declared that economic cooperation would become even closer. Many factors, however, now complicate economic relations.

Mirror statistics show that Russian goods imports from China amounted to $74 billion in January-September, down 11 % y-o-y. The decline in imports is mainly due to vehicle imports, which have halved this year. Other imports grew overall by 2 % y-o-y. Imports have also decreased in many other product groups besides vehicles (e.g. electrical equipment). Imports have been reduced especially by Russian recycling fees that have substantially increased prices of imported cars. Demand in Russia is also generally weaker due to slowing growth. Western sanctions also complicate Russia’s trade with China particularly due to problems related to payments.

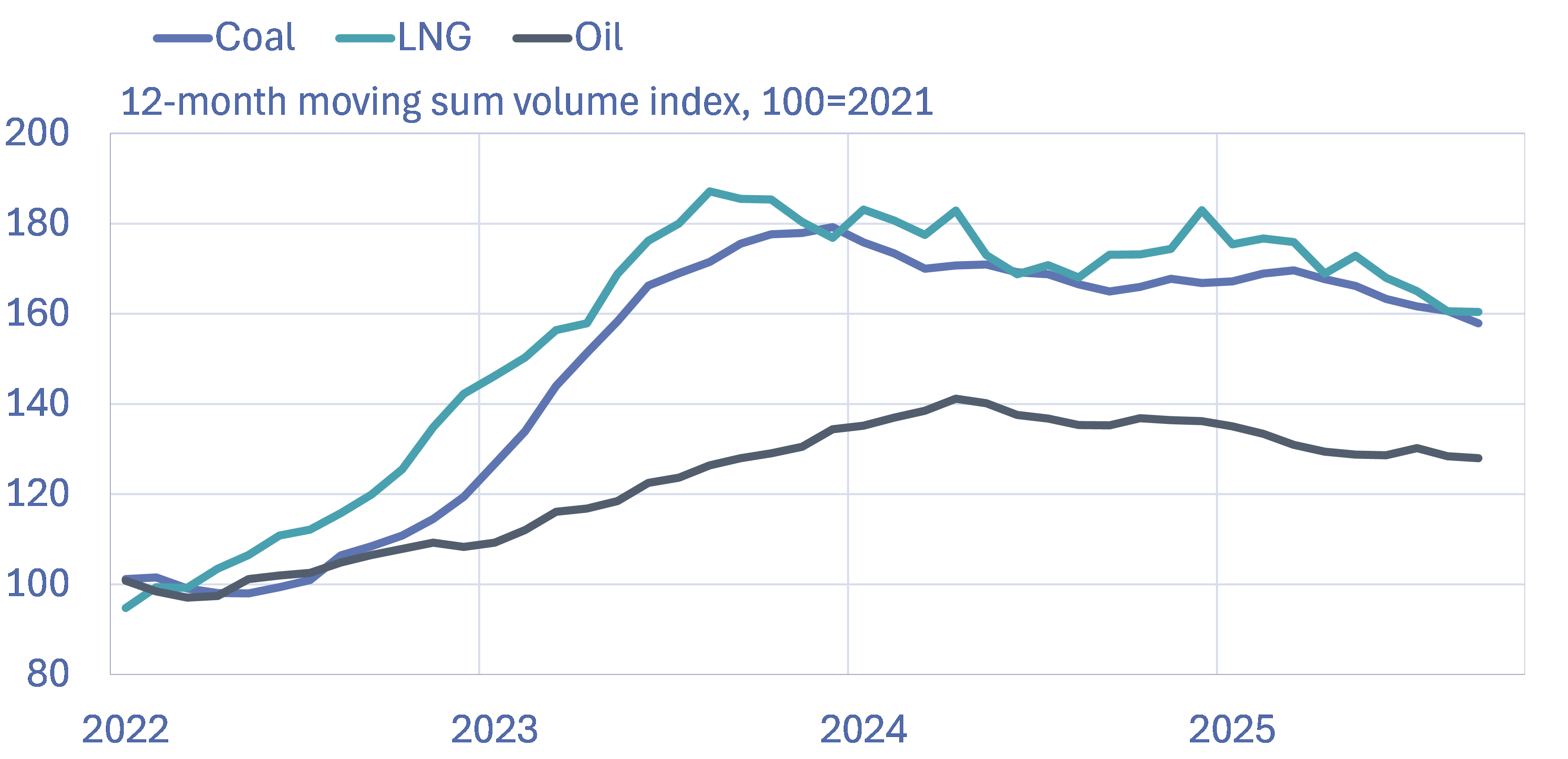

Mirror statistics further show that Russian goods exports to China amounted to $89 billion in January-September, a 7 % y-o-y decrease. Some of the decline in export values is due to falling commodity prices, but the export volumes of many key goods have also declined. In January-September, the volume of China’s coal imports from Russia contracted by 7 % y-o-y, crude oil by 8 % and liquefied natural gas (LNG) by 17 %.

The latest round of US sanctions on Rosneft and Lukoil, Russia’s largest oil producers, can further restrain Russia’s oil exports. According to media reports, many Chinese and Indian oil refiners have paused their imports of Russian oil. Data collected by Bloomberg also suggest that the volume of Russian crude oil exports has decreased over the past two weeks.

The volume of China’s imports of many energy products from Russia has turned to decline

Sources: CEIC, China Customs, BOFIT.