BOFIT Weekly Review 33/2025

Economic conditions in Russia continue to weaken

Russian output growth has stagnated this year even if the economy has not fallen into recession. Increasingly severe economic imbalances, high interest rates depressing demand and falling oil prices have sapped growth. Even with declining export earnings and reduced budget revenues from lower oil prices, budget spending has been significantly hiked in recent months to stimulate production linked to the war effort. Inflation remains high.

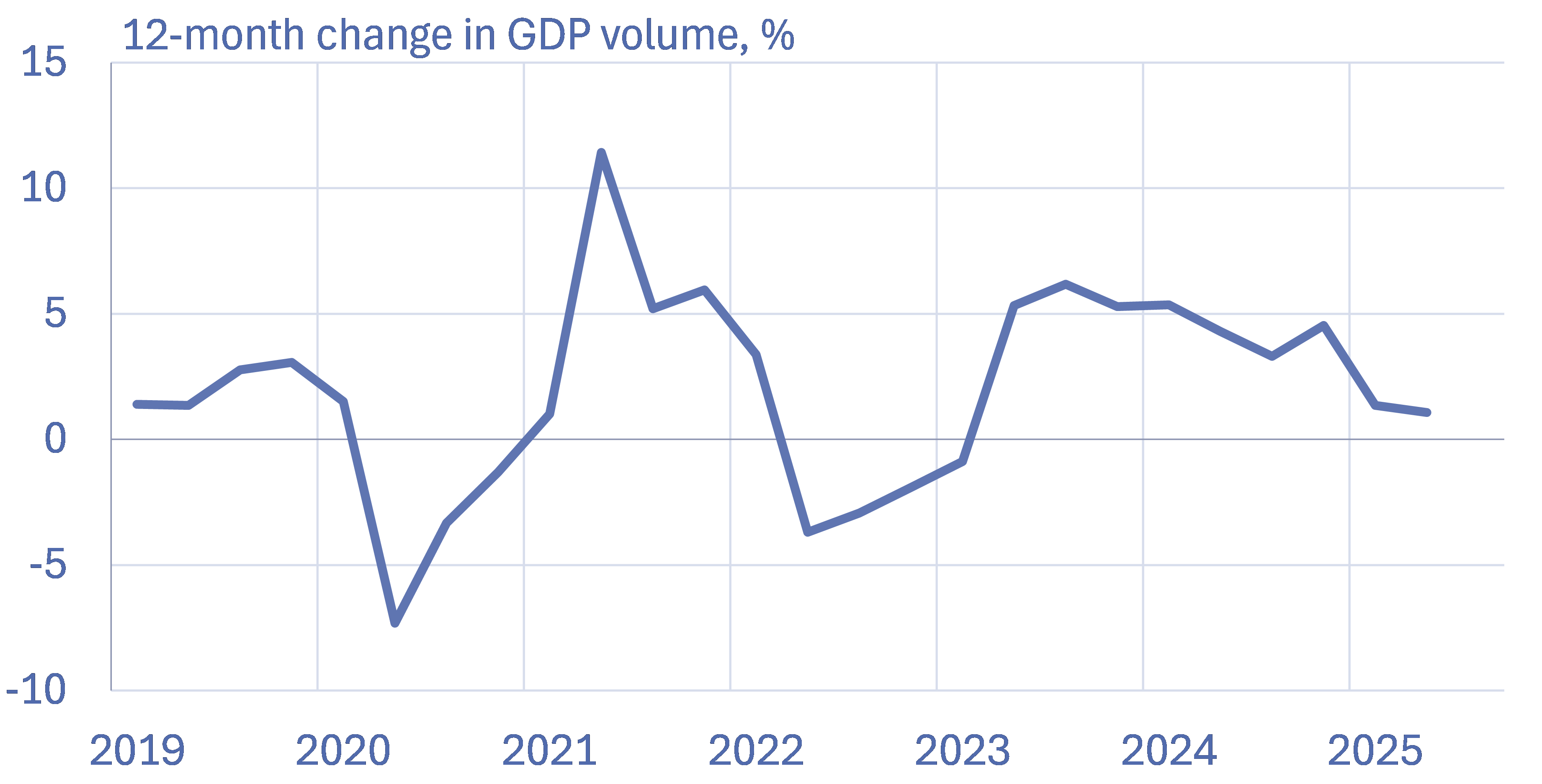

GDP growth slows further in second quarter

Rosstat preliminarily estimates Russian GDP grew by 1.1 % y-o-y in the April-June. Growth slowed further from the first quarter and was slower than expected. The latest forecast of the Central Bank of Russia (CBR) estimated second quarter growth at 1.8 % y-o-y and Bloomberg’s latest analyst survey at 1.5 %. Preliminary data also suggest that Russia’s on-quarter output returned to slight growth, thereby avoiding recession. First-half growth was 1.2 % y-o-y.

