BOFIT Weekly Review 43/2025

Russian economic growth expected to slow sharply; new sanctions increase risks

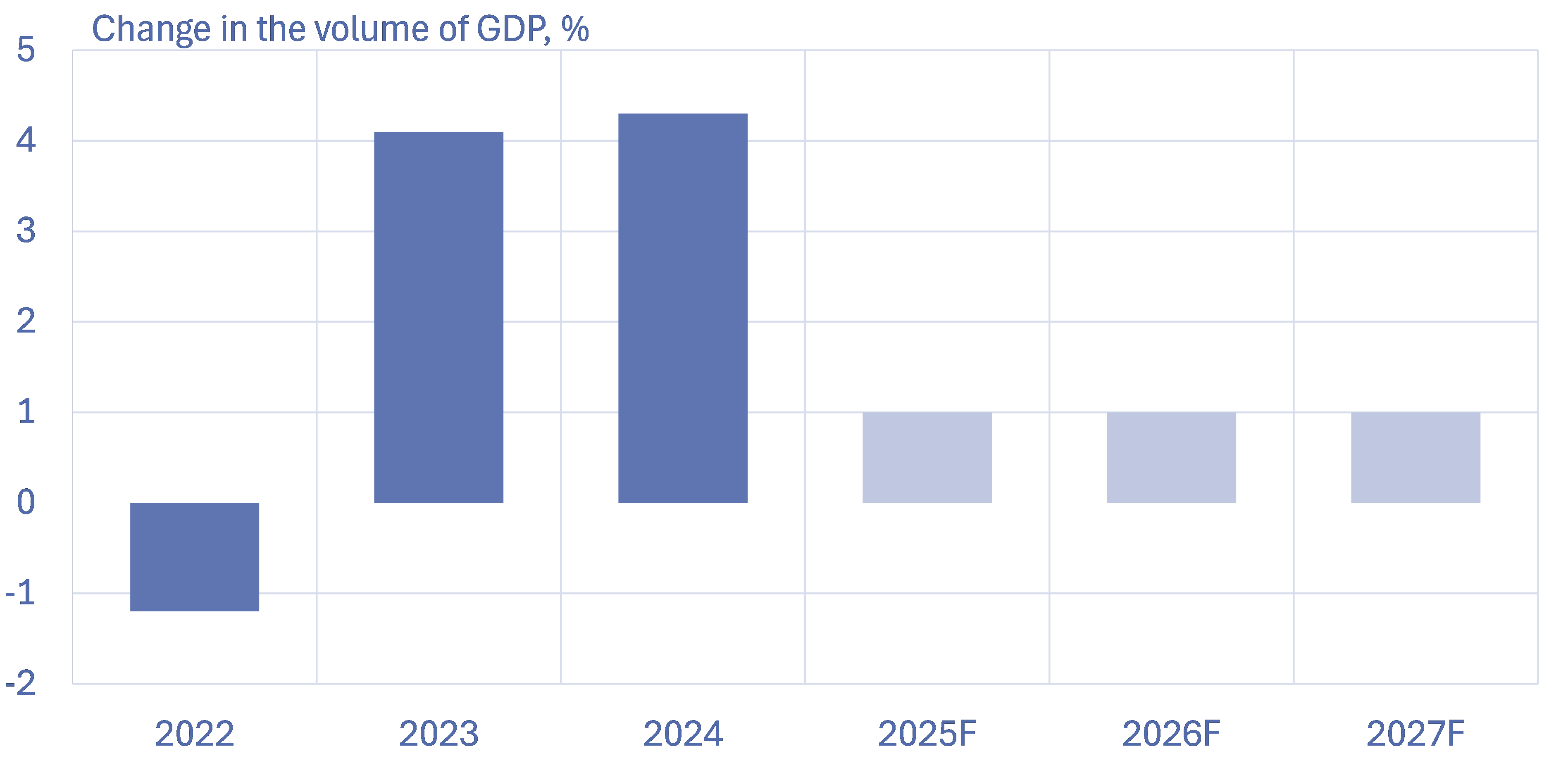

Our latest BOFIT Forecast for Russia 2025–2027, released on Monday (Oct. 20), expects Russia’s economy to grow by 1 % at most this year. Barring significant policy shifts or a large external shock, we see Russian GDP growing annually at around 1 % also in 2026 and 2027. While a full-blown economic crisis is currently not in sight, Russian economy faces significant risks as long as Russia continues its war in Ukraine.

Economic imbalances dampen Russia’s growth potential

Public spending continues to support domestic demand, and production in industries directly linked to the war effort in particular. Russia already utilises nearly all of its available production capacity, however, so further increases in public spending to boost growth can only yield limited returns. Because higher public spending drives up price levels overall, the Central Bank of Russia has been forced to fight inflationary pressure by raising its benchmark key rate to historically high levels.

While monetary policy is unlikely to have much impact on operating conditions within state-subsidised sectors – especially those involved with the war – high interest rates are already causing a slowdown in private consumption and private investment. High costs, labour shortages and tax increases limit the growth possibilities of private firms not serving the military-industrial complex. This leads to a substantial slowdown of wage growth and narrowing of corporate investment opportunities. The significant cuts last year to government subsidy programmes for housing loans, along with high interest rates, have stopped growth in household borrowing.

The downside risks to the expected economic development increase as economic imbalances become more severe. The use of tax hikes and cuts to other than war-related spending as a means of balancing public finances could drive the economy into recession. But continuing high growth in government spending also risks economic crisis. Russia’s dependence on earnings from sales of oil & gas and dependence on China create another set of risks to the Russian economy. A significant tightening of Western sanctions could also reduce Russian growth below forecast.

A prolonged pause in military operations combined with a loosening of sanctions could provide the Russian economy with a much-needed respite. Nevertheless, in the absence of significant political change, Russia’s military build-up, the redistribution of domestic assets, and the designation of Western actors as unfriendly would likely remain unchanged.

BOFIT’s latest forecast expects low growth for Russia in coming years

Sources: Rosstat (realised), BOFIT Forecast for Russia (Oct. 2025).

New sanctions packages increase pressure on the Russian economy

The United States and the United Kingdom have added state-controlled Rosneft, Russia’s largest oil company, as well as privately-held Lukoil, to their sanctions lists. The US and UK sanctions lists now include Russia’s four largest oil producers, which combined account for 70-80 % of Russian oil production and exports.

The EU also approved its 19th sanctions package on Thursday (Oct. 23). EU also tightened sanctions on Rosneft and another major Russian oil company, Gazpromneft, which is already on the US sanctions list. The latest sanctions package completely bans the import of liquefied natural gas (LNG) from Russia from the start of 2027. In addition, another 117 shadow fleet vessels were added to the EU sanctions list. Shadow tankers transporting Russian oil are used to circumvent sanctions (for more on the Russia’s shadow tanker fleet, see this BOFIT blog post from August). The EU’s sanctions list now includes nearly 560 vessels in Russia’s shadow tanker fleet. Additional Russian citizens and entities are now subject to sanctions, as well as certain banks and firms operating outside Russia (e.g. in China and the UAE).

The new sanctions can potentially have a substantial effect particularly on Russian exports. Global oil prices rose immediately on market expectations that sanctions could reduce Russian oil supply. The price effect is likely moderated with abundant supply perspectives from other producers. New sanctions can potentially also lead to a significant reduction in Russia’s budget revenues from oil & gas. They have accounted for roughly a quarter of Russia’s federal budget revenues this year. This could cause additional pressures for Russia’s public finances, as this year’s consolidated budget is already set to reach a record deficit (more on Russia’s budget framework in a recent BOFIT blog post).