BOFIT Weekly Review 26/2025

China invests heavily in domestic production of critical raw materials

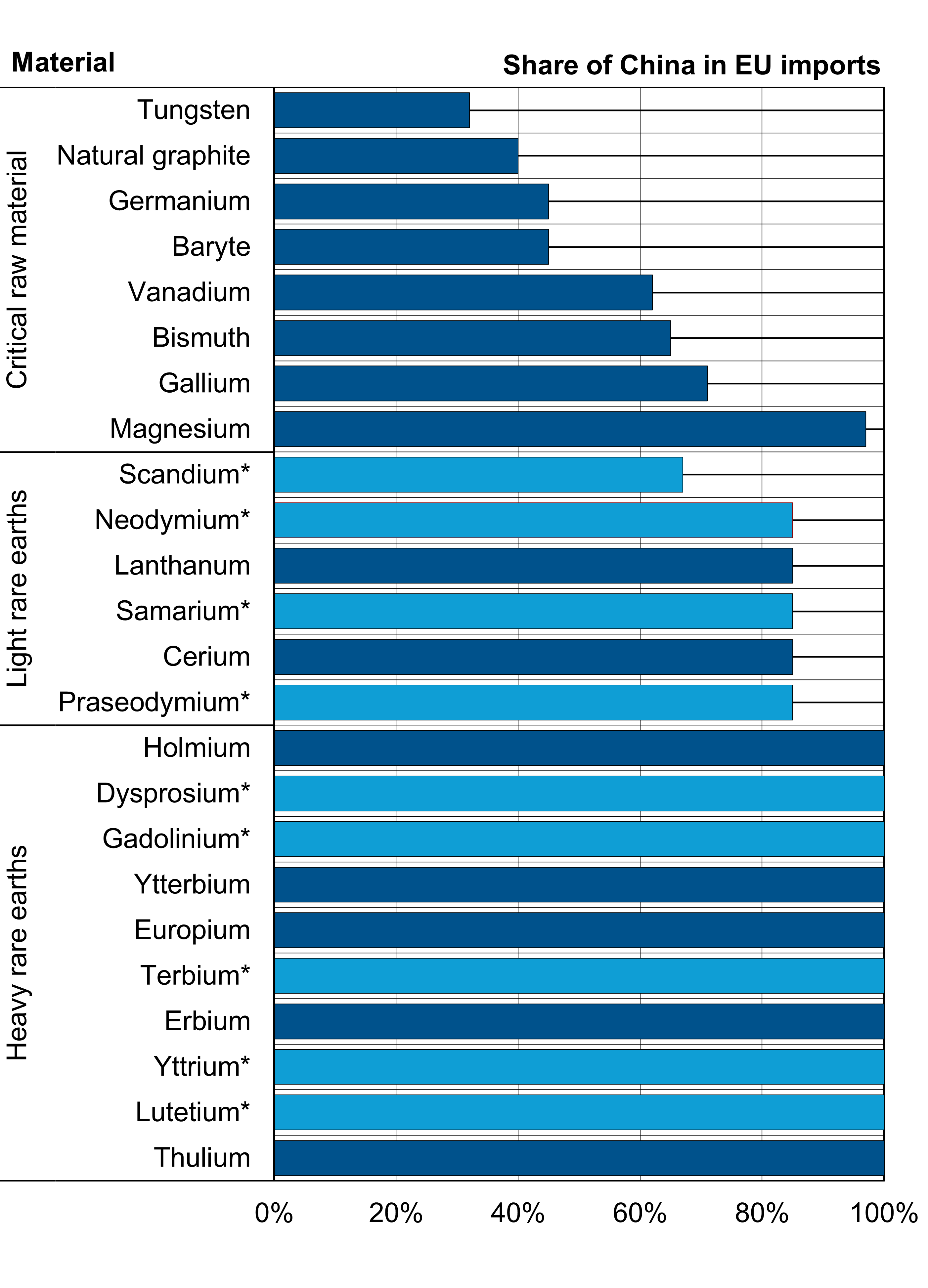

China is the global leader in production of many critical raw materials, and the country is investing heavily in mining and refining operations related to rare earth elements (REEs). Rare earths are, alongside a number of other materials, classified as critical raw materials due to their economic and strategic importance. Rare earths, including some vital to the production of permanent magnets, are essential to industries involved in production of electronics, defence applications, electrical motors and wind turbines. China is the top global producer of numerous critical raw materials and is uniquely dominant in REE processing. The European Union’s 2023 assessment of critical raw materials shows that of the 34 raw materials critical to EU production, China is the largest supplier of 24 of those materials. The International Energy Agency (IEA) reports that over 90 % of rare earths refining took place in China last year.

China has invested heavily in its rare earths production in recent years, particularly at the local level, and have increased monitoring of their rare earths supply chain. Changes include regulatory requirements that firms record and report which REE they use and the quantities used in production, as well as by setting production targets for REE mining and refining activities.

While China’s refining and processing operations are largely based inside the country, it remains extensively reliant on the mining operations of Chinese mining companies abroad for raw inputs. In response, the central leadership has significantly increased funding for domestic geological exploration. Many local governments have also increased their support for exploration. China also grants its mining sector lavish tax breaks and subsidies.

In terms of 2024 market capitalisation, China’s annual “energy mineral” production (includes REEs, nickel, lithium, natural graphite and manganese, among some others) broke down into roughly $35 billion from mining activity and $106 billion from refining activity. When currently announced investment projects are included, projected annual contributions rise by 2040 to $68 billion from mining and $176 billion from refining. In contrast, China’s coal industry last year accounted for over half of the net sales of $810 billion posted by China’s mining sector. By investing in domestic mining operations, China seeks to assure stable supply of critical raw materials and improve the resilience and competitiveness of the supply chains of Chinese firms.

Concern in policy circles over China’s significant role in the production and processing of critical raw materials surfaced in April after China imposed export restrictions on certain REEs in response to the reciprocal tariff increases proposed by the Trump administration. China had already restricted the exports of certain critical raw materials. While the countries reached an interim agreement at the start of June, China has kept its export-permitting regime in place for REEs and permanent magnets. This requirement has disrupted many global production chains dependent on inputs subject to China’s tight permitting process. For example, Japanese firms in June began to report that export restrictions had already begun to affect Japanese industries and requested that China expedite the granting of export permits. Europe’s carmakers are also concerned about the impacts of the export restrictions. In June, China promised to accelerate the granting of export permits to European firms. The volume of Chinese permanent magnet exports fell by 74 % y-o-y in May and 53 % from the previous month.

The EU depends on China for a wide range of critical materials

* Light blue bars indicate materials subject to export restrictions as of April 2025

Sources: European Union (2023), BOFIT. Import shares for 2016–2020.