International forecasters in recent months have cut their forecasts of Russian GDP growth for this year. The IMF now expects Russian GDP to rise by 0.9 % this year and 1 % next year. The July report from Consensus Economics, an average of analyst forecasts, predicts 1.4 % growth this year and 1.3 % in 2026. The CBR did not revise its earlier forecast for the Russian economy in its update released at the beginning of August, and still expects GDP to grow by 1–2 % this year and 0.5–1.5 % next year.

Future economic trends could also be affected by today’s (August 15) meeting of presidents Donald Trump and Vladimir Putin in Anchorage, Alaska. While a major breakthrough in peace negotiations is largely not expected prior to the meeting, an outcome favourable to Russia would reduce pressures on its economy. On the other hand, if US would impose additional sanctions on Russia, that could severely exacerbate an already-deteriorating economic situation in Russia.

Russian GDP growth slowed further in the second quarter of 2025

Sources: Rosstat, BOFIT.

Output contracted in many branches this year

Industrial output has contracted in most branches of the Russian economy this year. While manufacturing, lifted by industries connected to the war effort, continued to grow overall, other branches suffered from declines in output (including foodstuffs, metals, automobile manufacturing and machinery & equipment). Output of the extractive sector declined by 2 % y-o-y in the first half of this year. The poor performance of extractive sector was apparently reflected also in a contraction in the volume of transport and wholesale activity in the first half of this year.

Household situation has also weakened. Growth in the construction sector has evaporated in recent months. Housing construction, in particular, has weakened. Residential housing construction fell by 2 % y-o-y in the first half of this year. Growth in housing loans has slowed with the phasing out of many support programmes. Retail sales still grew by 2 % y-o-y in 1H25, and commercial activity continued to be supported by wage increases and low unemployment. Many large Russian firms, however, have already announced that they are transitioning to a shorter work week. Both demand and corporate profitability have declined.

CBR lowered its key rate in July

The CBR attributes lower economic growth to reduced demand and estimates that inflation has fallen faster than expected in recent months. In response, the CBR board decided at July 25 meeting to lower the key rate by 200 basis points to its current level of 18 %. In June, the CBR began lowering the key rate from its historical 21 % high.

The CBR still sees such risk factors as persistently high inflation expectations and potential changes in the ruble’s exchange rate could sustain high inflation in the months ahead. The CBR guidance for its next scheduled rate meeting on September 12 was neutral. The CBR board will assess the need for further rate cuts based on realised economic performance and price trends in Russia.

The CBR’s updated forecast sees inflation declining slightly faster than it earlier expected. July consumer prices rose by 9 % y-o-y. The on-year rise in consumer prices are expected to slow to around 6–7 % at the end of this year. 12-month inflation is expected to reach the CBR’s official 4 % target by the end of next year. The forecast also sees the key rate averaging about 19 % this year, and then falling to around 12–13 % next year.

