BOFIT Weekly Review 25/2025

Russian central bank lowers its key rate; growth in corporate borrowing slows

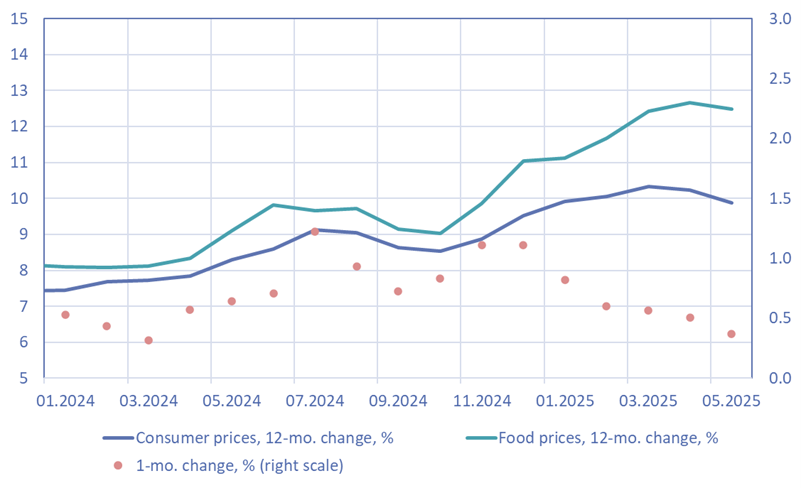

At its regular meeting on June 6, the Central Bank of Russia’s board of directors decided to lower the key rate by 100 basis points to 20 %. The CBR raised the key rate several times during autumn 2024 in an effort to quell soaring consumer prices. During April and May 2025, the average rate of rise in prices seemed to taper off. While 12-month inflation for all goods and services was still hovering around 10 % in May, on-month inflation showed signs of a gradual slowdown. The CBR stated that slowing of the month-to-month change in prices and lower growth in bank lending left room for a rate cut even with inflation still well above the CBR’s official 12-month inflation target of 4 %.

Prices for many food items and various services have continued to climb faster than the average rise in prices. In contrast, prices for non-food goods such as clothing and certain home appliances have only risen slightly over the past year. Many of the durable consumer goods included in Russia’s consumer price index are imported, so recent ruble appreciation has eased inflationary pressures.

Falling interbank rates, which closely track the CBR’s key rate, are expected to be bleed through to lower bank lending rates. The effects from adjustments in the key rate on bank lending could be dulled by the rapid growth in government spending and generous government loan-subsidy programmes. Even with the rate cut, the CBR’s monetary stance remains tight and lending rates quite high. These conditions will continue to dampen growth of the credit stock overall.

The rise in consumer prices has slowed in recent months

The 1-mo change in consumer prices is seasonally adjusted by the CBR

Sources: Rosstat, Central Bank of Russia, BOFIT

Growth in corporate credit has slowed this year

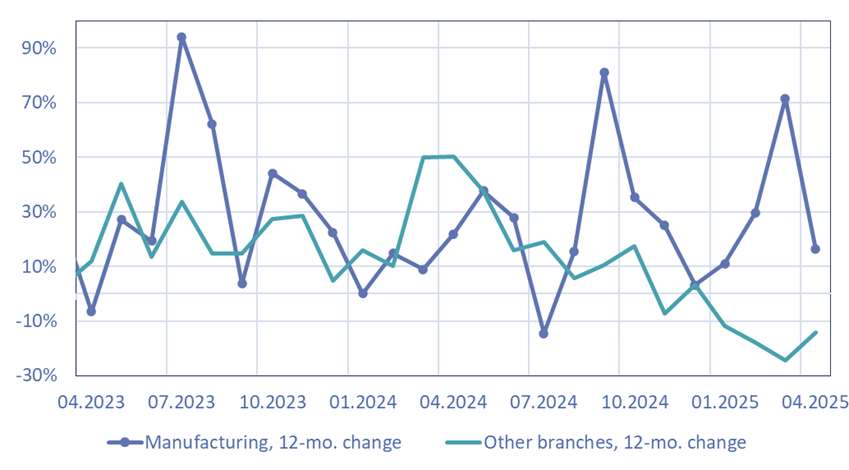

During the first three months of this year, banks slightly reduced their corporate lending from the same period in 2024. Looking at bank corporate lending at branch level, it appears most growth in new loans came from lending to a handful of manufacturing branches. New lending was particularly strong in the first quarter for firms involved in chemicals production, petrochemicals and metals refining. Production increases in these branches reflect strong orders for military materiel to support the war effort. In many other sectors, the volume of new credit has diminished sharply. For the first quarter, manufacturing accounted for well over 20 % of all new corporate loans. The average maturity of loans in the corporate loan stock is quite short, which partly accounts for the large monthly fluctuations in the volume of new loans issued.

