BOFIT Weekly Review 39/2025

Russia struggles to balance fiscal and monetary policy demands

Russian economic policymakers continue their quest to balance between the loose fiscal policy requirements needed to continue the war in Ukraine and the tight monetary stance required for curbing economic imbalances. Government spending and government-subsidised lending have increased dramatically in recent years. The preliminary 2026–2028 budget framework sees the federal budget remaining in deficit throughout next three years, even with increased government revenues from tax hikes. In recent months, the Central Bank of Russia (CBR) has gradually lowered its historically high key rate as inflationary pressures have subsided in response to slowing demand growth. The slowdown in growth, however, has raised concerns of the economy falling into recession, along with calls for a quicker transition to looser monetary policy.

The new forecast from Russia’s ministry of economic development sees the country’s GDP rising by 1 % this year and 1.3 % next year. Growth is hoped to revive a bit in coming years. The ministry estimates that continued moderate growth will be maintained mainly by private consumption supported by rising wages and strong employment. Fixed investment, on the other hand, is expected to contract slightly next year. The average export price of Russian oil is forecast to be $59 a barrel next year, rising to $65 a barrel in 2028. The discount relative to the price of benchmark Brent crude is expected to shrink slightly compared to this year. The ruble’s exchange rate is predicted to weaken gradually over the next few years.

CBR cuts key rate again

At its regular policy meeting this month, the central bank board decided to further reduce the key rate by 100 basis points to 17 %. While the market expected a rate cut, many were hoping for a more substantial decline of the key rate. The CBR based its decision on rate cut on signs that both inflation and demand in the Russian economy were cooling, but it also noted several factors for restraint, including recent acceleration in lending growth and prevailing high inflation expectations. The CBR also noted the inflationary risks from further ruble weakening and uncertainty over budget plans.

