BOFIT Weekly Review 37/2025

Russian economic growth continued to slow in July

Russian output growth remained slow in July. The drag from tight monetary policy on demand is becoming more apparent, especially in the slowing of growth in fixed investment and investment-led branches. Inflation has also slowed gradually in recent months. Russian economy is expected to continue modest growth in coming months, but economic development is vulnerable to many risks. Government spending continues to increase, while government support measures appear to become more narrowly tailored and firms are expected to shoulder an even larger burden of war costs.

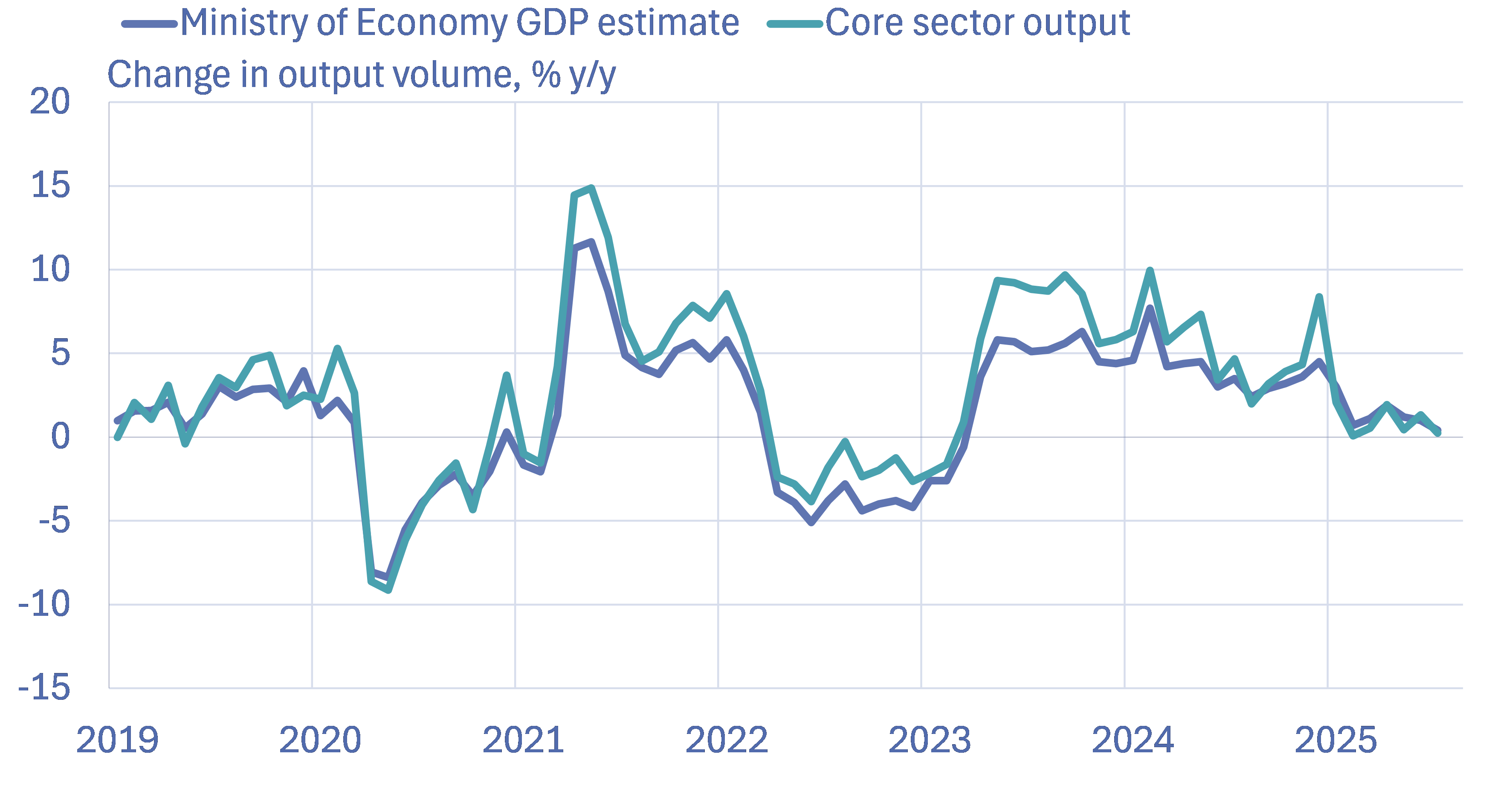

Output growth has flatlined

July figures suggest output growth slowed further. The composite index based on five core sectors of the economy rose by a mere 0.2 % y-o-y. Russia’s economic development ministry estimates that overall GDP growth in July was a mere 0.4 %.