Volume of new loans to corporations in manufacturing sectors continued to grow this year

Change in volume of new corporate loan issues from 12 months previous

Sources: Central Bank of Russia, BOFIT

The total corporate lending stock of banks at the start of May was 86.1 trillion rubles, a slight drop from the start of the year. In the first quarter of this year, growth of the loan stock was subdued by high interest rates, stricter capital adequacy requirements for banks and substantial advance payments from the budget to cover payments on public procurement orders. On-year growth in the loan stock slowed from last year’s growth pace above 20 % to just 14 %. No similar slowdown was seen for corporate bond issues.

Fixed-rate loans represent a diminishing share of corporate loans in recent years. As of end-March, 65 % of the corporate loan stock consisted of adjustable-rate bonds, up from less than 40 % three years ago. The average interest rate in March for new corporate loans of less than a year was 18.7 %, but there is no detailed breakdown of subsidised-interest loans available. Company restructurings and payment troubles related to corporate loans have increased, but they still affect only a small share of corporate loans overall. The CBR reports that the capital adequacy ratios of Russia’s banking sector remain at a high level and that banks’ reserves are sufficient to cover potential credit losses.

Rising government debt

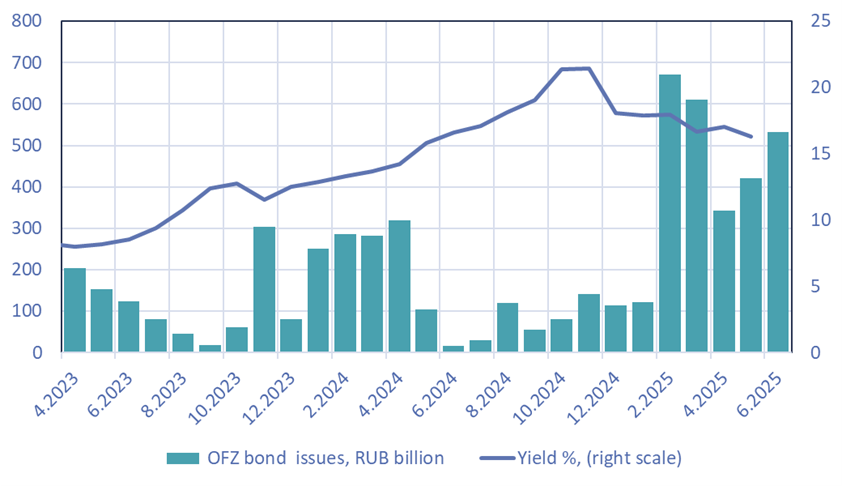

Despite high interest rates, ruble-denominated bond issues have increased sharply this year. The original 2025 budget plan called for issuance of approximately 4.8 trillion rubles worth of new bonds, of which about 1.8 trillion rubles raised would go to paying down maturing bonds. During the first five months of this year, government bond borrowing amounted to roughly 2.2 trillion rubles. The total amount of government bonds on issue as of end May was 24.425 trillion rubles, a 20 % increase from end-May 2024. The pace of bond borrowing accelerated in June. By June 19, the finance ministry had issued over 0.5 trillion rubles worth of floating-rate bonds.

Russia’s large state-controlled banks are typically the biggest buyers of new bond issues. January-May figures show that Russian commercial banks purchased 64 % of new bond issues. Sanctions have effectively excluded foreign investors from the Russian bond market. The CBR reports that in the first quarter of this year, foreign investors only purchased 2.5 % of new bond issues. The share of government treasuries held by foreign investors has decreased over the past five years from 32 % to less than 4 %.

Following the June rate cut, the average yield on bonds with maturities of less than a year was about 17 % and about 15 % for 10-year bonds. Government and corporate ruble bonds are traded on the Moscow Exchange.

The amount of government bond issues has increased sharply this year

Average yield for OFZ federal loan bonds with 2-year maturity

Sources: Central Bank of Russia, BOFIT