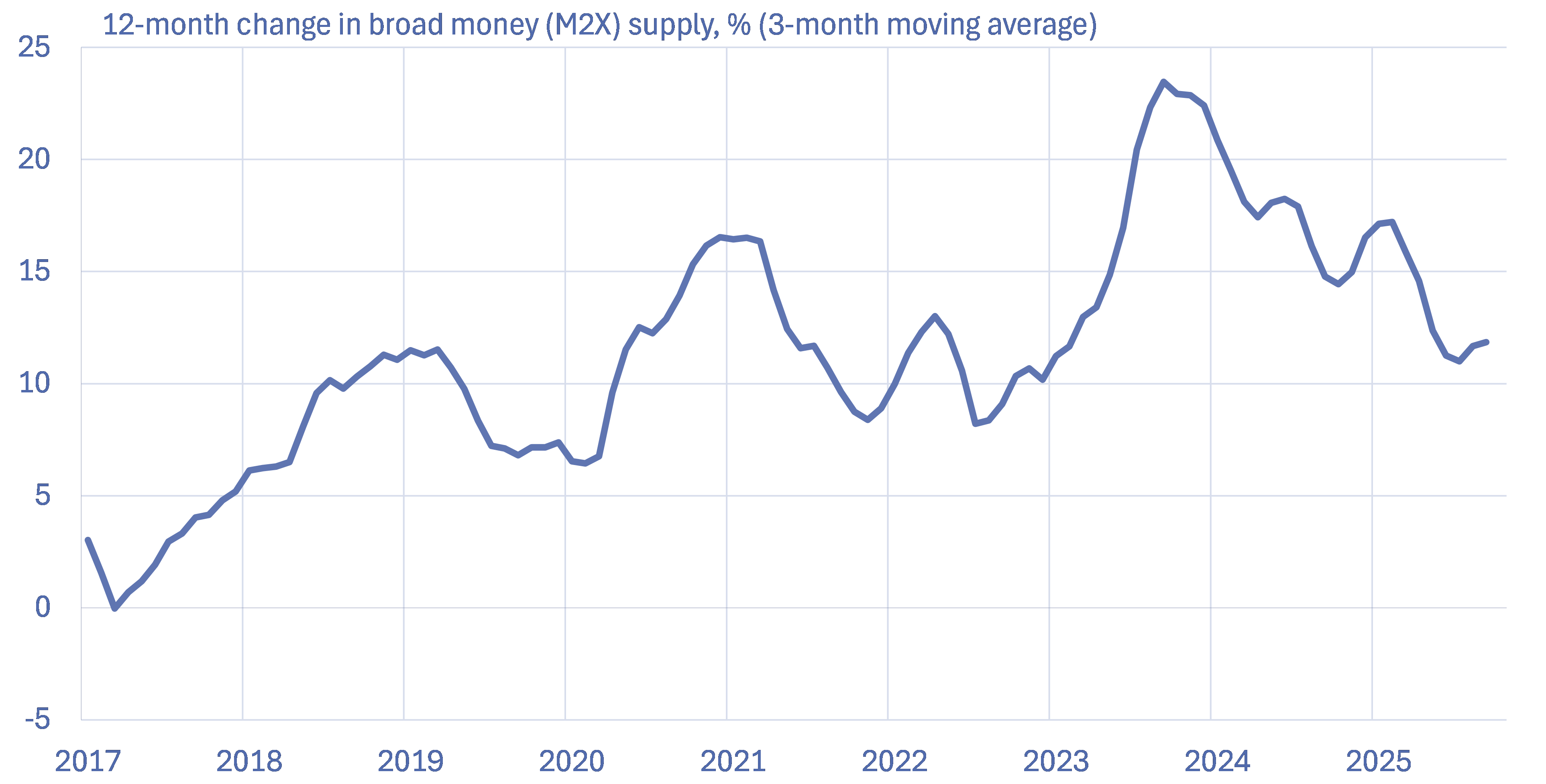

Rapid credit growth in recent years has also been reflected in an exceptionally strong increase in Russia’s money supply. Despite a slowing in recent months, money supply is still growing rapidly. Changes in the inflation rate typically lag changes in money supply growth by several months, implying that increased inflationary pressure could continue for a while.

Growth of Russia’s money supply has remained brisk in recent months

Sources: Central Bank of Russia, Macrobond.

Consumer prices rose by 8 % y-o-y in August. Food prices were up by 10 % y-o-y, while non-food goods climbed by 7 %. Prices for services rose by 11 % y-o-y, driven in part by hikes in administratively-set rates for municipal services such as water, heat and electricity.

Gasoline prices have become a popular topic in Russia in recent months. Gasoline prices have risen, and in several regions of the country gas stations are encountering supply troubles due to record-high wholesale prices. Officials have already begun to implement measures to assure fuel availability and restrain price gouging. Restrictions have been placed on exchange trading of refined petroleum products and the ban on gasoline exports has been extended. A temporary ban on the export of diesel fuel is also under discussion. Production of petroleum products has been hobbled by recent Ukrainian drone strikes on Russian oil refineries.

Federal budget set to remain in the red

The finance ministry this week presented to the government its proposed amendments to this year’s budget and the budget framework for the upcoming 3-year period. The proposal should be sent next week to the lower-house Duma for approval. While details on the amendments to this year’s budget plans are still sketchy, a finance ministry press release indicated that further spending increases were coming this year. Finance minister Anton Siluanov already announced earlier that the government plans to borrow more this year than previously planned. According to media reports, the federal budget deficit this year should increase to 2.6 % of GDP.

Under the revised budget plan adopted in June, federal budget spending should rise this year by 5 %. For the first eight months of this year, spending was already up by 21 % y-o-y. In addition, revenues have increased more slowly than expected, further ballooning the federal budget deficit. While the original federal budget plan called for a deficit of 1.2 trillion rubles, the deficit accumulated in the first eight months of this year already exceeded 4.2 trillion rubles (2 % of GDP).