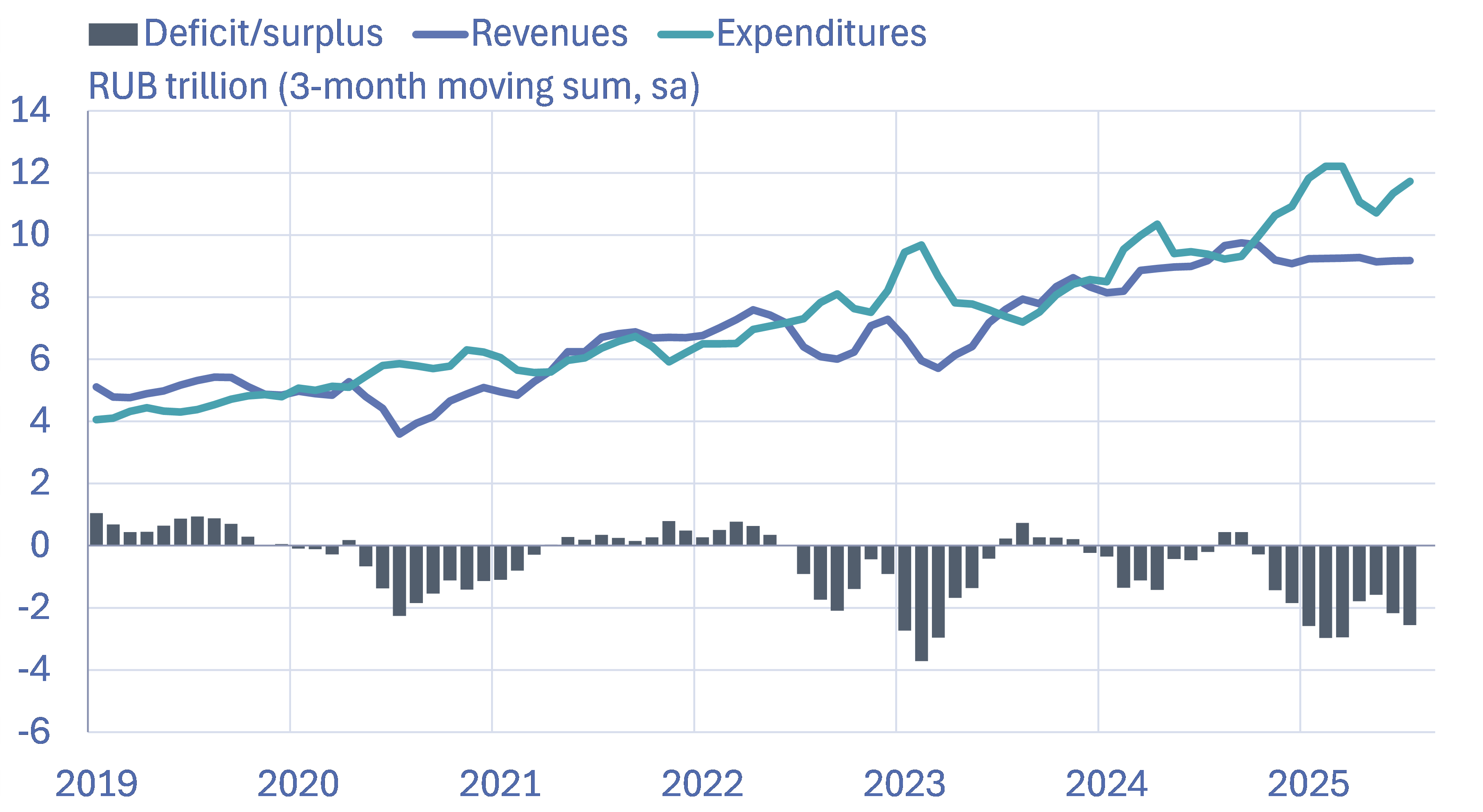

Federal budget deficit balloons

Preliminary figures released by Russia’s finance ministry show federal budget revenues in the first seven months of this year were up just 3 % y-o-y. Oil & gas revenues fell by 19 % on lower oil prices. Other revenue streams grew by 14 %. Due to a sharp increase in the profit tax in at the beginning of this year, revenues from corporate profit taxes, in particular, rose rapidly. The growth in revenues from value-added taxes was largely driven by the rapid rise in prices.

Federal budget spending increased by 21 % y-o-y in January-July. The deficit swelled further in July, amounting to a deficit of nearly 5 trillion rubles (2 % of GDP) for the first seven months of the year. The finance ministry explains that the large deficit reflects the fact that annual budget spending has become more front-weighted than earlier. In recent years the budget spending has nevertheless spiked also at the end of the year.

The budgeted federal deficit for the current year is 3.8 trillion rubles. This year’s budget framework was changed in June when the planned deficit was increased significantly. The finance ministry has already announced its intention to again revise the budget framework in September. While no detailed information has been released, the budget deficit is expected to increase further.

The valuation of the National Welfare Fund (NWF) was bolstered by the transfer of oil revenues collected earlier by the government. NWF liquid assets at the beginning of August were valued at 4 trillion rubles, an amount just barely sufficient to cover this year’s planned budget deficit.

While federal budget revenues have remained flat, spending has risen quickly in recent months

Sources: Russian finance ministry, CEIC, BOFIT.