Output appears to have been largely supported by consumption-driven branches. The volume of retail sales and service-sector sales still increased by 2 % y-o-y in July. Unemployment remained at historically low levels and wages continued to rise quite briskly.

Industrial output has nearly stagnated this year. While the trend for extractive industries stabilised in July, development in the manufacturing sector weakened and production declined sharply in certain manufacturing branches. For example, metal industry output contracted by 10 % y-o-y, machine-building by 12 % and the car industry by 26 %. For industries closely linked to the war effort, output continued to enjoy strong growth, as e.g. production of transport vehicles other than automobiles was up by nearly 50 % y-o-y in July.

Construction growth showed a modest pickup in July, rising by 3 % y-o-y. Total output in the construction sector grew even with the ongoing sharp decline in housing construction, which fell by 14 % y-o-y in July.

Agricultural output contracted slightly in July. This year’s crop-harvesting operations have been shackled by problems such as the tight labour supply and fuel shortages in many Russian regions.

Russian economic output growth slowed further in July

Sources: Russian Ministry of Economic Development, Rosstat, CEIC, BOFIT.

Investment growth fades

Growth in fixed capital investment has seen a dramatic slowdown in recent months, falling to just 1.5 % y-o-y in the second quarter (still nearly 9% in the first quarter of this year). Despite slowing investment overall, investment in production of transport vehicles other than automobiles doubled in the first six months of this year.

The slowing in investment growth reflects a bleak demand outlook and difficulties in finding financing. The share of investment financed directly from budget funds has fallen this year, and currently stands at 12 %. Companies financed a larger share of their investments either out of pocket or with bank loans. Such funding opportunities have also become more scarce this year.

Rosstat figures show that the overall profitability of Russian firms as measured in rubles decreased by 9 % y-o-y in the January-June period. Roughly 30 % of all firms showed losses, and the share of non-profitable firms in nearly all branches increased. The coal industry as a whole, i.e. coal companies in aggregate, showed even losses, with two-thirds of all coal companies operating in the red.