The latest three-year budget framework sees federal budget spending increasing by 4 % a year in 2026 and 2027, and then rising to 7 % in 2028. The budget’s projected spending growth for next year could also be reduced if this year’s budget estimate is exceeded. Revenues are also expected to rise, but the federal budget will nevertheless remain in the red for the entire 3-year period. The 2026 deficit is expected to be about 3.5 trillion rubles (1.6 % of GDP). The projection sees the deficit over the following years contracting slightly. No detailed breakdowns of spending and revenues are yet available.

In any case, defence spending appears to further increase next year, as the finance ministry has proposed an increase in value-added tax (VAT) rates next year in order to cover defence spending. The general VAT rate would be raised from its current 20 % to 22 % at the start of next year. The VAT increase, however, will exclude “socially important” goods such as food and medicine, which will continue to be subject to a 10 % VAT rate. To bolster government revenues, the finance ministry has also suggested such measures as increasing taxes on gambling companies.

Under Russia’s latest budget plan, the federal budget would continue to run deficits over the next three years

|

RUB trillion |

2024 |

2025B |

2026P |

2027P |

2028P |

|

Revenues |

36.7 |

38.5 |

40.3 |

42.9 |

45.9 |

|

Expenditures |

40.2 |

42.3 |

44.1 |

46 |

49.4 |

|

Deficit |

-3.5 |

-3.8 |

-3.8 |

-3.1 |

-3.5 |

|

Deficit (% of GDP) |

-1.7 |

-1.7 |

-1.6 |

-1.2 |

-1.3 |

Note: B) Figures reflects approval of amendments to the 2025 budget act on June 24, 2025. P) Figures for 2026–2028 based on the finance ministry’s preliminary budget framework submitted to the government on September 24, 2025.

Sources: Russian Ministry of Finance, BOFIT.

Ruble depreciation could add to inflationary pressures

The ruble has lost value against other currencies in recent months, with the ruble-dollar rate this week hovering around 84 rubles to the dollar, a 6 % drop since end-June. The weakening apparently reflects the cuts in the key rate and shifts in foreign trade. Exports have weakened, while imports recently appear to have started to rise again. In August, the government also abandoned its requirement that large exporting firms convert their repatriated forex export earnings into rubles. In any case, the ruble’s exchange rate is still considerably stronger than it was at the start of this year.

Setting of the Russian currency’s official value has changed somewhat in recent years. The ruble is no longer a freely convertible currency as Russia has imposed various capital controls. Due to western sanctions, trade in western currencies in particular has been moved from the Moscow Exchange to the OTC market, where price formation is less transparent (BOFIT Weekly 35/2024). Because a handful of corporations play a major role in Russia’s forex market, a significant action by any one of these companies can swing exchange rates.