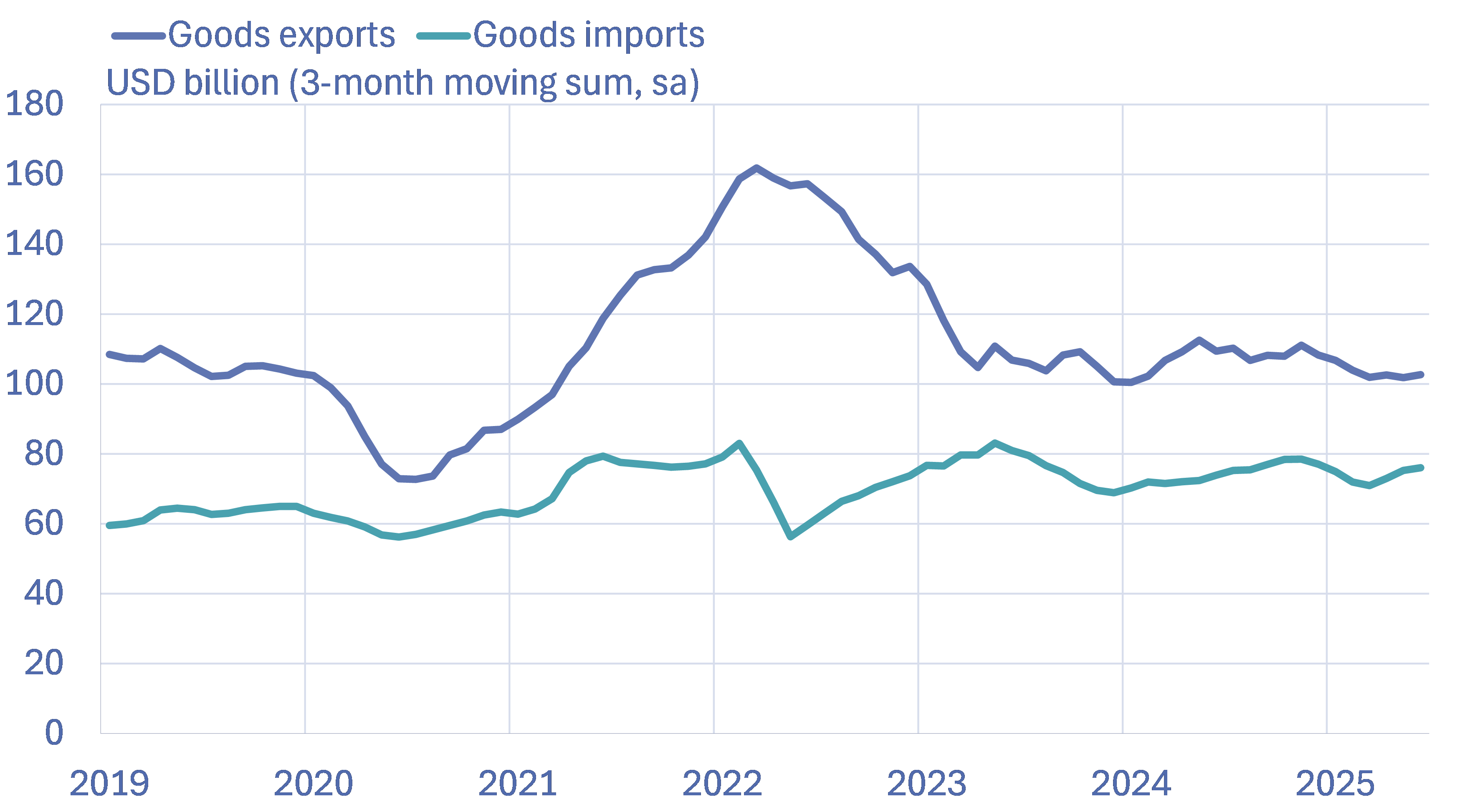

Foreign trade declines

The value of Russian goods exports has contracted in recent months. The value of exports fell by 8 % y-o-y in June. Exports were particularly hard hit by the drop in global oil prices and new sanctions imposed on Russian oil. According to the International Energy Agency (IEA), the average export price of Russian crude oil in the first half of this year was approximately $60 a barrel, a drop of 16 % y-o-y. The average discount on Russian oil compared to similar blends has decreased slightly in recent months to around $11 a barrel. In January-June, the value of Russian goods exports contracted by 6 % y-o-y to $196 billion.

After slight growth last spring, good imports dipped slightly this summer. The value of imports fell by 1 % y-o-y in June. Imports were subdued by fading demand, and particularly the effect of high interest rates on the acquisition of investment goods. Car imports from China have declined sharply after the increase in recycling fees on imported cars. The value of Russian goods imports in the first of this year amounted to $139 billion, an increase of about 1 % y-o-y.

The newest EU sanctions package further restricts Russian foreign trade. In mid-July, the European Council approved its 18th sanctions package, tightening restrictions on Russian commodity exports. The latest round of sanctions and their implications are discussed in detail in this recent BOFIT blog post. The United States has stated to impose an additional 25 % import tariff on India at the end of August if India continued to purchase Russian oil.

Russia’s goods trade has shrunk in recent months

Sources: Central Bank of Russia, BOFIT.