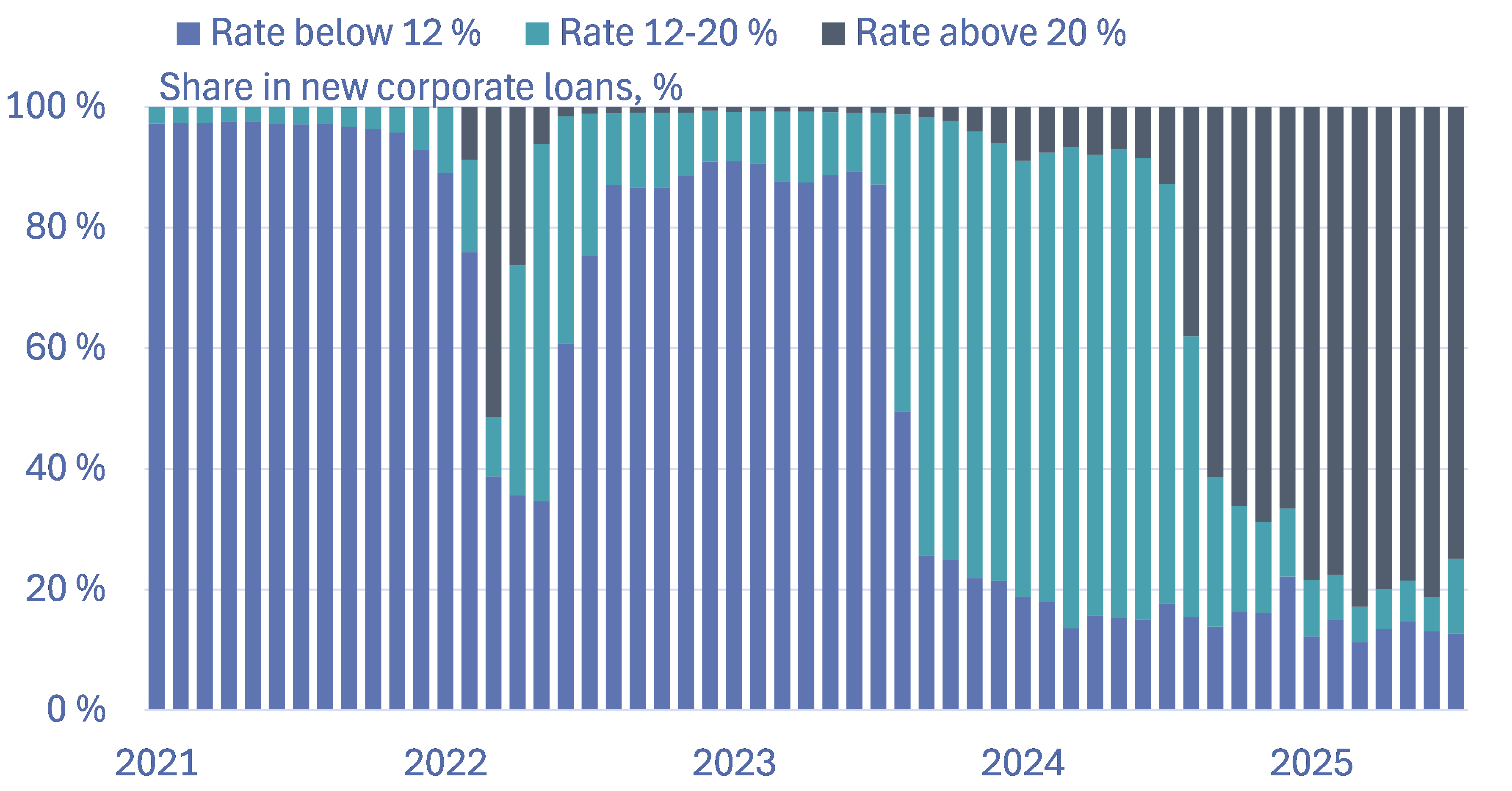

Lending rates have taken off in recent months in response the CBR’s key rate. The record-high setting of the key rate is now reflected in the rates charged on recent loan issues. The bulk of loans granted this year carry interest rates in excess of 20 %. Even with high interest rates, the contribution of bank loans to overall financing of investments has continued to rise this year. The trend suggests that the government is increasingly shifting its provision of investment support to firms away from direct funding out of the budget to subsidising bank loans in various forms. CBR figures for June show that about 16 % of the total loan stock consisted of loans receiving interest subsidies, with most of these loans consisting of subsidised housing loans. The substantial cutbacks in housing loan subsidy programmes, however, is now manifested in the slowdown in housing construction.

Corporate loan rates have sharply increased in Russia

Sources: Central Bank of Russia, BOFIT.

Federal budget remains deeply in the red

Preliminary figures from Russia’s finance ministry indicate that federal budget revenues increased by 3 % y-o-y in the first eight months of this year. Although oil & gas revenues contracted by 20 %, other revenue streams grew by 14 %. The single largest one-off item in August came from record-high dividend payments to the government by state-owned Sberbank and VTB on last year’s earnings, adding roughly 500 billion rubles to the state coffers. Finance minister Anton Siluanov reported that budget revenues from sales of companies seized by the state have this year already amounted to roughly 30 billion rubles and should reach 100 billion rubles by the end of this year with the conclusion of the sale of major assets such as the Moscow’s Domodedovo Airport.

Although revenues from sources other than oil & gas have grown briskly, they still slightly lag budget projections. Revenues during the first eight months of the year corresponded to roughly 60 % of the revenues expected for the entire year. The 21 % y-o-y increase in federal budget spending significantly outstripped revenue growth in January-August. The federal budget deficit for the same period amounted to 4.2 trillion rubles (2 % of GDP).

The finance ministry is currently drafting modifications to this year’s budget and its latest 3-year budget framework. The latest revisions are expected to generate a larger budget deficit this year than previously projected. This expectation was further bolstered by finance minister Siluanov’s recent comment that the government expects to borrow more money this year than previously planned. Siluanov noted that Russia can easily take on additional debt, even if borrowing opportunities are limited due to lack of access to foreign investors and high borrowing costs. According to Siluanov, the Russian state currently must pay a rate of 14 % on its debt.

Much discussion on CBR rate decision

Russia’s central bank has kept its key rate exceptionally high for many months in its efforts to quell spiking inflation. The effects of high rates have begun to show results in recent months. Growth in both demand and prices has slowed. While tight interest rate policy has moderated economic imbalances, it has also provoked considerable criticism in recent months from politicians, bank chiefs and corporate bosses, who complain that the tight interest rate policies are driving the country into recession. The CBR began to gradually lower rates this summer and analysts expect the CBR board to lower the key rate further by 100–200 basis points at today’s monetary policy meeting.

At the beginning of September, the CBR released its latest economic outlook, including alternative scenarios of economic growth over the next three years. In the base scenario, GDP grows by 1–2 % this year, 0.5–1.5 % next year and 1.5–2.5 % in 2027. The price of Russian oil is expected to average around $55 a barrel this year and in 2026, and then rise to about $60 a barrel in 2027. The CBR’s worst-case scenario sees the average price of oil falling to $30–35 a barrel, with Russian GDP contracting on-year by about 2–3 % in 2026 and 2027.