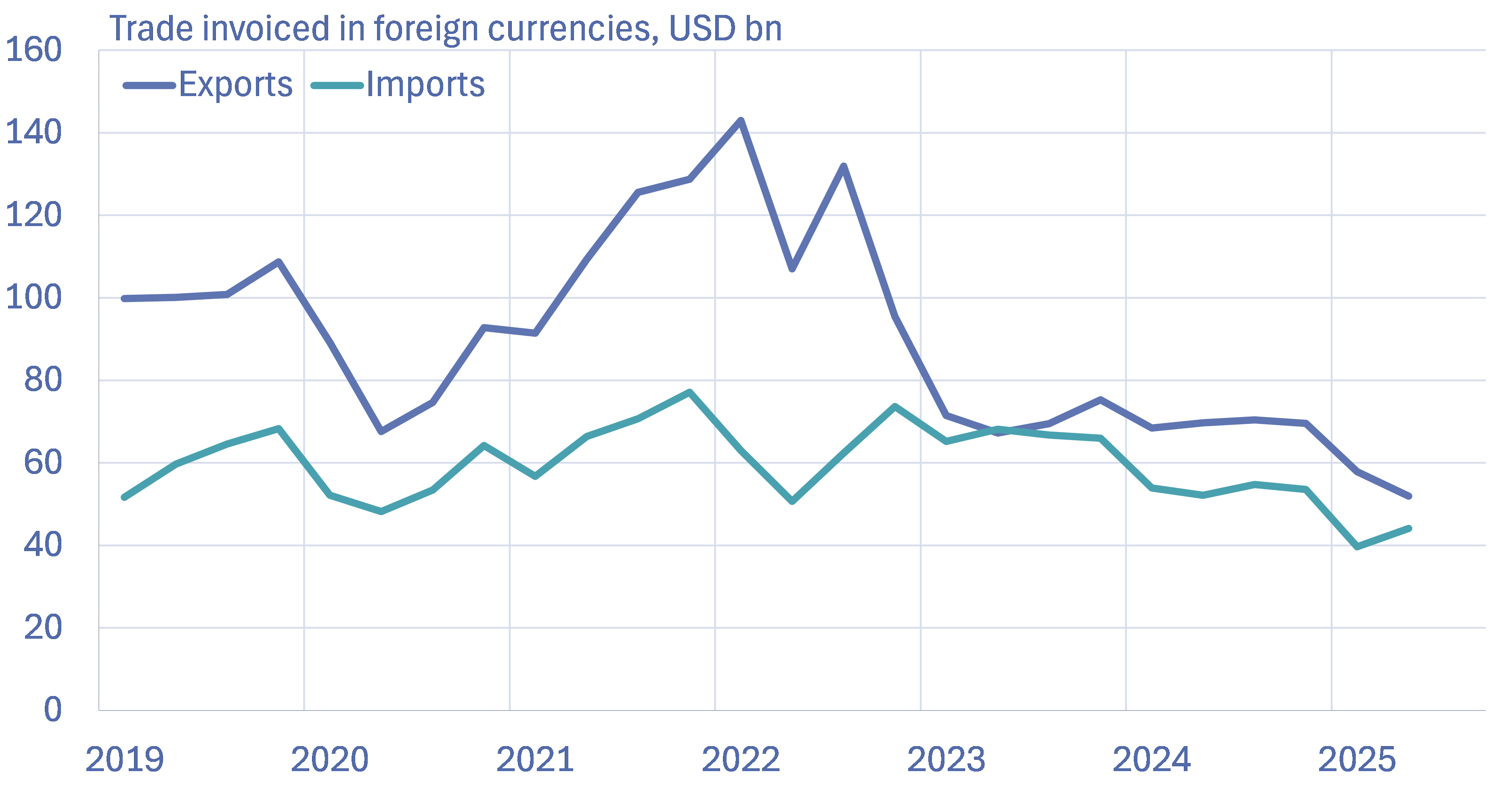

The importance of foreign currency exchange rates in the economy has also diminished. Exchange rate trends are important mainly in foreign trade. Due to sanctions, however, the contribution of foreign trade to Russia’s economic activity has shrunk. In 2021, exports corresponded to 30 % of GDP and imports 21 %. In 2024, their respective shares were just 22 % and 18 %. In addition, the share of foreign currencies in trade invoicing has declined sharply in recent years. Over half of Russian foreign trade is now conducted in rubles. The increasing shift to rubles in export revenues could make it harder for Russia to pay for imports because a large share of imports is still invoiced in foreign currencies. The balance of Russia’s trade invoiced in foreign currencies has recently narrowed sharply.

The ruble’s exchange rate also influences government budget revenues. The production tax on oil, for example, is based on the dollar-price of oil. When the ruble’s exchange rate is strong, government budget revenues, which are calculated in rubles, decline. This complicates funding of government spending, which is denominated in rubles. Oil & gas revenues have still constituted about 25 % of federal budget revenues this year.

Russia’s surplus in trade invoiced in foreign currencies has shrunk in recent months

Sources: Central Bank of Russia, BOFIT.